Market Overview - November 3rd 2025

S&P Index Options & Volatility

Following up on last weeks overview:

With majority of Mag7 earnings behind us (only NVDA and AVGO left in mid Nov) this week is relatively quiet data wise. FOMC last week, however, did not go as smooth as many hoped, with Dec rate cut odds plunging from high 90’s to ~70%. With the gov shutdown we are again likely not getting the NFP print on Friday, likely ISM used as proxy to figure out employment/inflation trends.

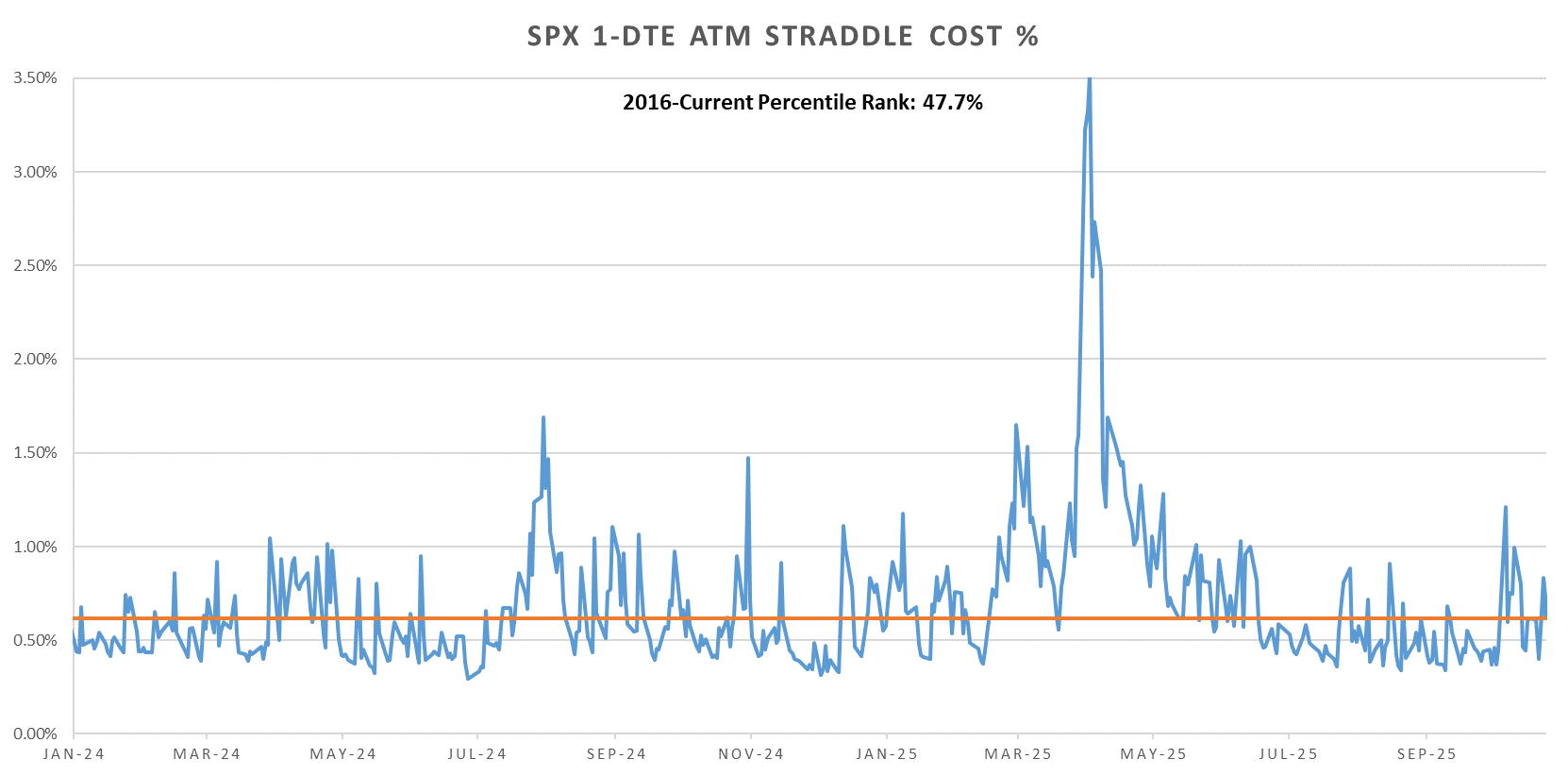

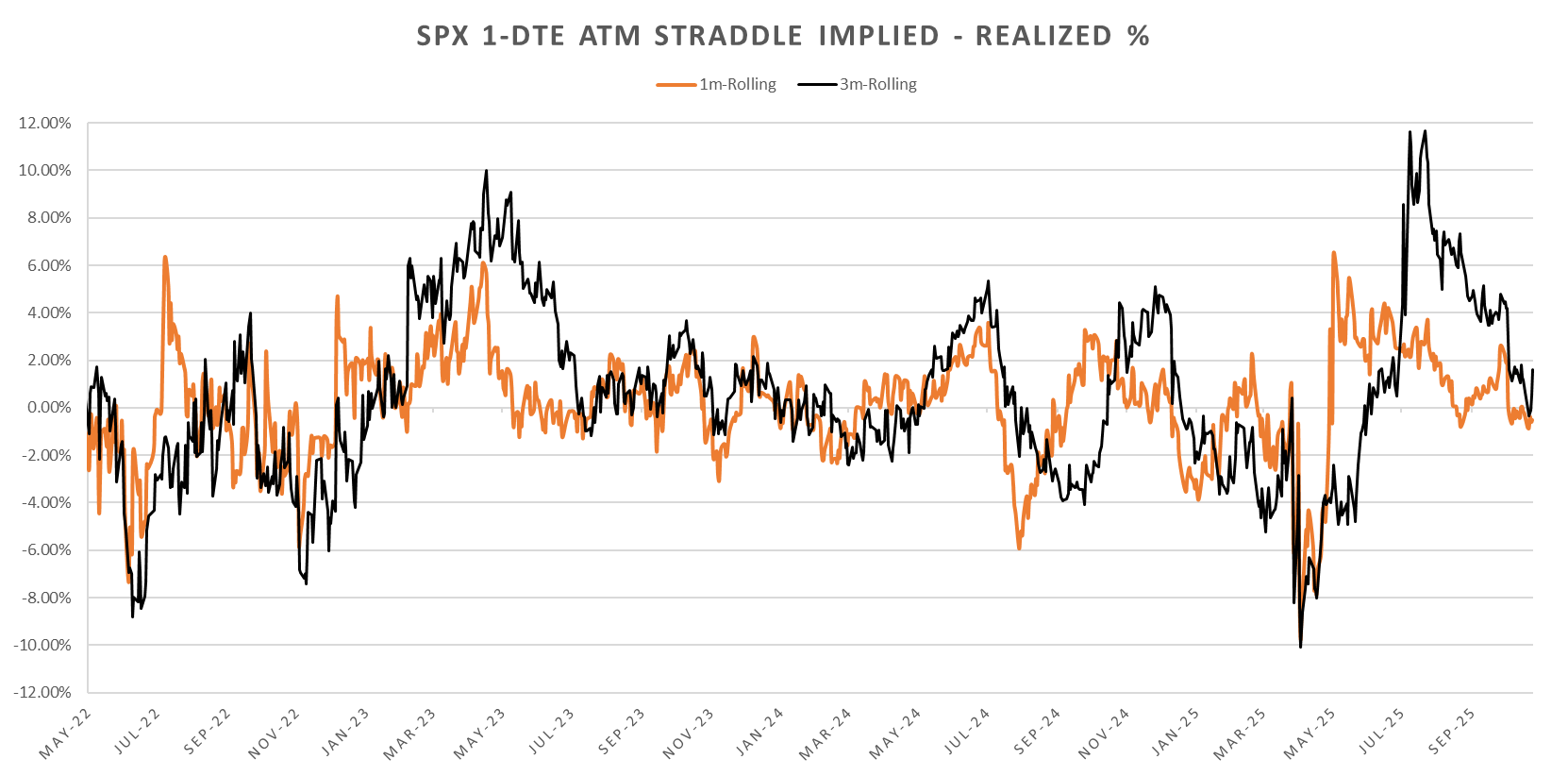

Despite earnings & FOMC behind us, short dated straddle cost not dropping off to lows yet. We’ve got 3m and 1m rolling VRP back down to 0 on a rolling basis as well on the back of wild upside moves we’ve seen in Sep.

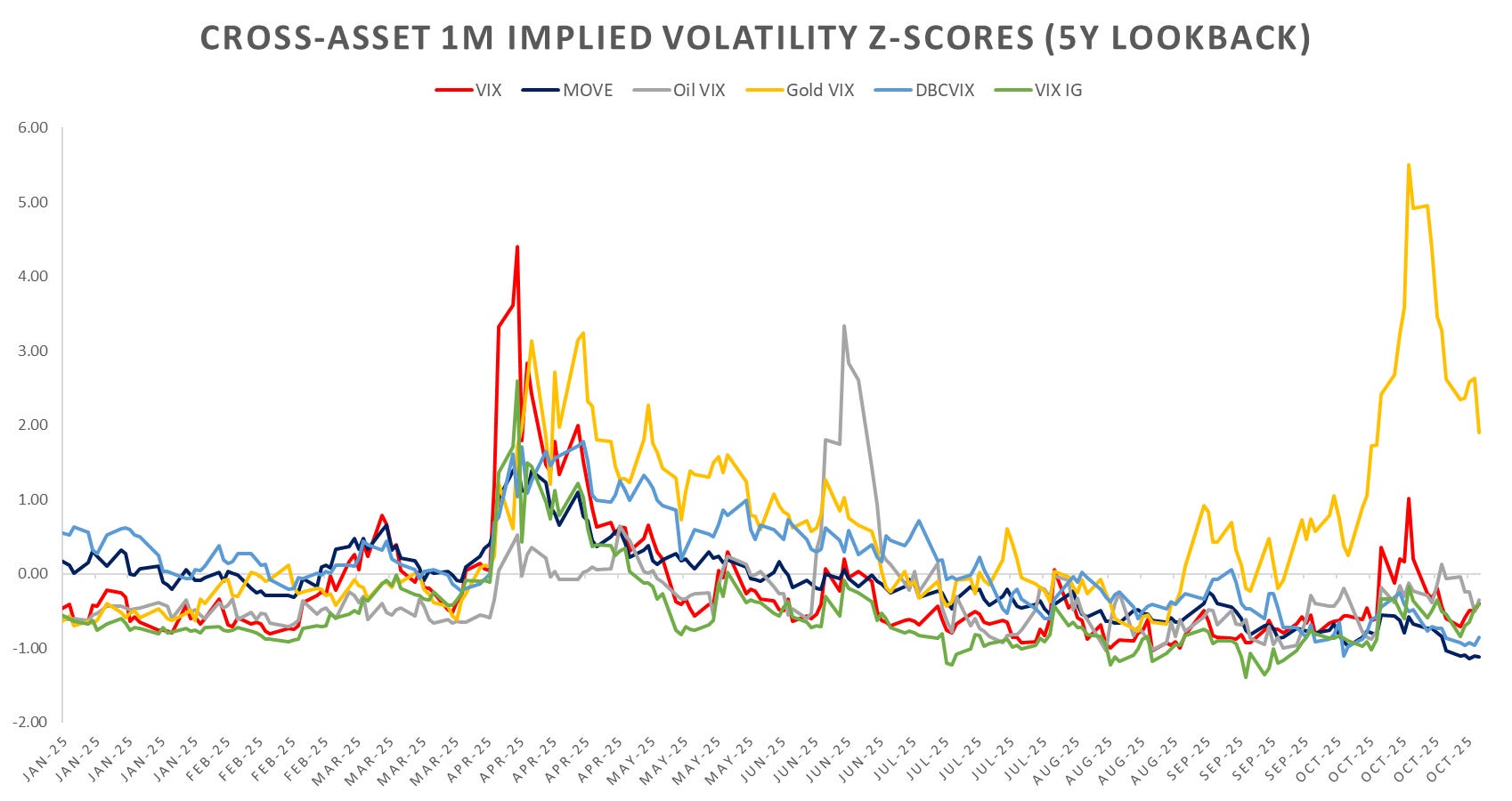

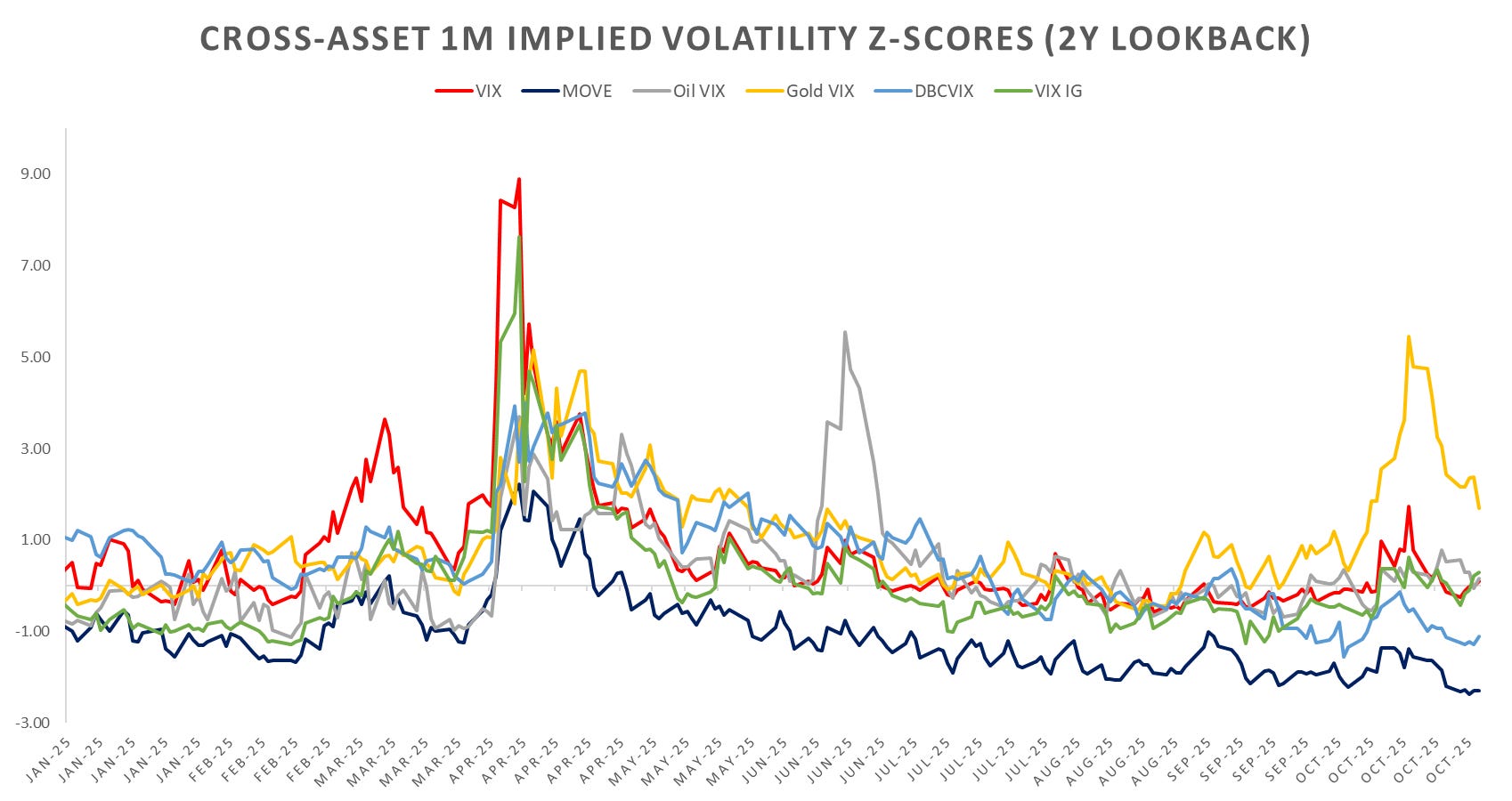

Mixed cross asset vols last week, gold down, rest of assets flat/up after Fed comments on Dec rate cut being “far from a foregone conclusion.”

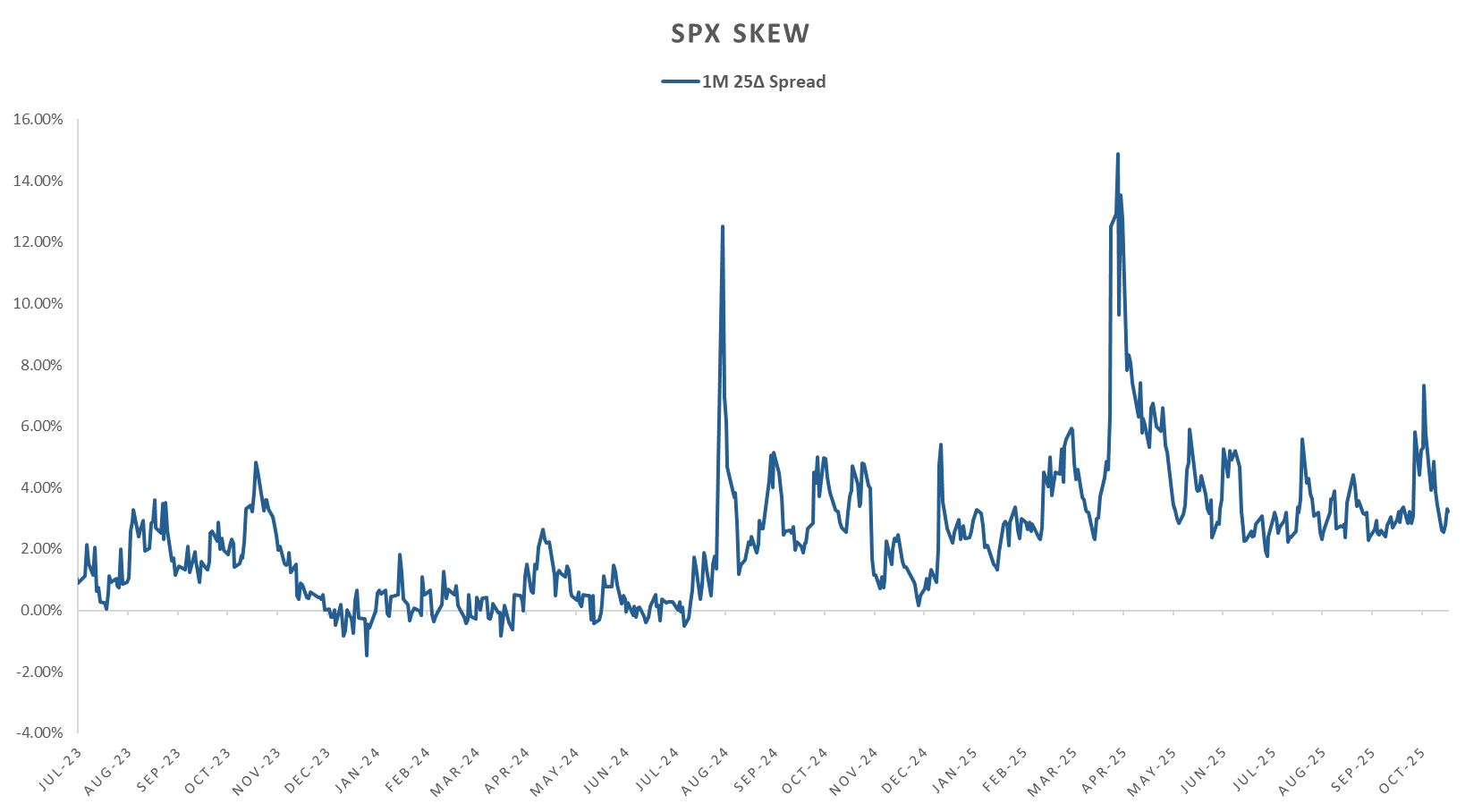

Skew normalized again, 1m 25d spread back to 6 month lows… Tariffs rolled back, economy proves as resilient as one could hope for and Fed going through with rate cuts just kills any chances to see some deeper downside.

Looking at intraday price action:

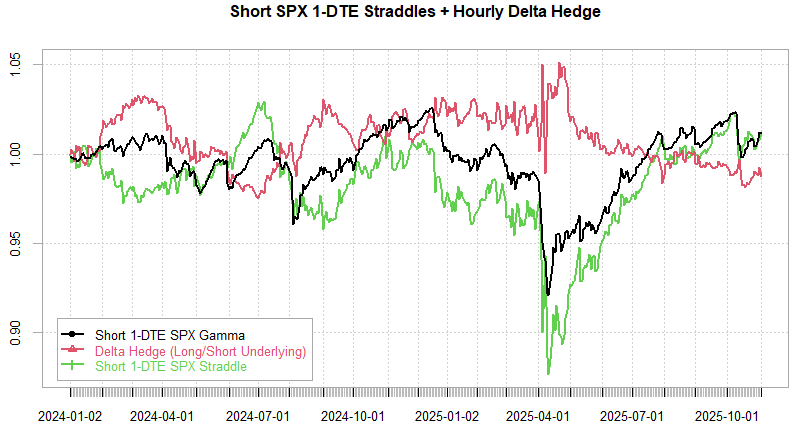

1-DTE SPX straddles hedged/unhedged net up on the week, elevated premiums for earnings / FOMC once again just another opportunity to sell risk premium.

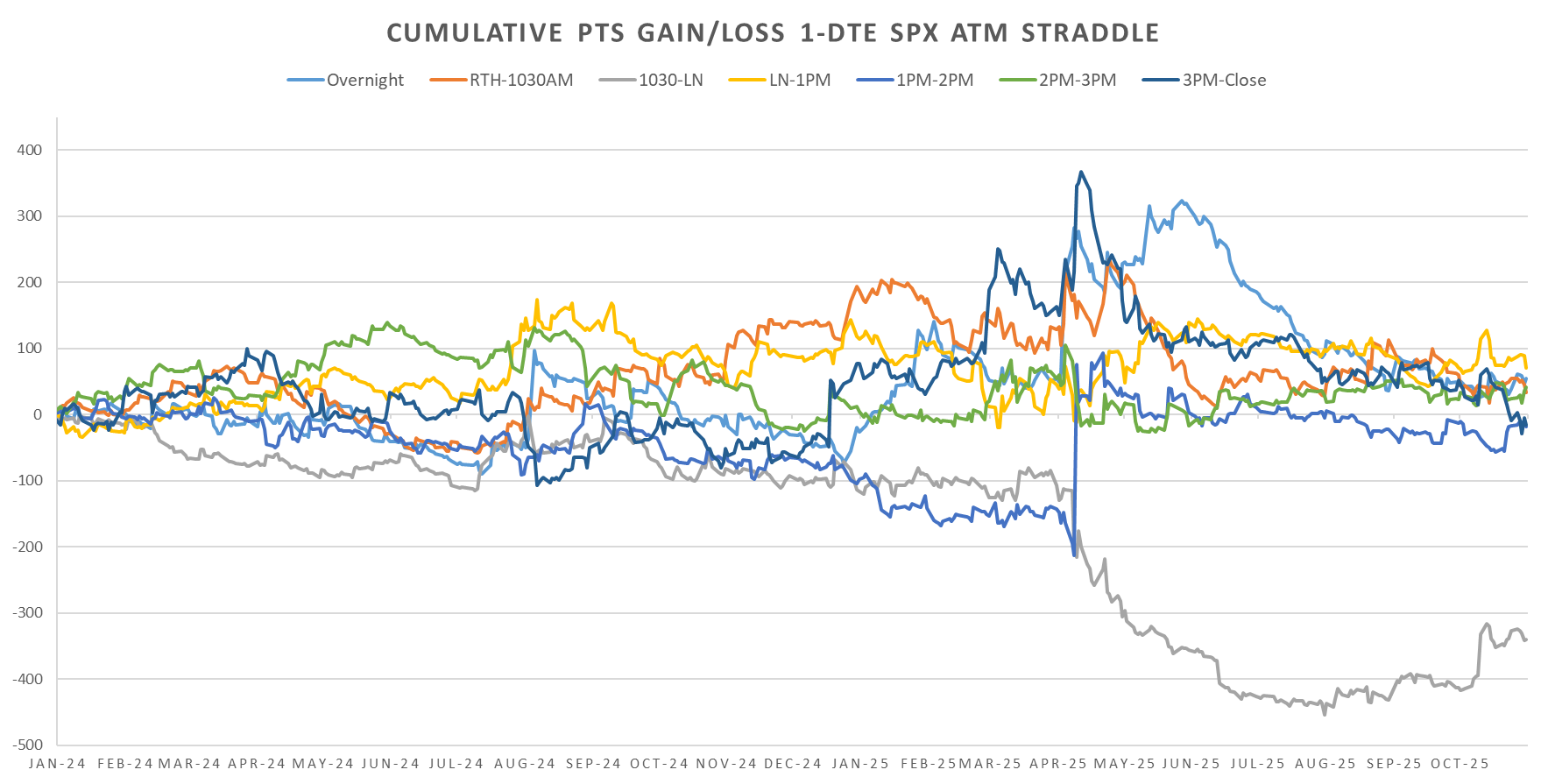

Looking at the 1-DTE SPX straddle cross section, the 3pm-Close time period has been losing momentum ever since the April ‘Liberation Day’ peak. Likely, this is the result of low realized volatility over last 6 months.

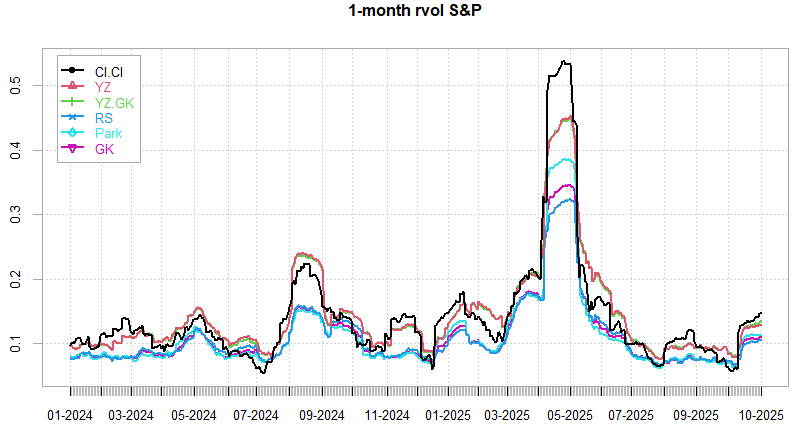

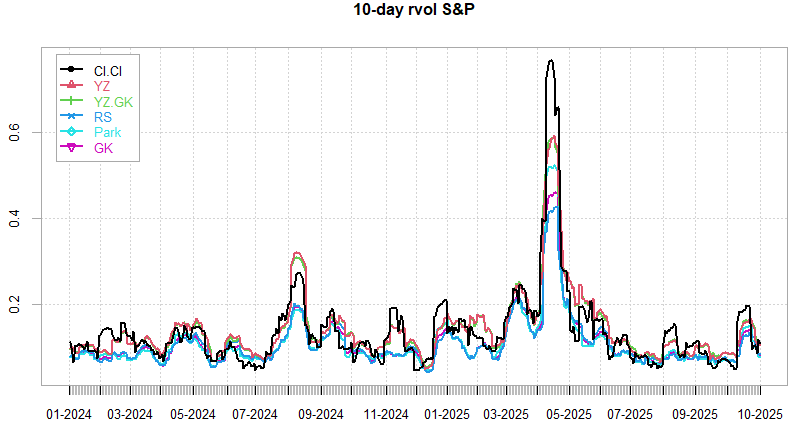

Realized Volatility Overview

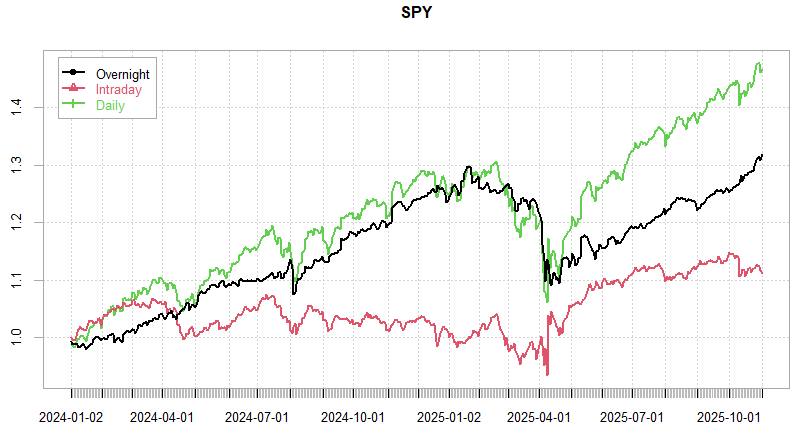

Overnight performance hits new post Jan 2025 peak, almost a 45 degree line up since April. RTH performance once again suffering lately since the China tariff headlines on Oct 10th.

Looking at 10d rvol, RTH ranges leading the way lower last week. ‘Gap up and fade’ is the theme, although any large downside gets retraced by close. Very strong realized dispersion continued into Thursday earnings, down into eow albeit slightly.

Single stock average implied vol down to sub 40 after last weeks earnings. Vast majority of Mag7 1m ivols down to 20’s, 30’s post earnings (10pts off), NVDA / AVGO / TSLA still stuck mid 40’s/50’s. Large cap tech once again leading indices higher, with broader market weak after Dec rate cuts get put into question.

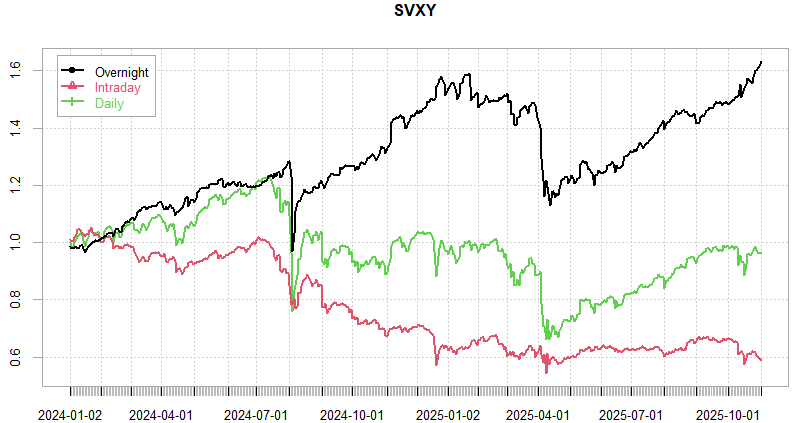

Similar to SPX, VIX Futures overnight short performance hitting new highs with RTH session back to April lows…

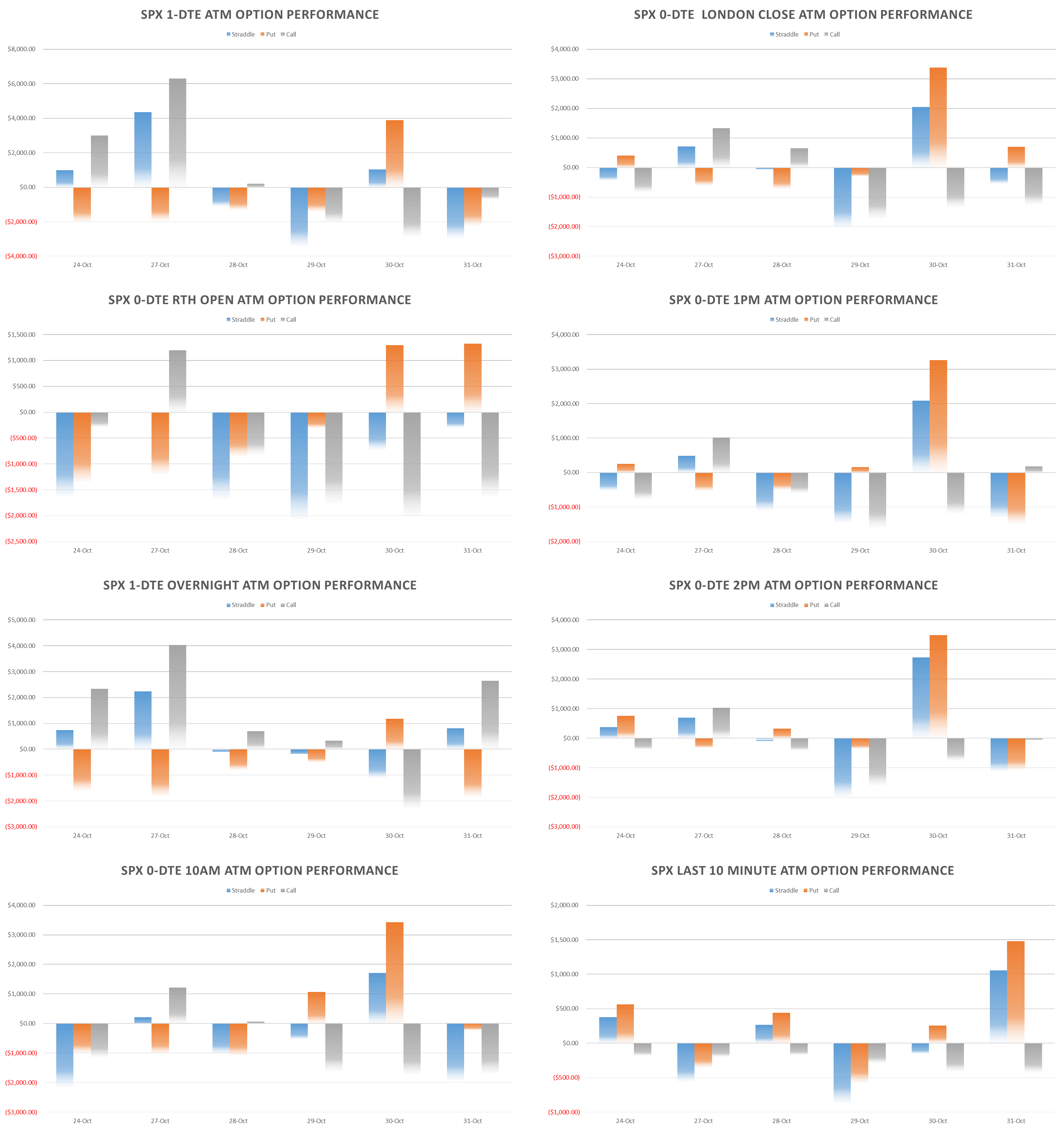

SPX ATM Straddle Performance

RTH straddles biggest winners for 2nd week in a row, down a total of ~60pts over last 6 trading days. High dispersion putting a cap on intraday rvol so shorting ‘event’ premiums continues to pay out.

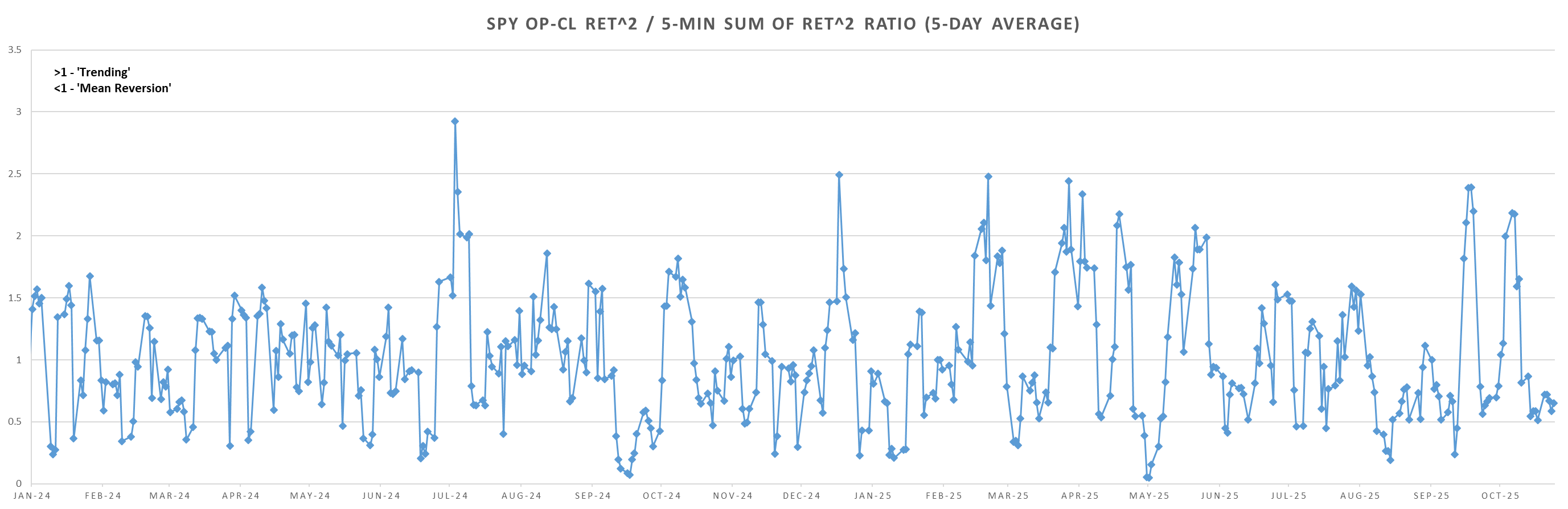

Intraday Variance Ratio

From the following post:

As mentioned further up, strong mean reversion intraday. bias heavily towards long straddles into start of the week.

Overall very choppy performance this year when tracking the var ratio, especially post April… Extended period of low rvol so nothing is happening outside occasional headline that nukes everything.

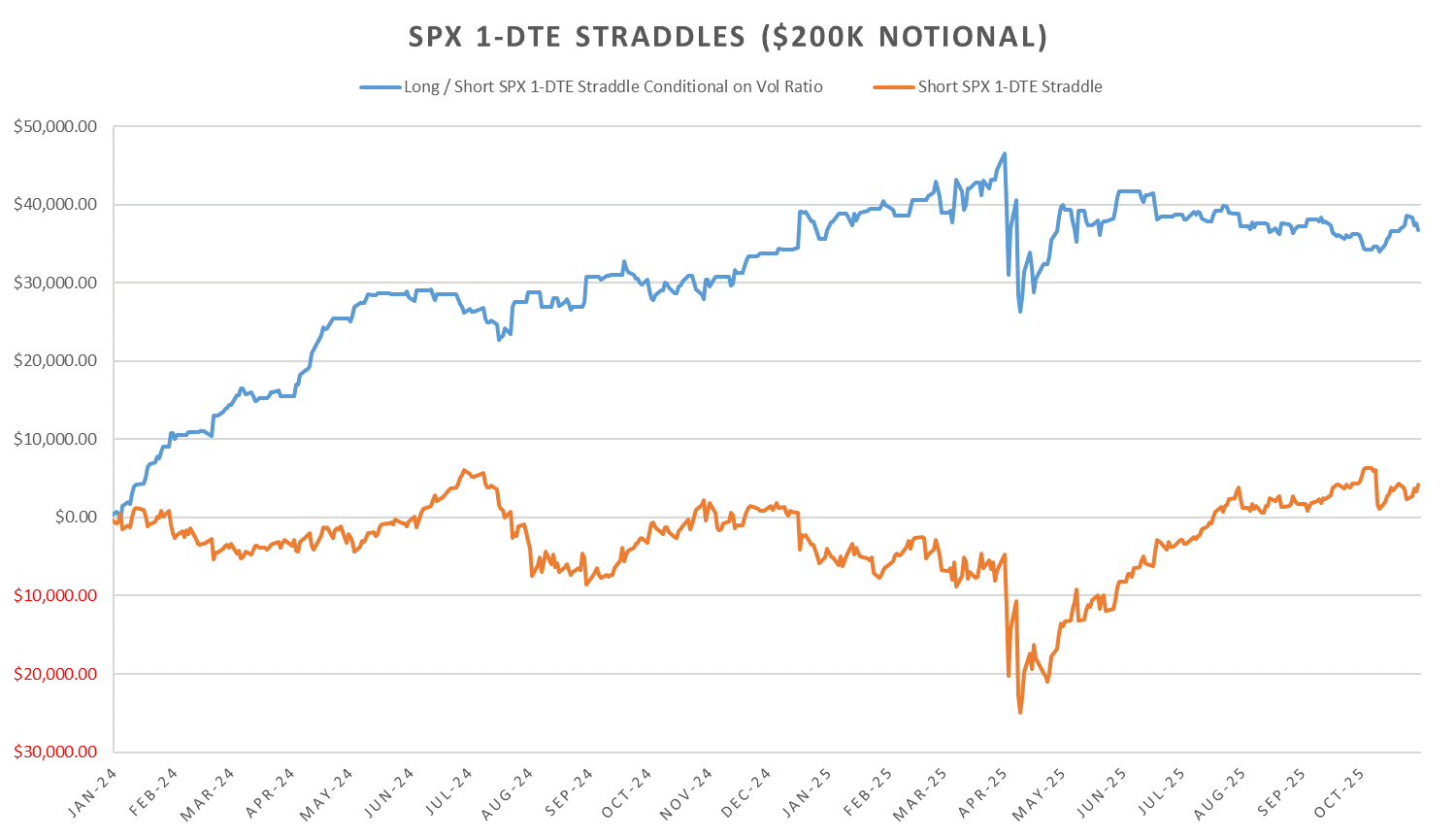

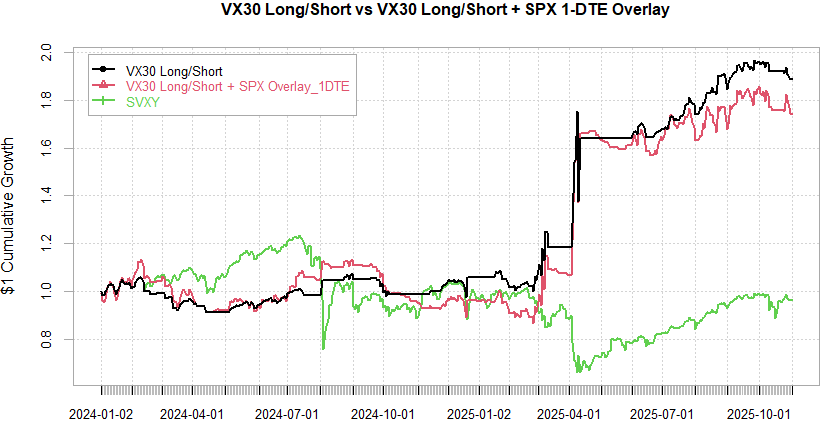

VX Carry & SPX Overlay

From the following post:

Latest short not working out well so far, VIX futures refuse to slide lower. Still, I think there is sufficient cushion into year end to expect a decent roll down by end of Dec, although with Dec rate cut odds now in question it might take up till Dec 10th meeting to see meaningful downside in Dec/Jan contracts.

As always don’t hesitate to reach out!

Have a great week!

You highlighted how shifting rate expectations and low realized volatility are shaping SPX behavior with clarity. I liked how you connected the persistent mean reversion and skew normalization because it captures the underlying calm despite macro uncertainty. Recent data from JPMorgan shows index option volumes up 20% year over year while realized volatility remains muted, signaling ongoing premium selling. I wonder if others think this structural trade can persist into year-end.

What drove the var ratio l/s 1dte straddle pnl beginning of the year? Not a strong trend for the short strategy beginning of the year, so the strategy must’ve had a very high hit rate?