Variance Ratios using 5-min intraday vol sampling

Using divergences in the intraday / open-close volatility ratio's to improve Long / Short 1-(0) DTE SPX Straddle performance

Follow up for the previous post:

The logic behind the initial attempt at using Variance Ratios was quite simple, find divergences between various volatility estimators and trade the straddle long/short based on these divergences resolving.

Initially we’ve looked at various cl-cl and range based volatility estimators. In this post we will look at sampling the S&P intraday 5-min volatility and hopefully improve the performance of the long/short straddle strategy based on previous volatility estimators.

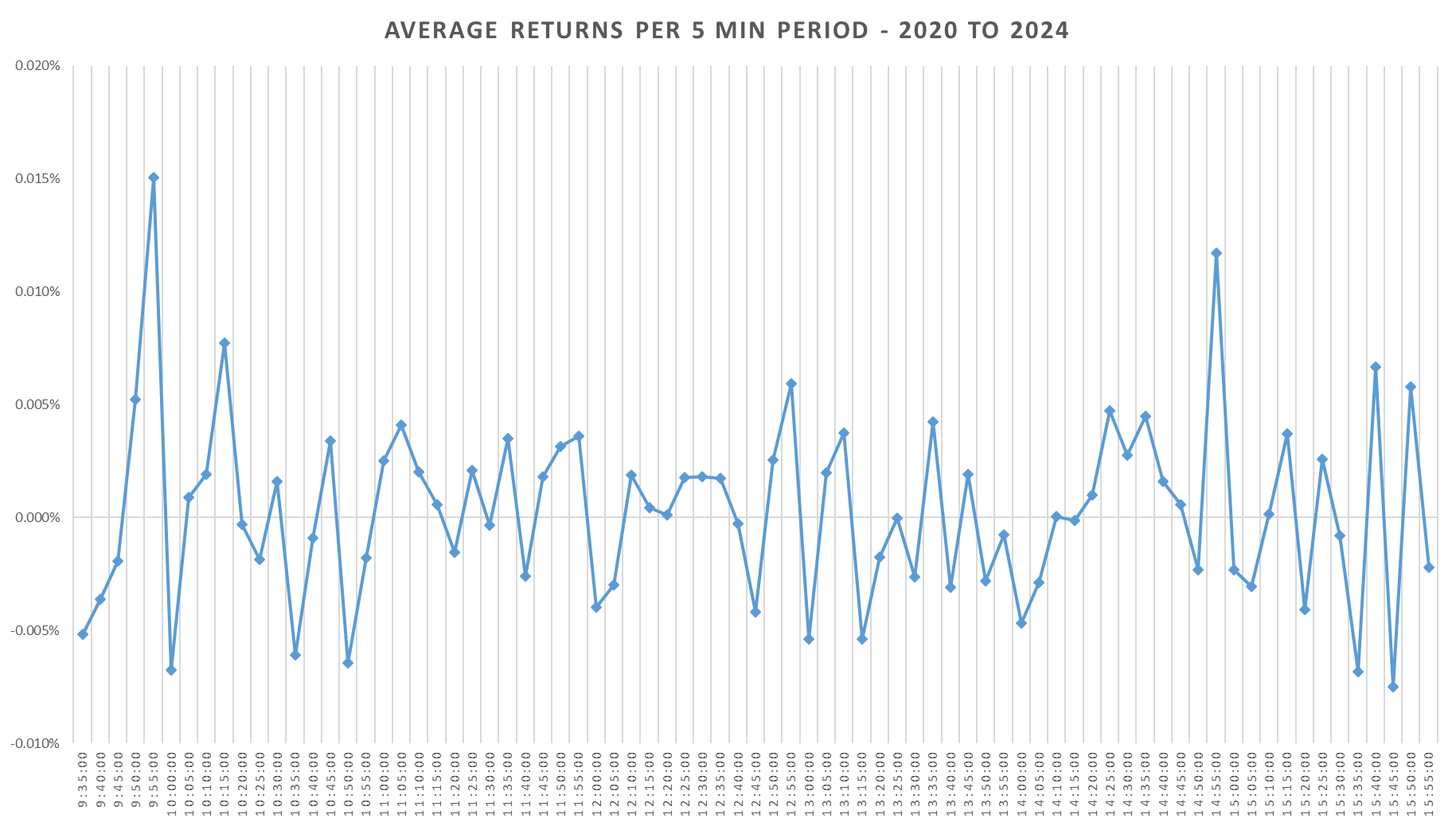

Lets look at some familiar characteristics of the higher frequency intraday returns:

Looking at daily 5 min SPY data between Jan 2020 and Dec 2024 we get the ‘classic’ U-shape in squared returns. Opening & closing 5 min volatility is highest, with volatility putting in a trough around 1pm.

What we are primarily interested is identifying periods of high mean reversion & periods of strong trend. We define the ratio as follows:

Keep reading with a 7-day free trial

Subscribe to Vol Vibes to keep reading this post and get 7 days of free access to the full post archives.