NFP Overview

As we approach the main ‘vol’ event of the week, SPX Straddles for tmrw, at close, traded ~100bps. JPM gives the breakdown for how it expects SPX to react on a beat/miss scenario:

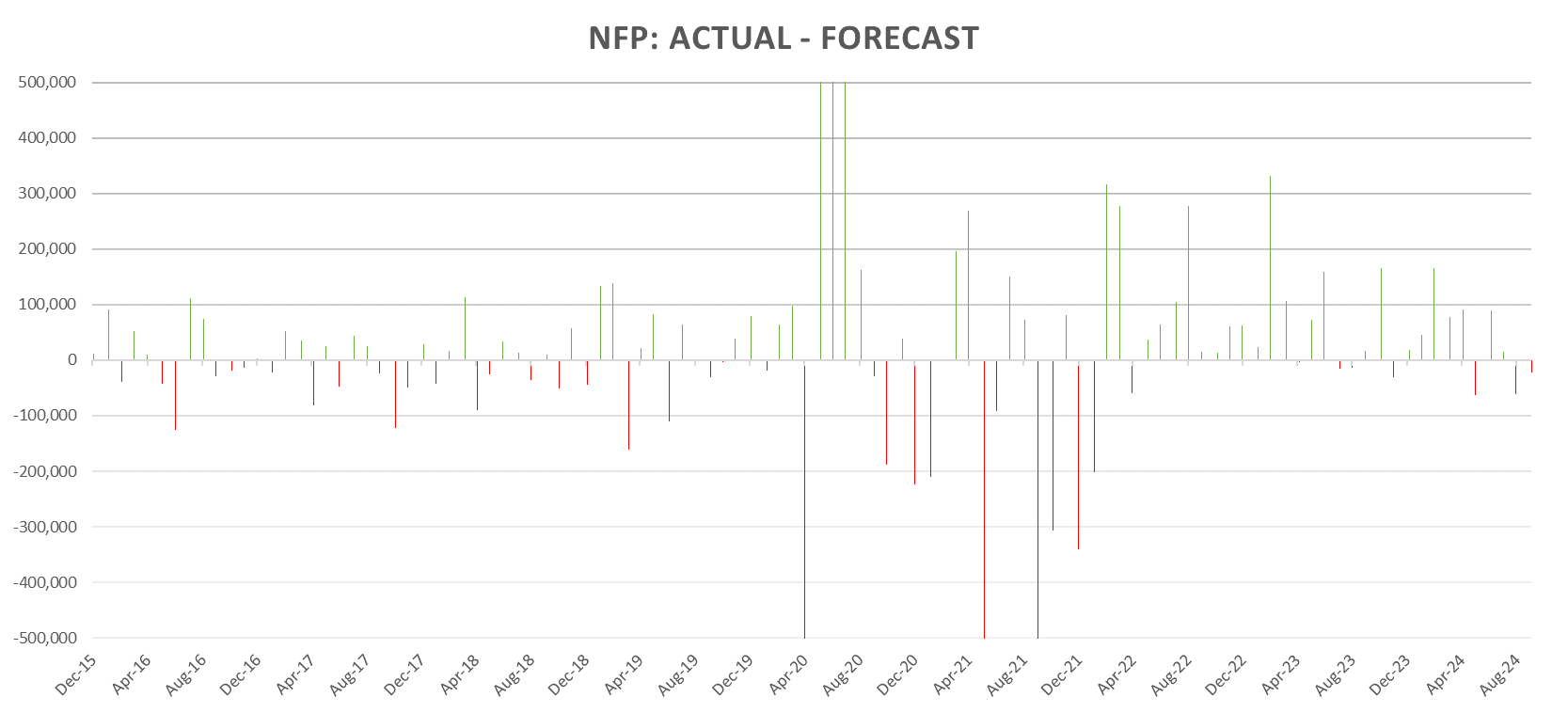

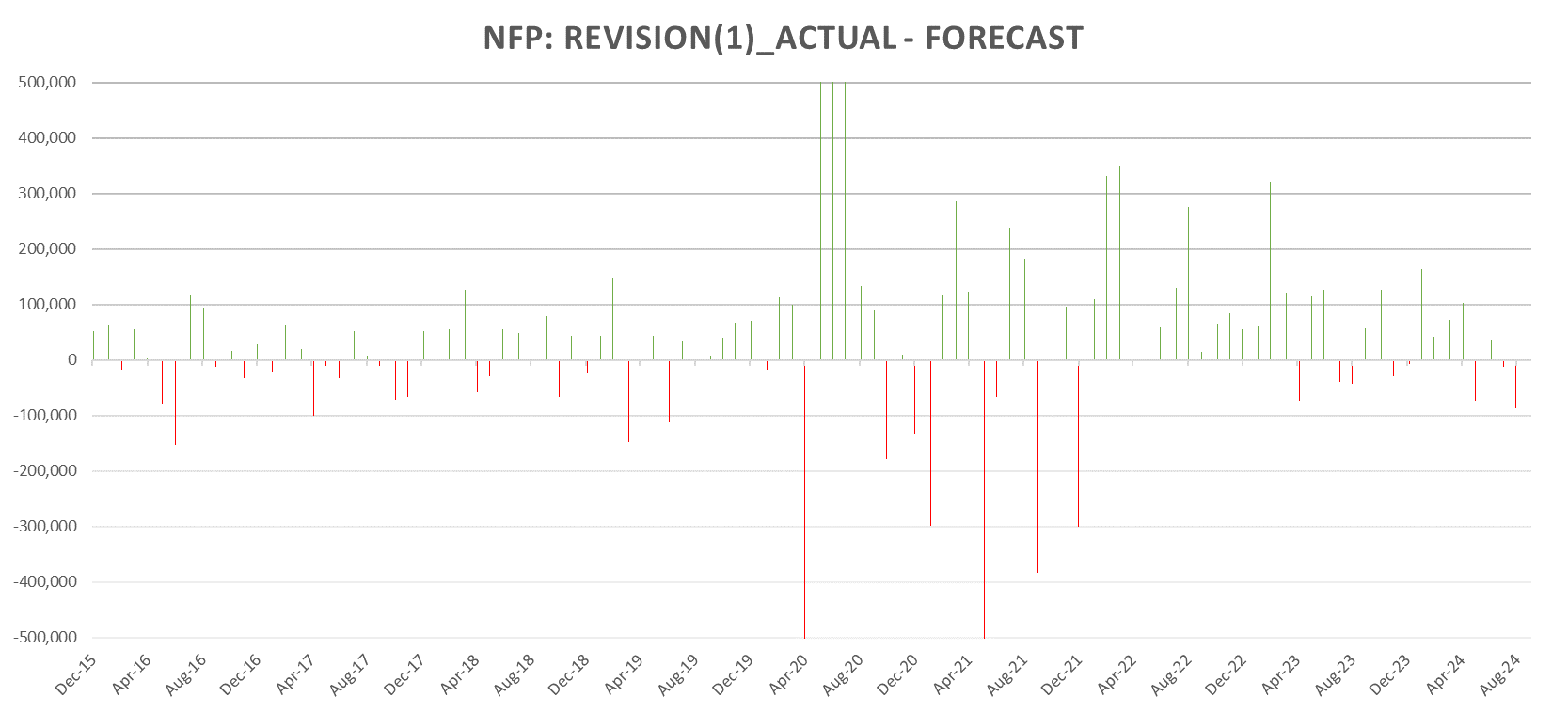

Lets look at some NFP data going back to 2016:

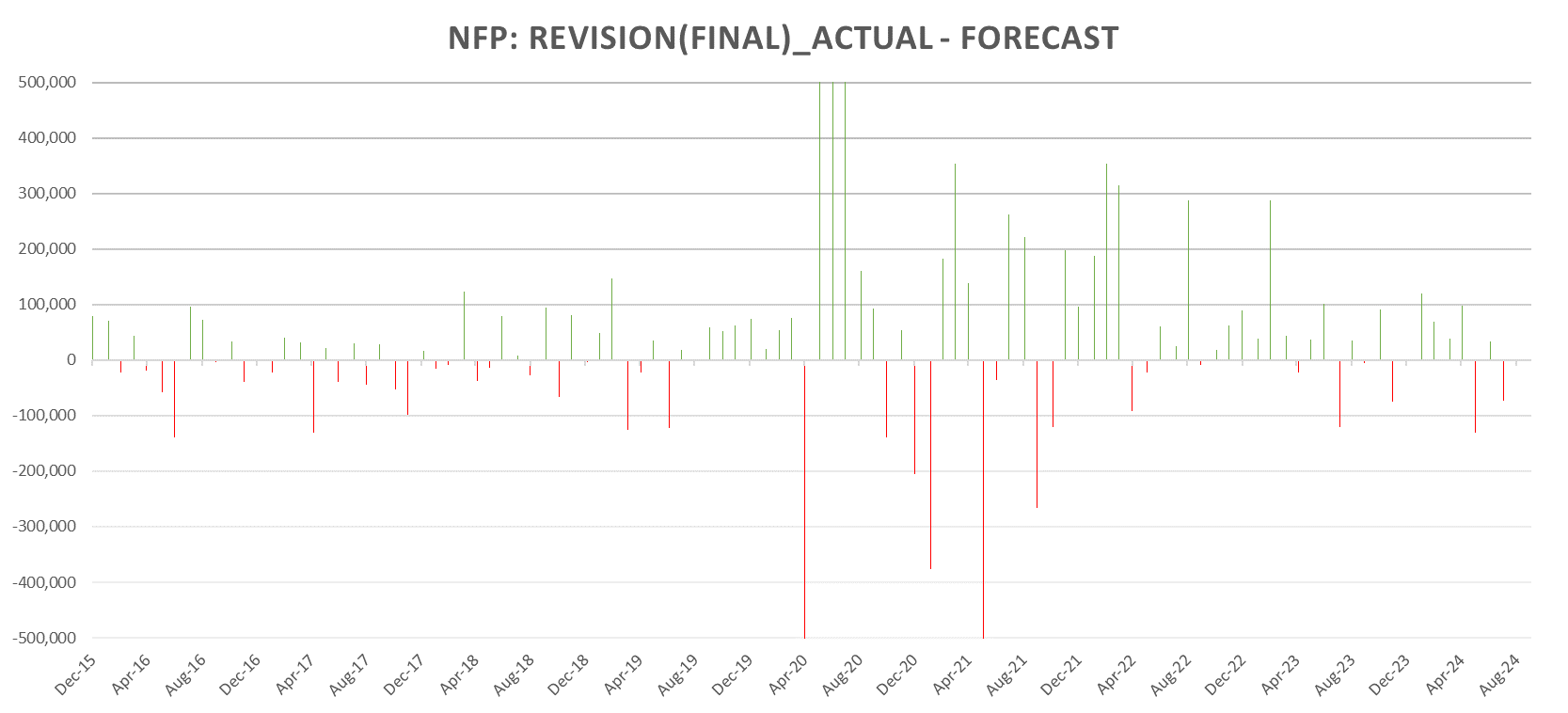

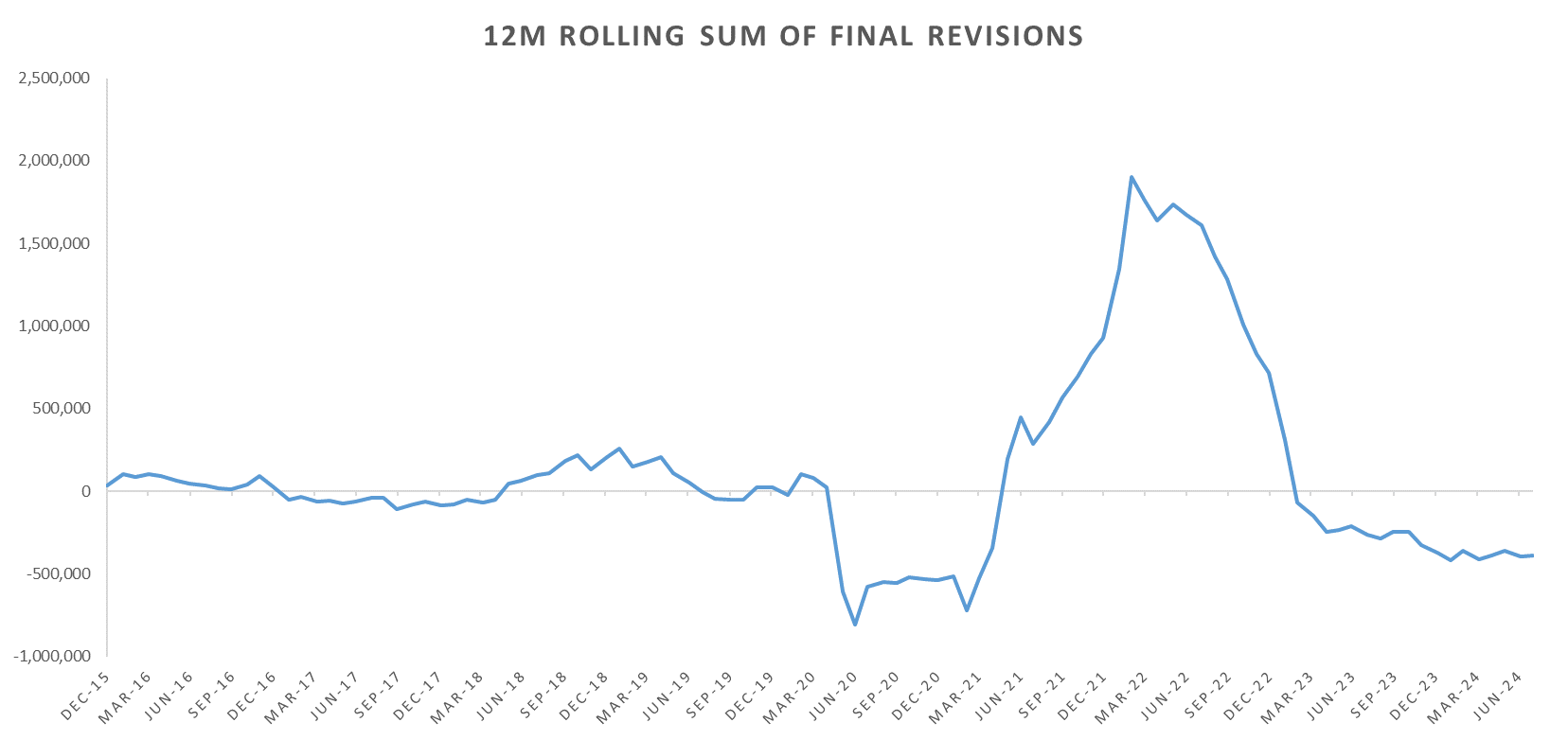

Looking at the final revision sum:

So, lets see how SPX performed during the various periods since 2016:

Current 1-DTE Straddle priced ~100bps, around 10 bps lower than the September & August NFP day straddle (bit surprising.)

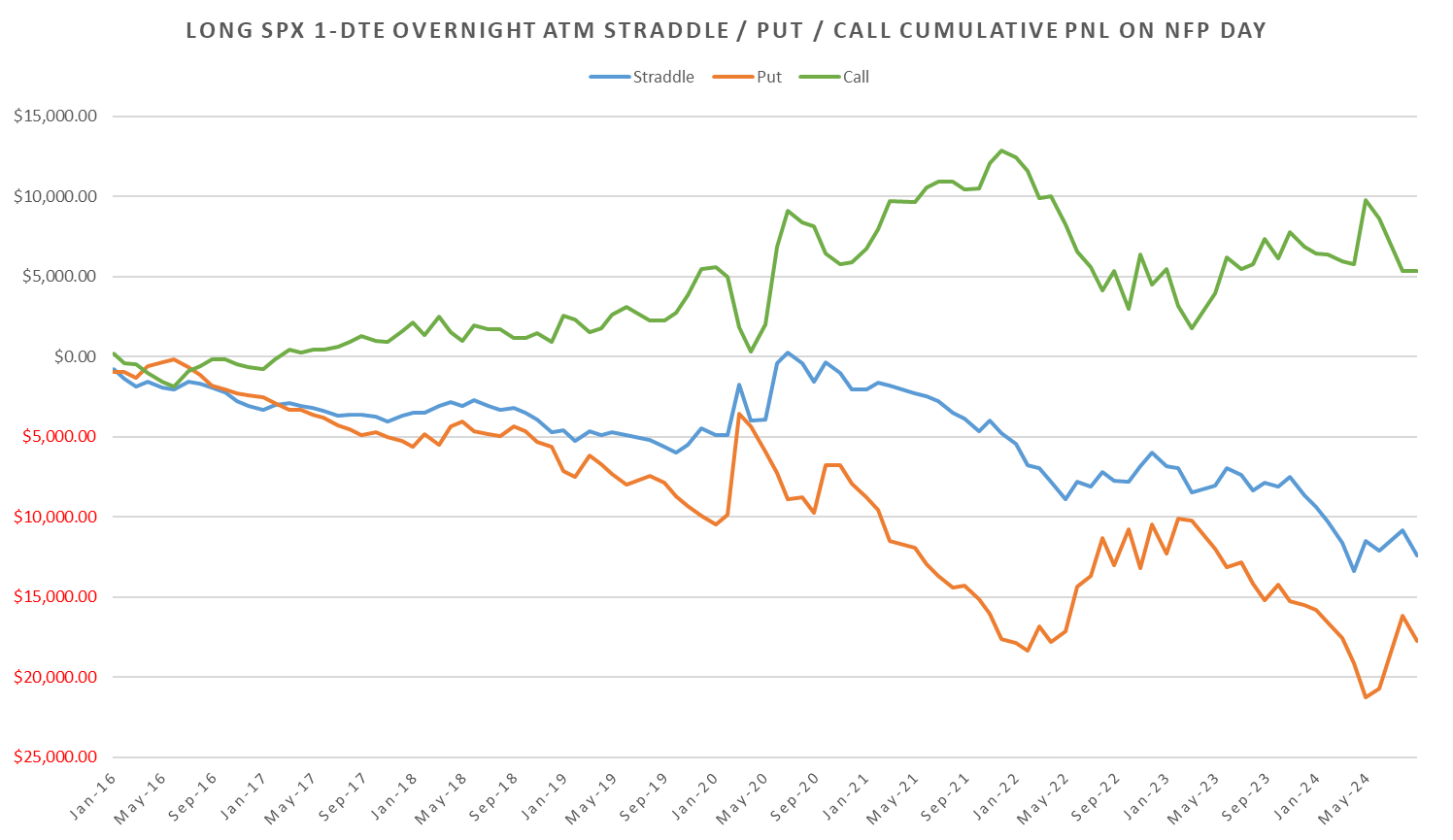

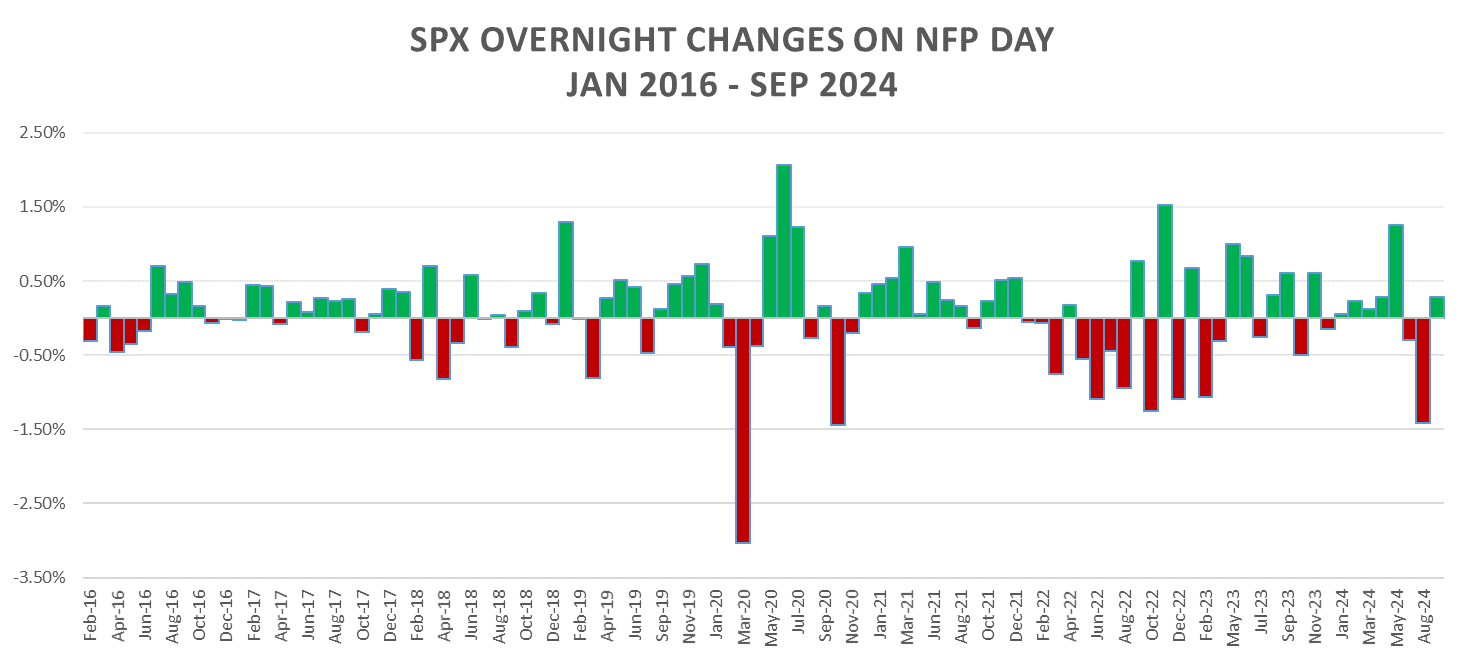

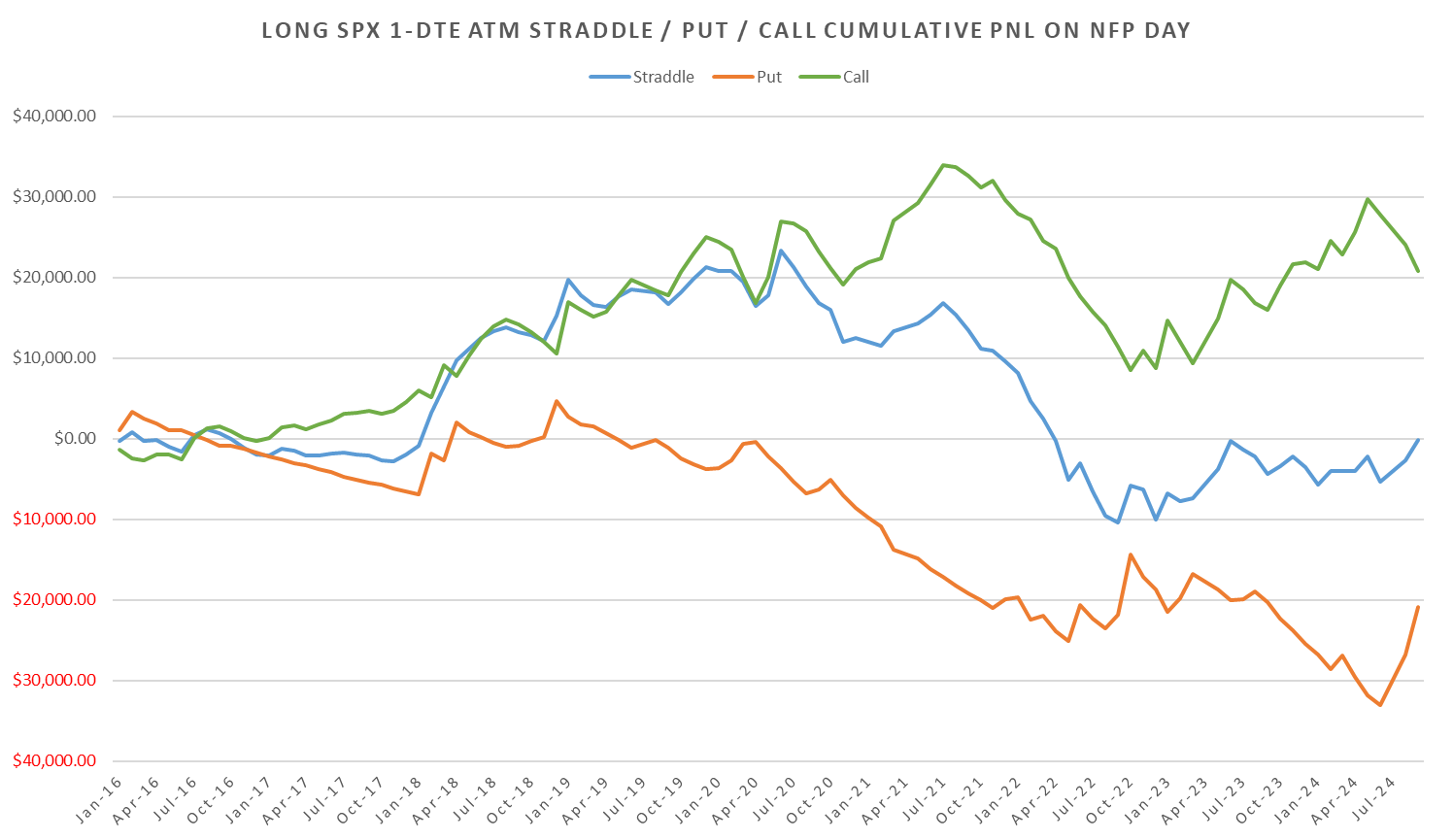

Overnight performance of the straddle (captures the data release):

Outside of 2020, event premium way too rich throughout the various macro outlooks.

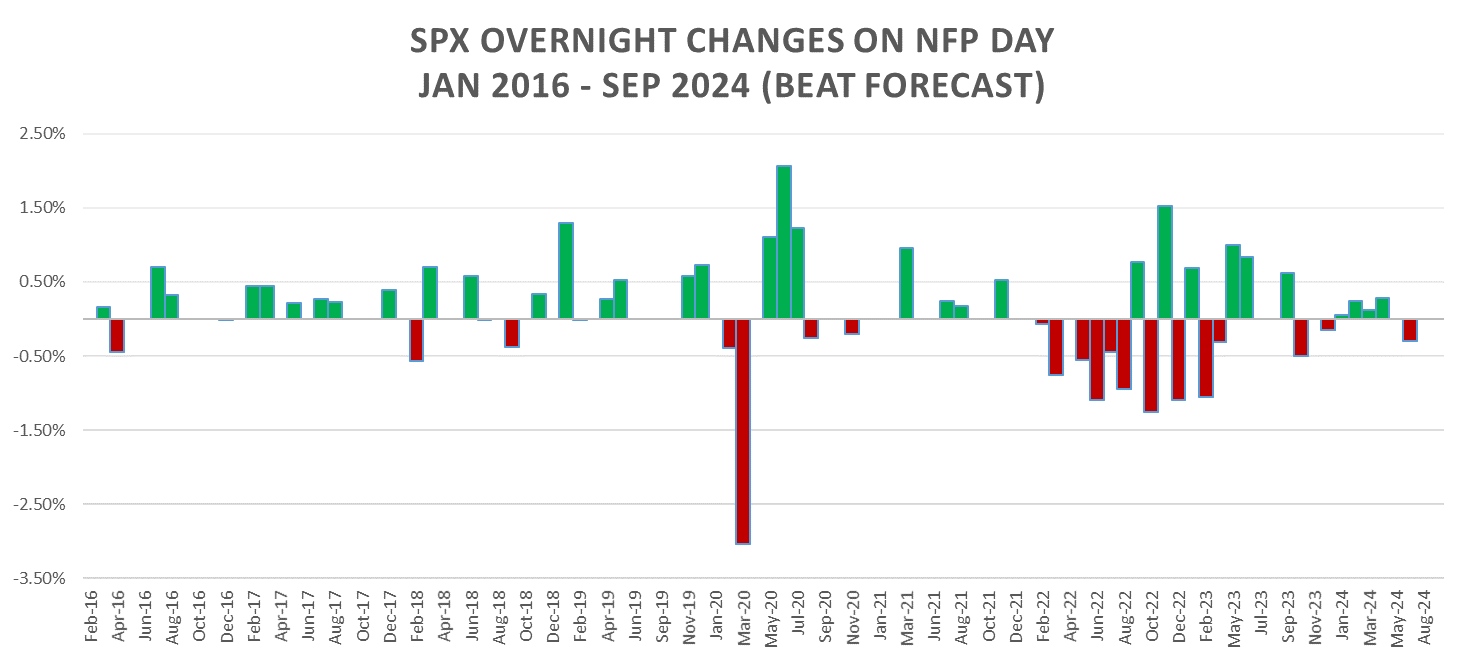

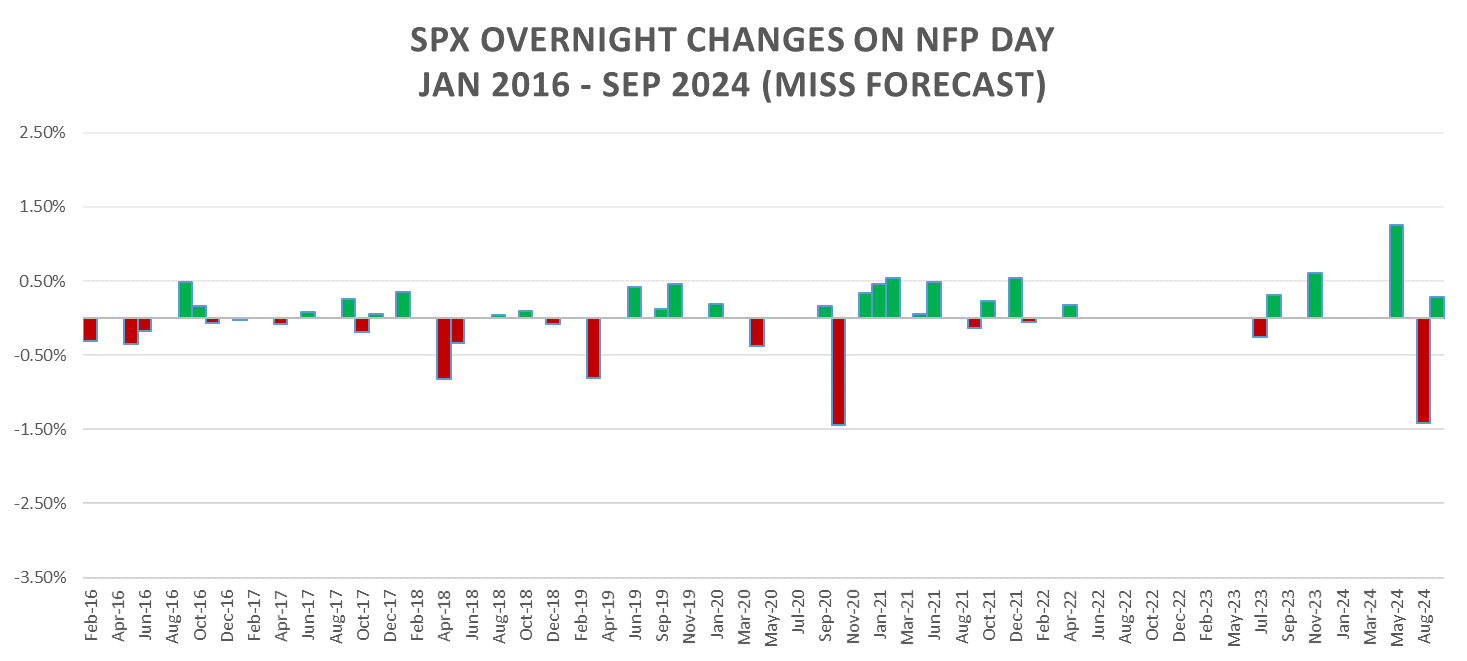

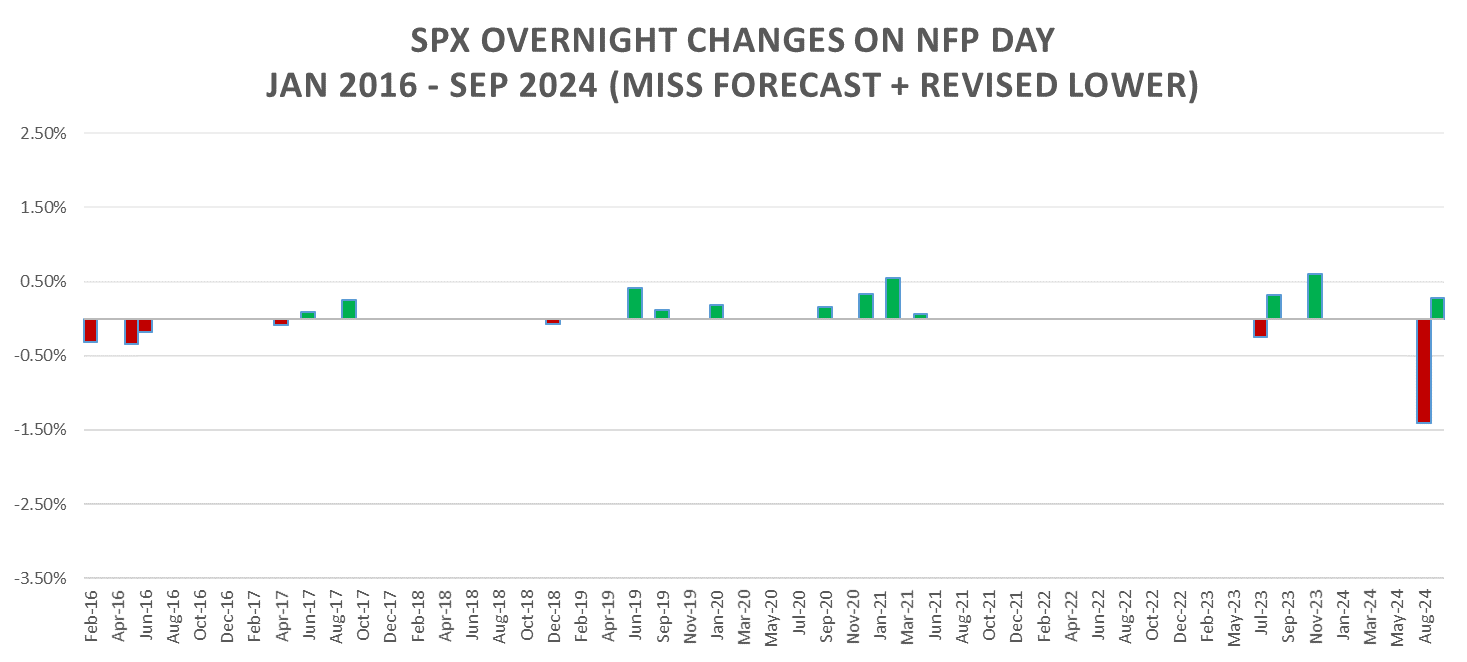

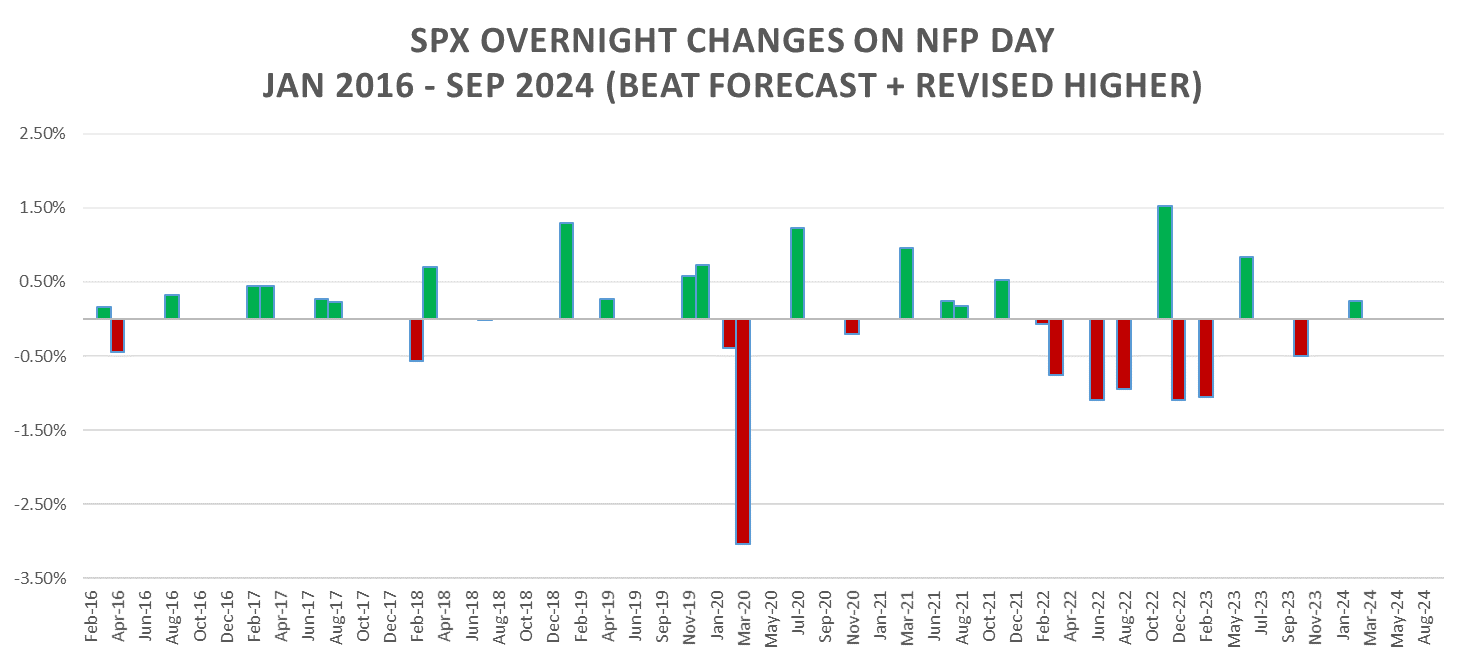

Sorting by beat/miss:

Additionally sorting by Beat/Miss + Up/Down Revision:

Yeah… you could have the #’s a week in advance, still wouldn’t help you!

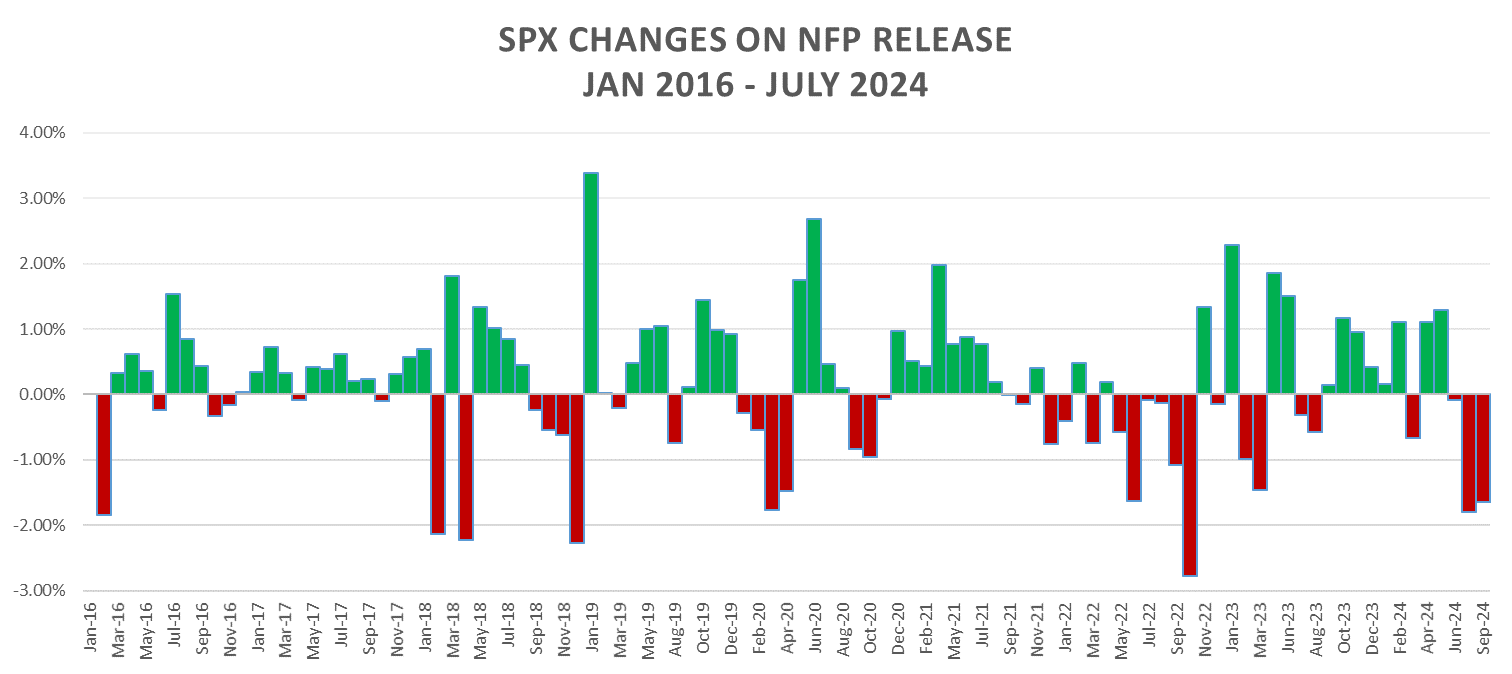

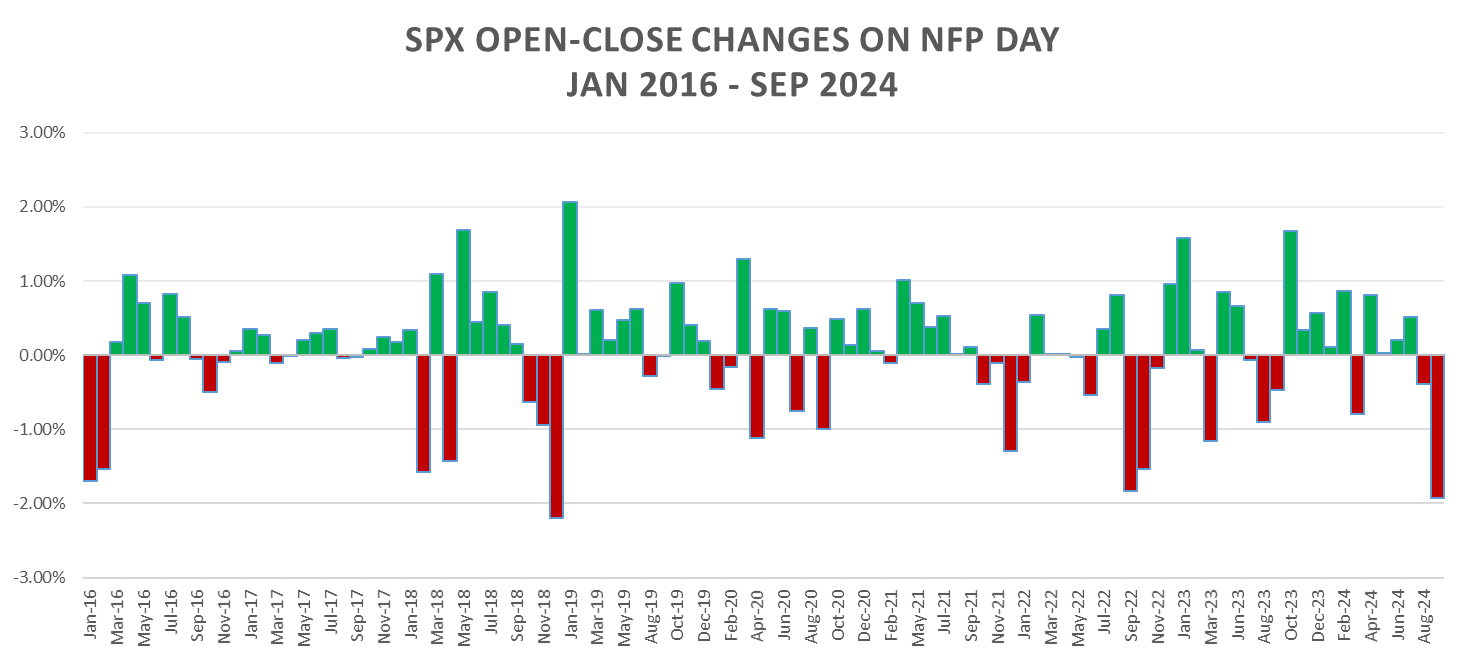

Looking at the full day performance:

Lately a trend day up/down into the close. Holding 1-DTE Straddle till close not losing since 2022.

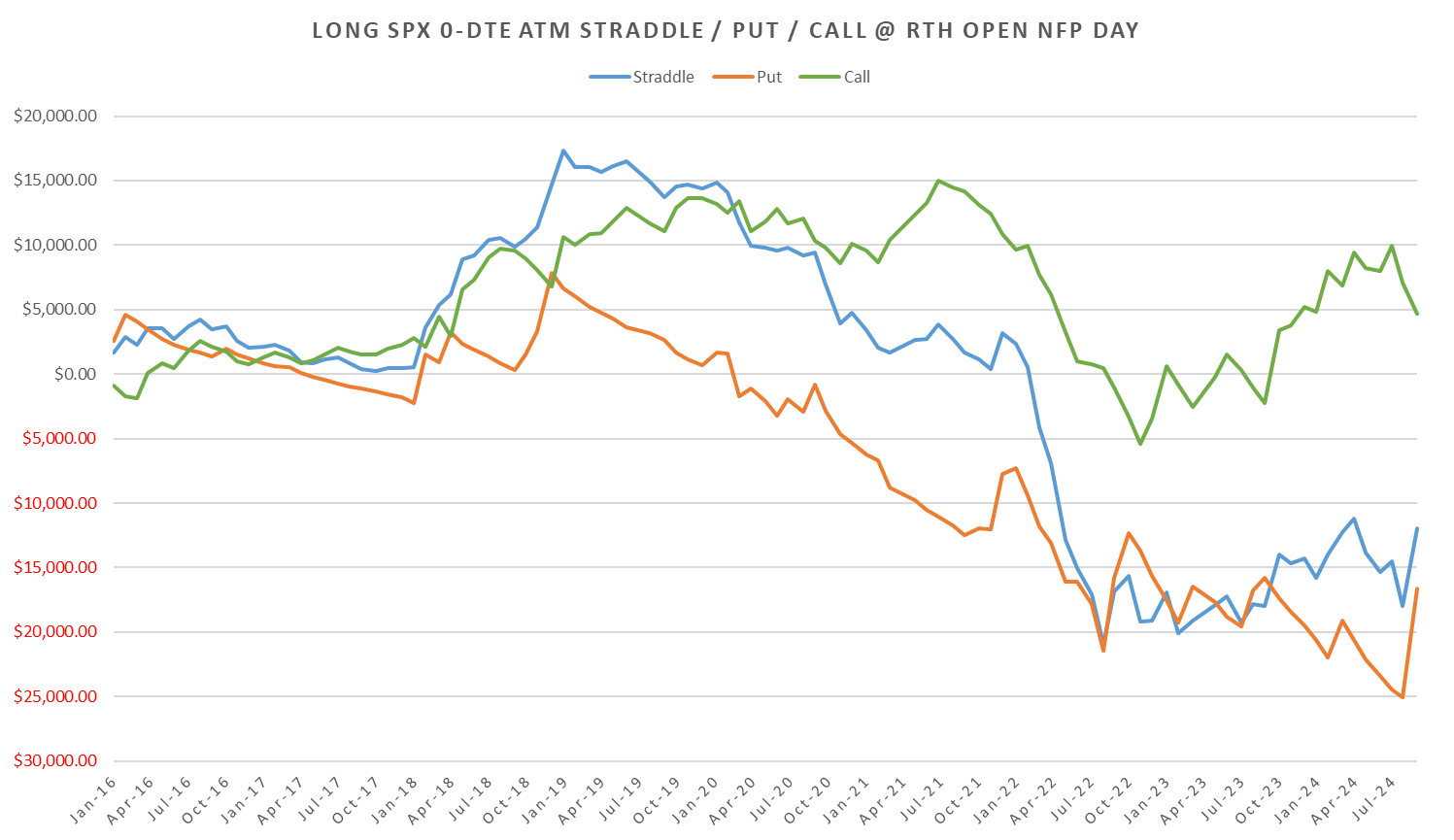

Opening straddles at RTH open after event premium deflates:

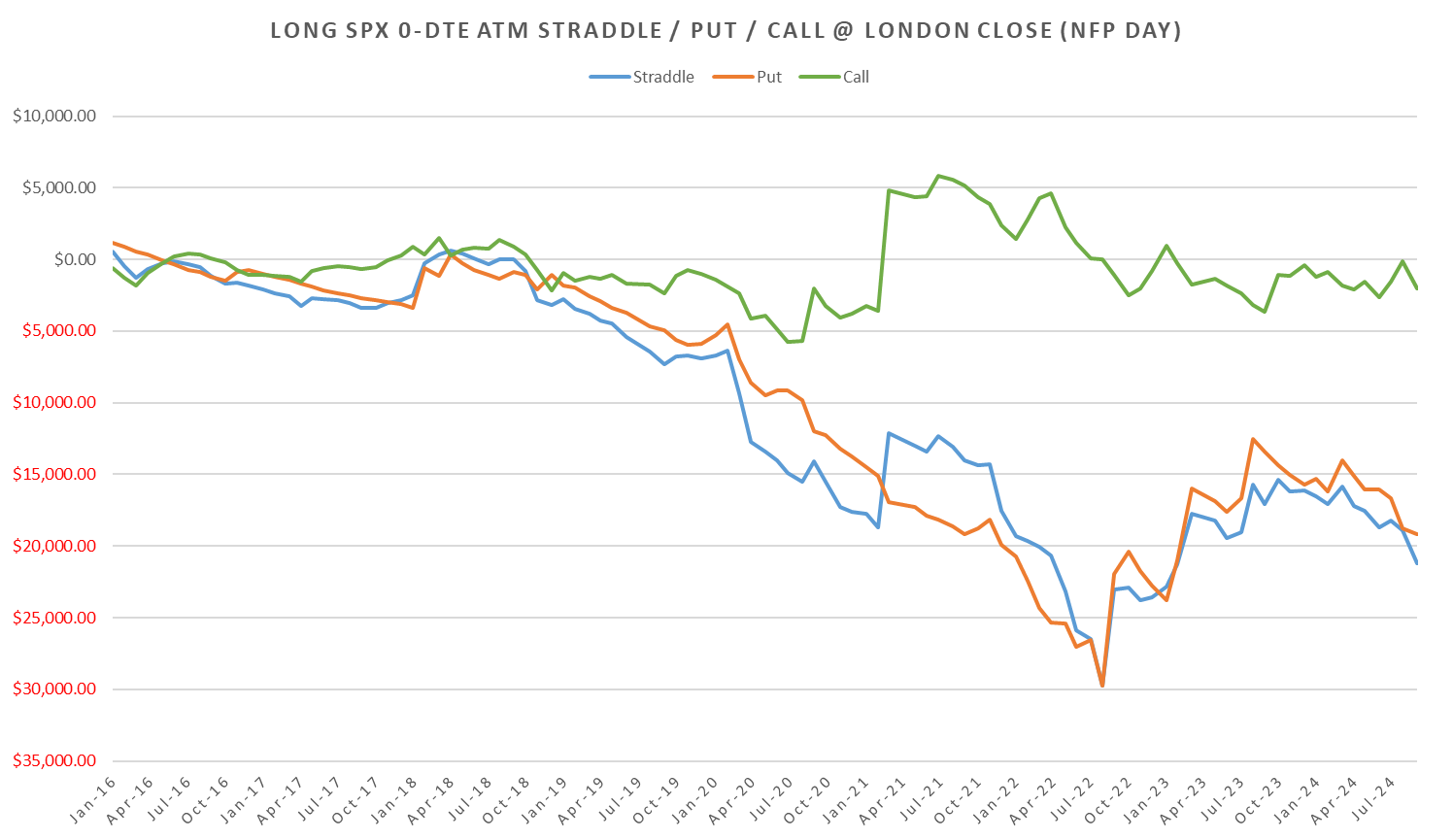

London Close Straddles:

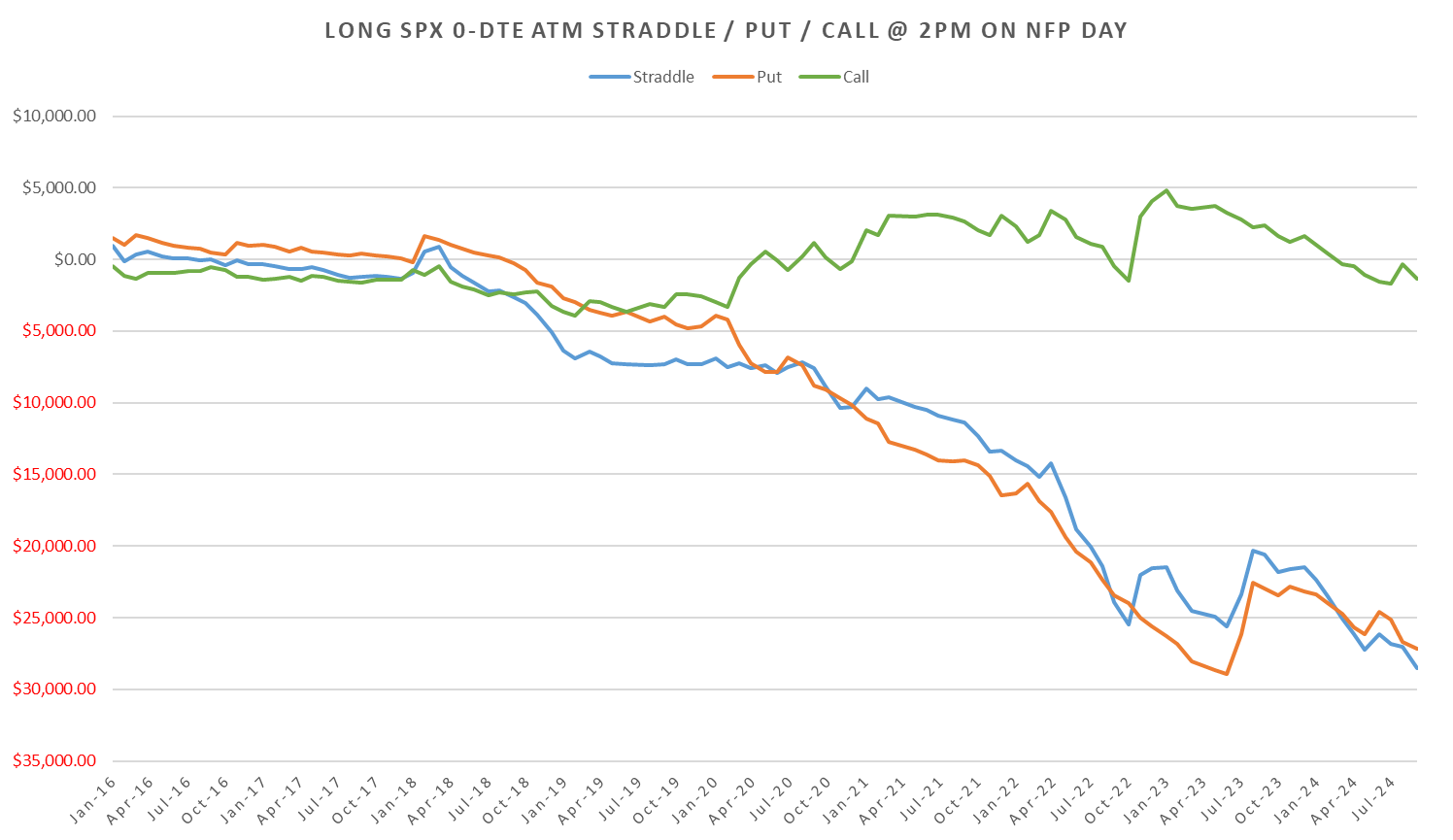

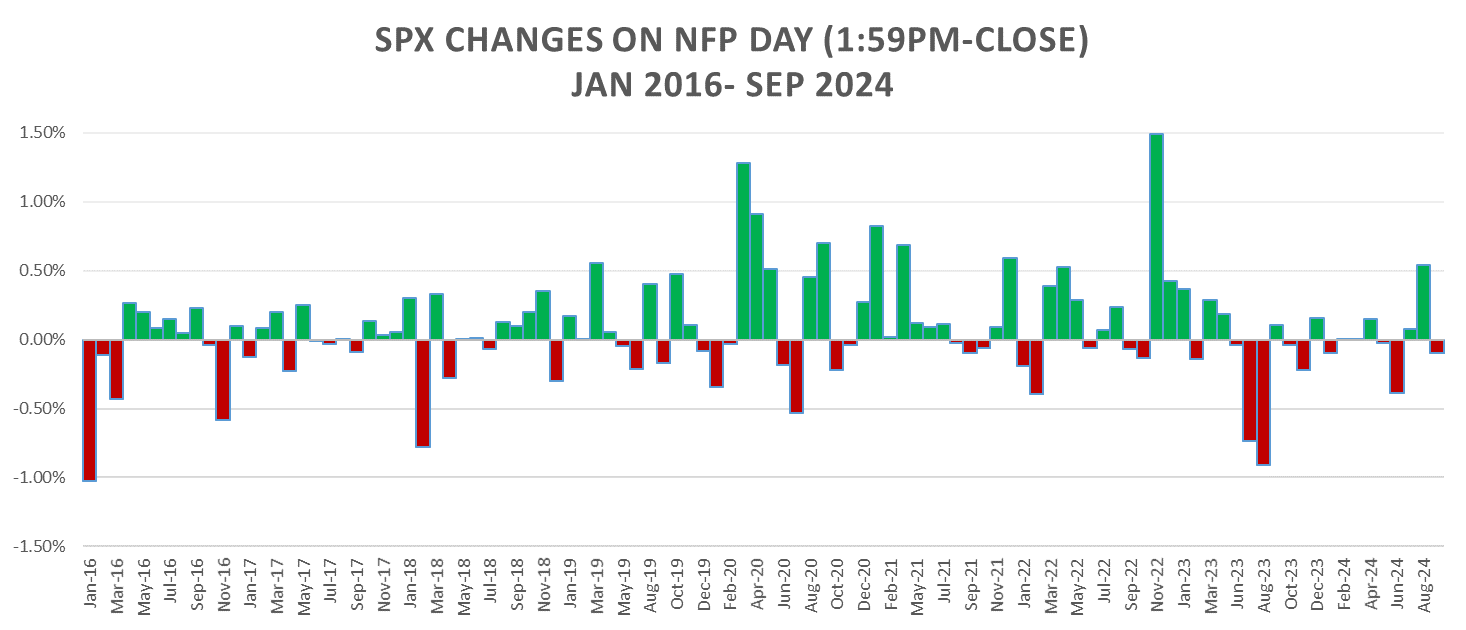

2pm-Close Straddle:

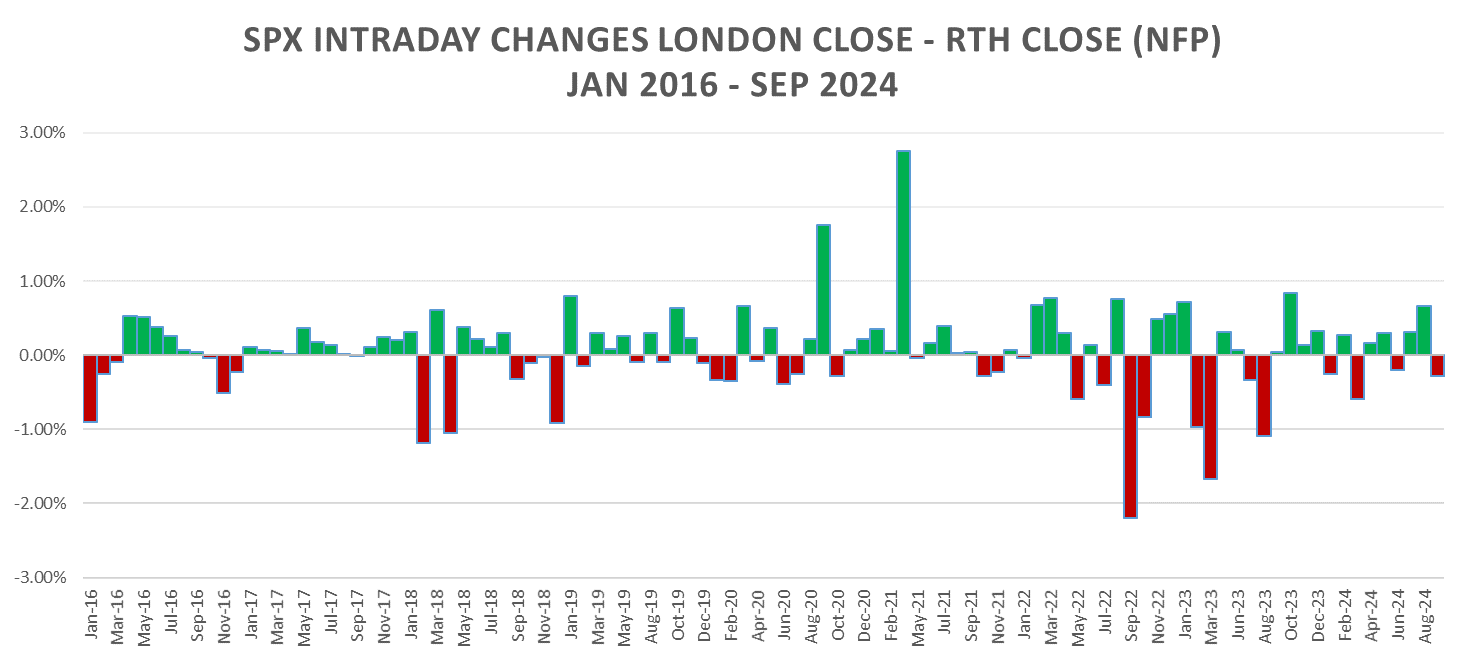

EoD skewed bullish in 2020 & 2022 but lately just relatively flat. Middle East headline risk over weekend should prevent strong upside move into close.