Maybe markets take a breather after OpEx...

A look at market performance surrounding monthly(quarterly) option expirations through options

Following our brief overview of SPX option performance on monthly(quarterly) OpEx, lets take a closer look at some intraday patterns and see if there’s anything worth sweating over.

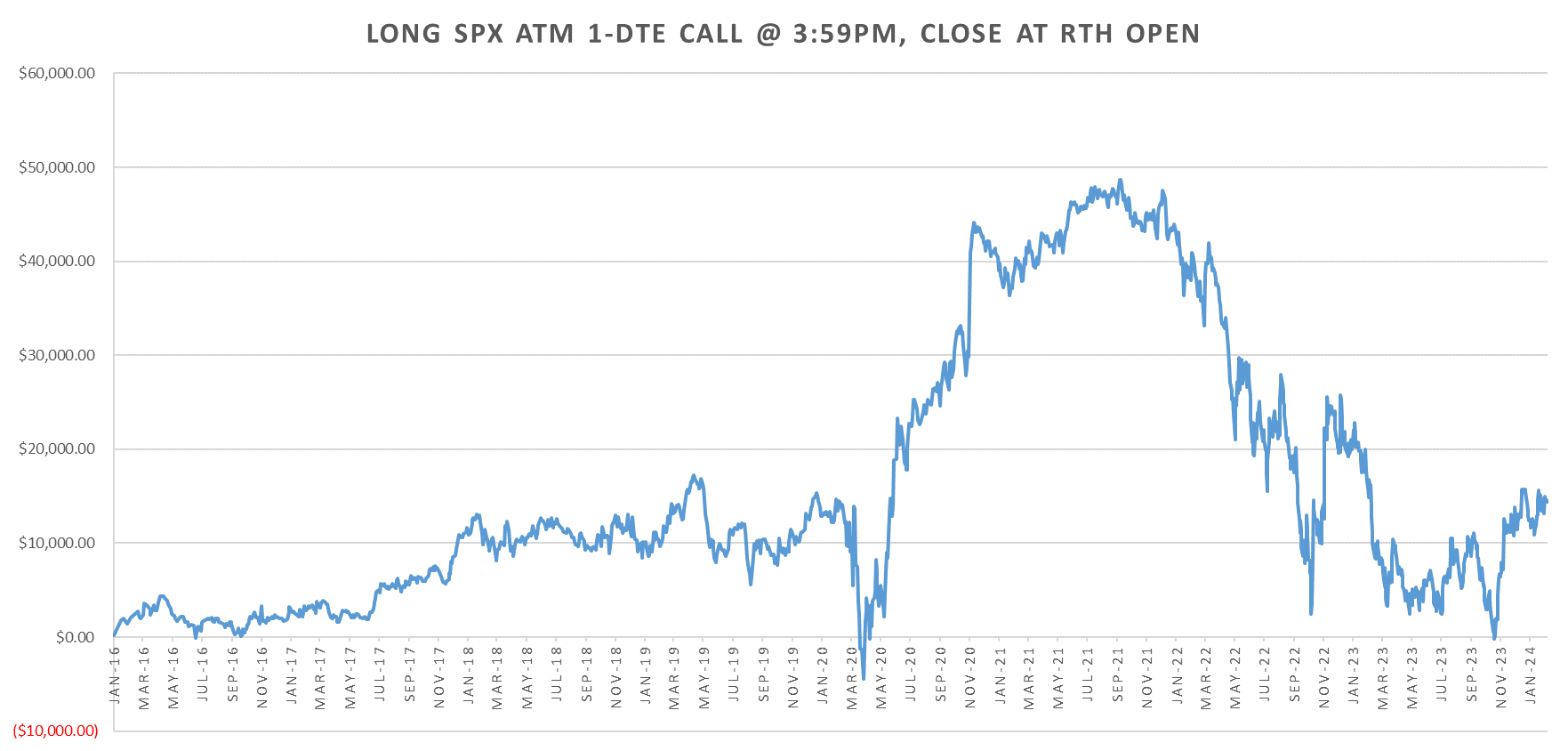

When we break down the overnight/intraday performance we see the jump in call performance around 2020/2021 much in line with overall overnight performance during that period (not just monthly opex.) This ‘excess return’ has been erased in 2022, with pnls stagnating around flat since 2018.

What IS interesting is the regular trading hours (rth) put performance… Unlike the general Friday template calls during rth have barely seen any positive ‘excess return’ runs since 2017 and that includes the overwhelmingly bullish performance of last couple of years.

Post ‘London Close’ puts were exciting up until Jan2022… after which for some reason puts have struggled to make any money on OpEx days at all, with calls performing slightly better than puts last year and a half (but not really any stability to any of these trades.)

Lastly, lets take a look at the possibility of March quarterly OpEx being the turning point for this rally. In line with what we saw this week going into OpEx, markets look sluggish, initial ramp on Mon/Tue following by drip on Wed/Thu. The 7-DTE charts plot the final PnL of the trades opened on the Friday prior to monthly OpEx and held till expiry on the Friday of monthly OpEx.

Keep reading with a 7-day free trial

Subscribe to Vol Vibes to keep reading this post and get 7 days of free access to the full post archives.