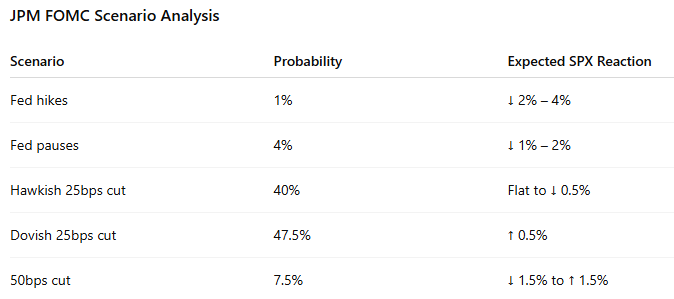

Markets taking a breather after last weeks ramp into FOMC tomorrow. JPM lays out the scenario analysis:

So most likely scenario ~ flat…

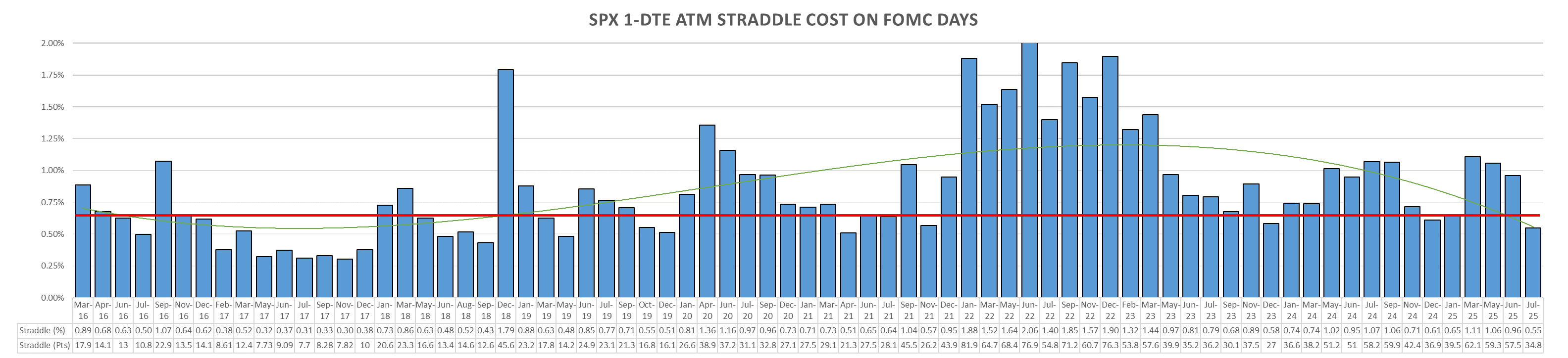

SPX 1-DTE Straddle ~65-70 bps for tomorrow, higher than July but still near lows for the 2020+ period.

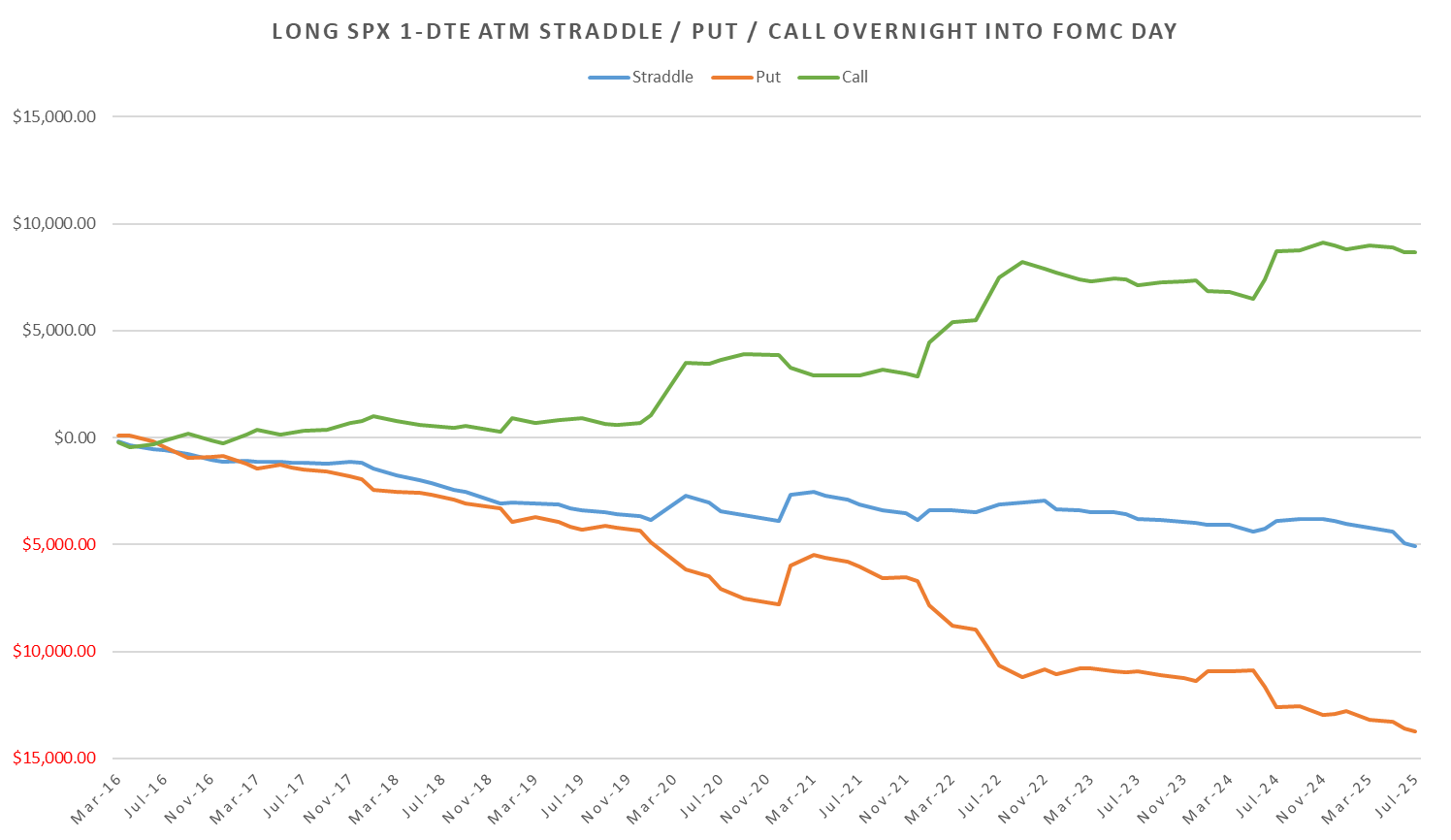

Updated 1-DTE & Intraday SPX Straddle performance:

Note: All charts represent $200k notional bet size (ex. ~3 XSP at 6000 SPX)

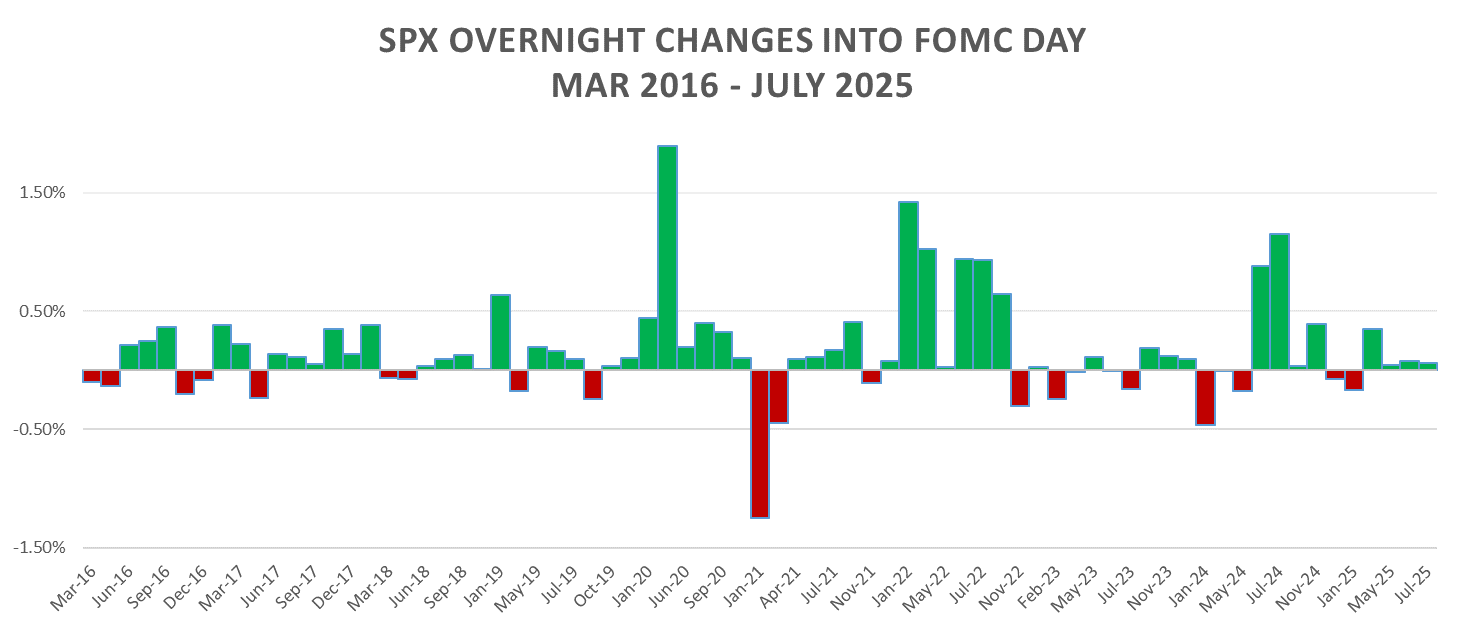

1-DTE

Overnight Straddles

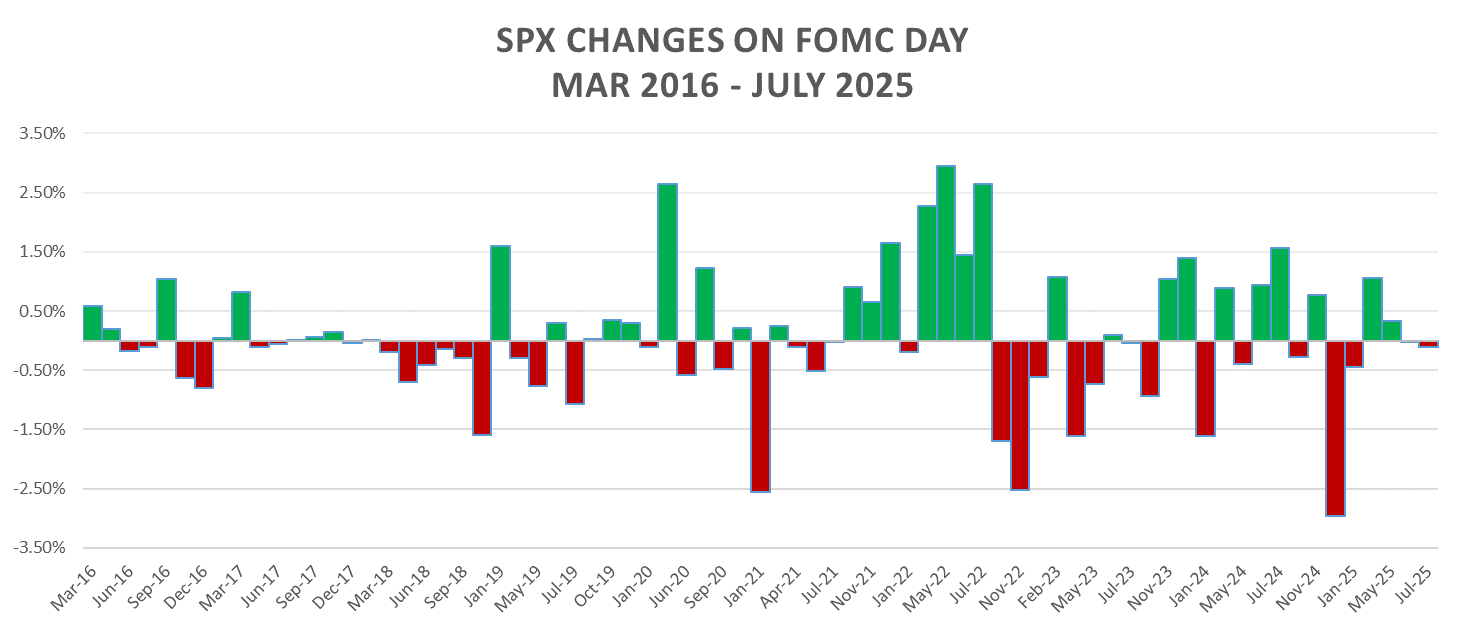

The ol’ reliable drift up into FOMC…

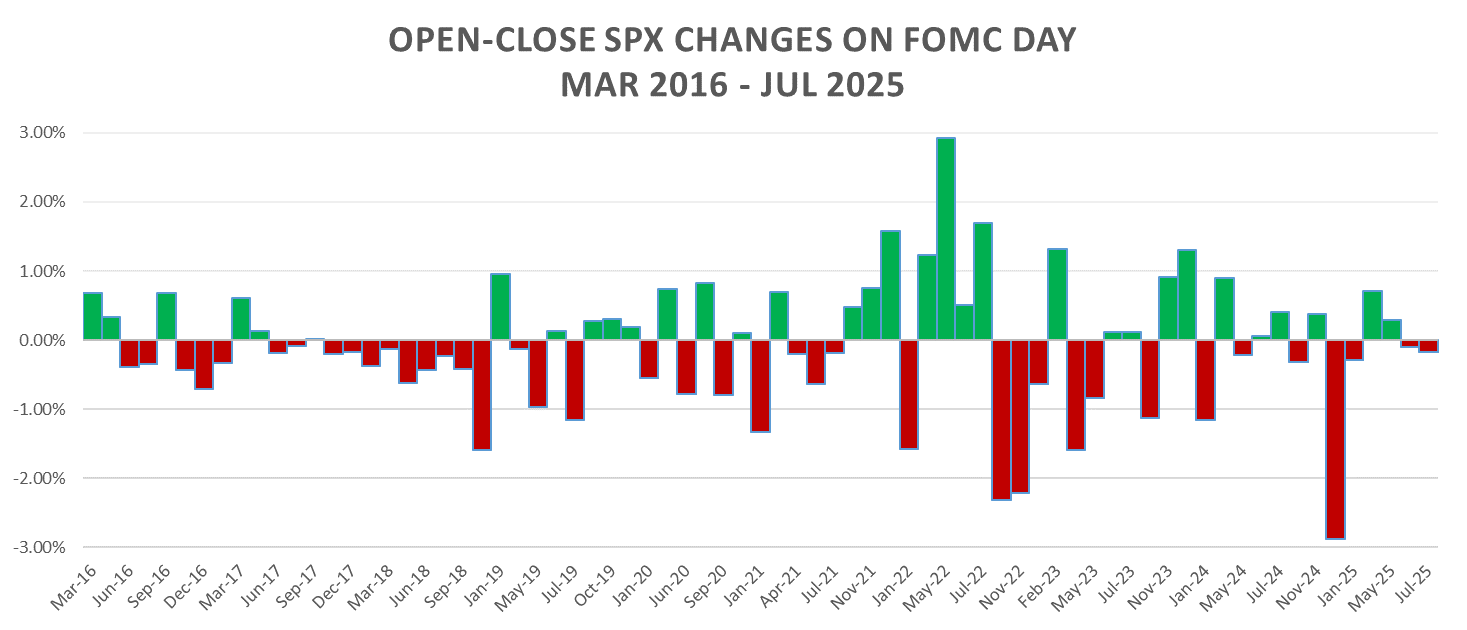

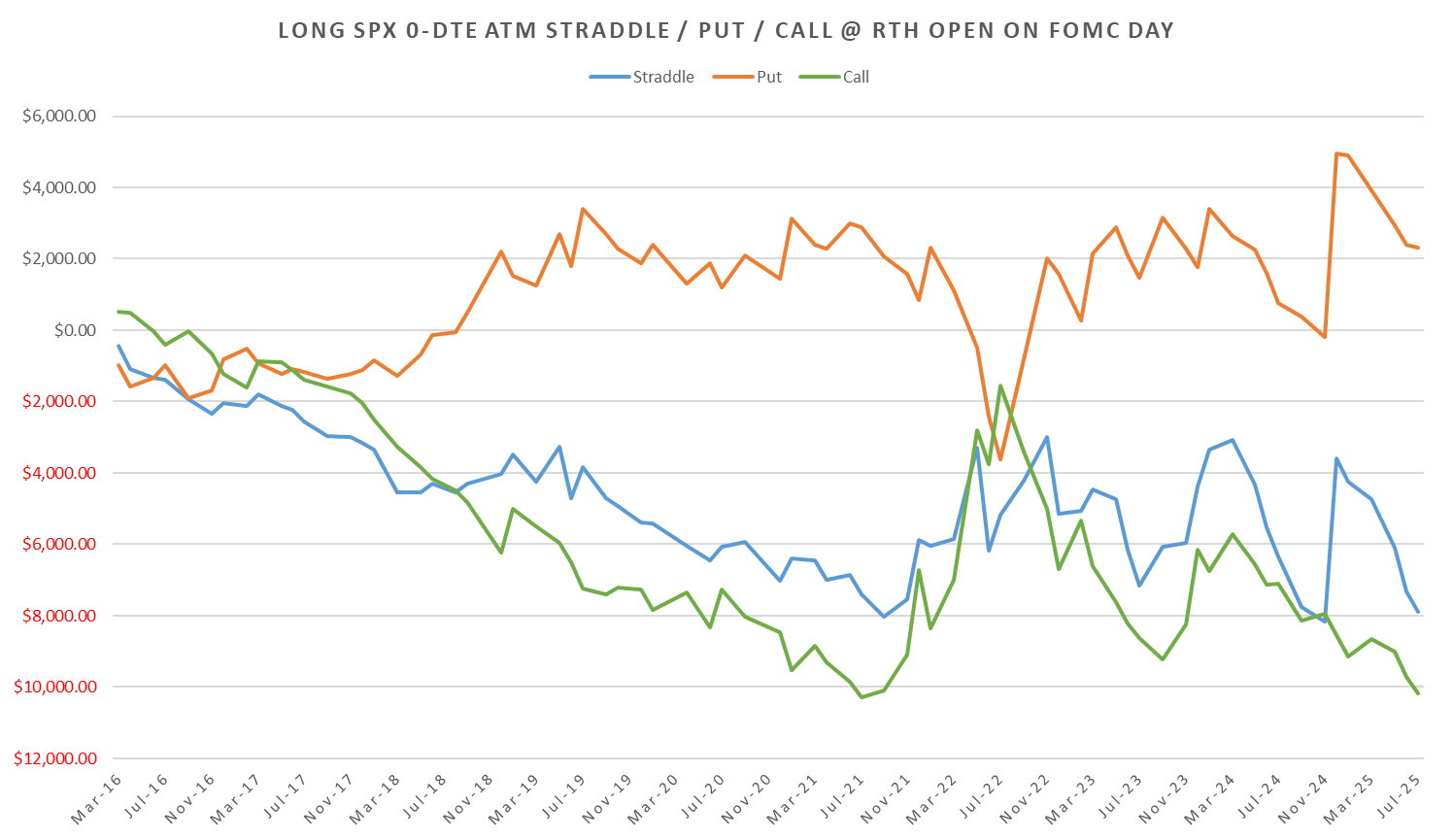

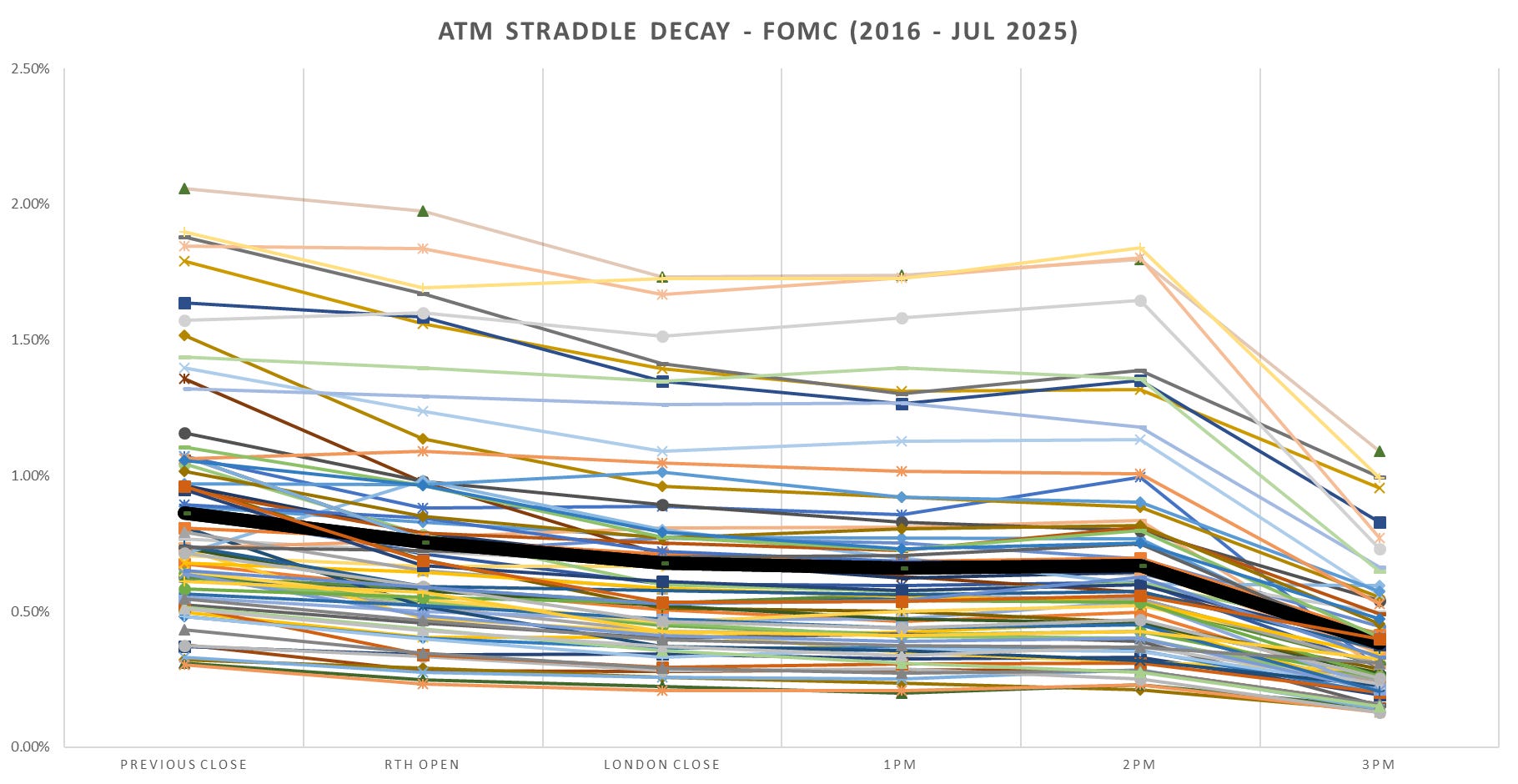

RTH Straddles

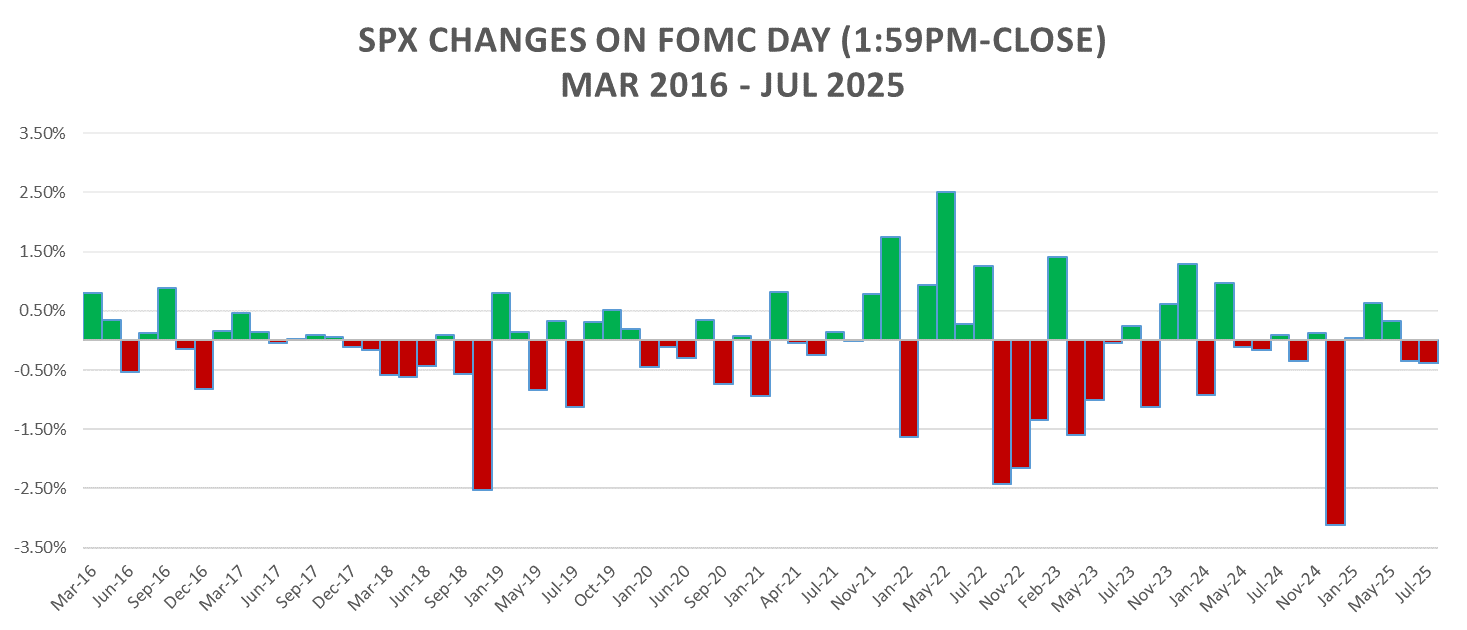

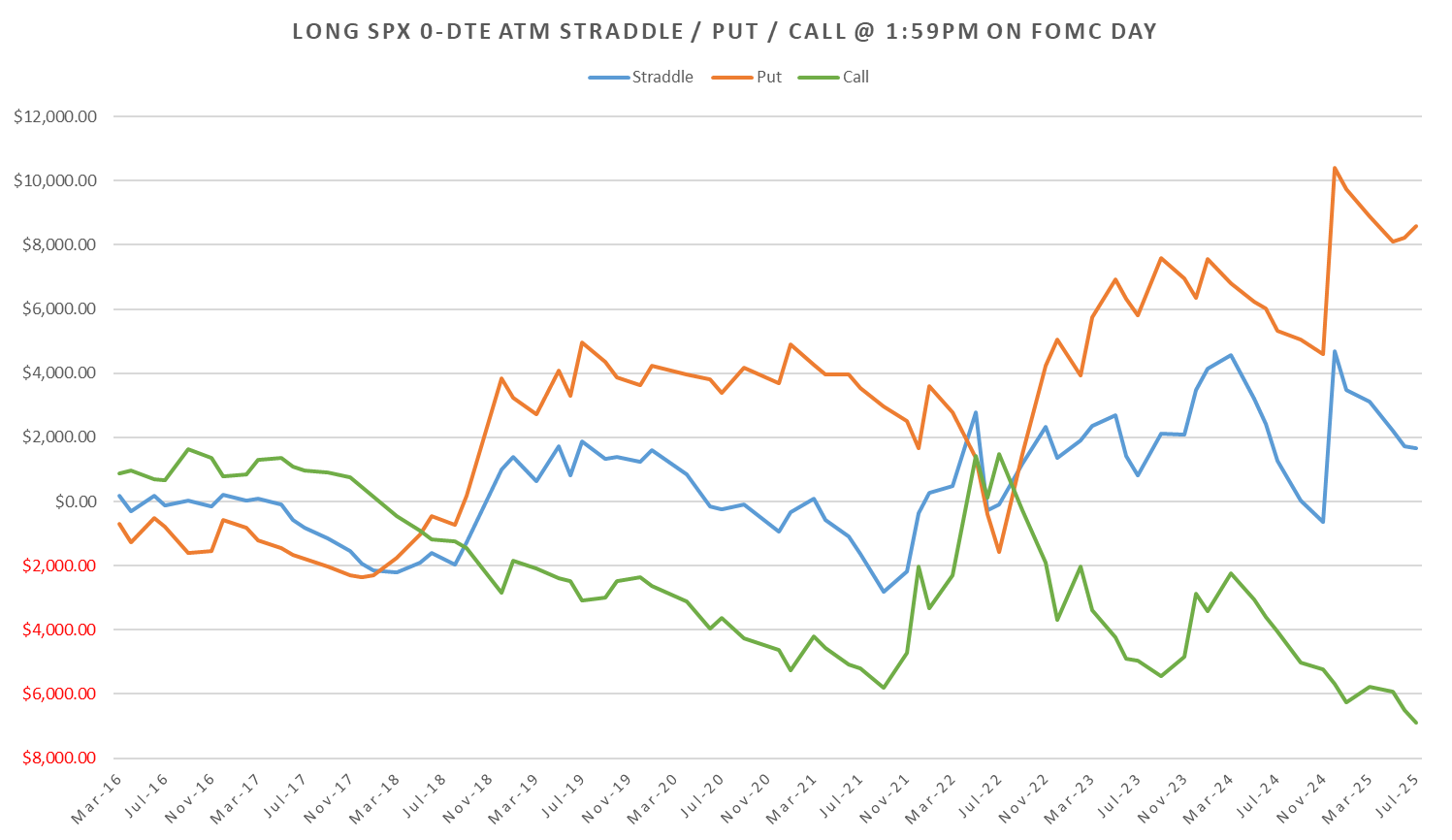

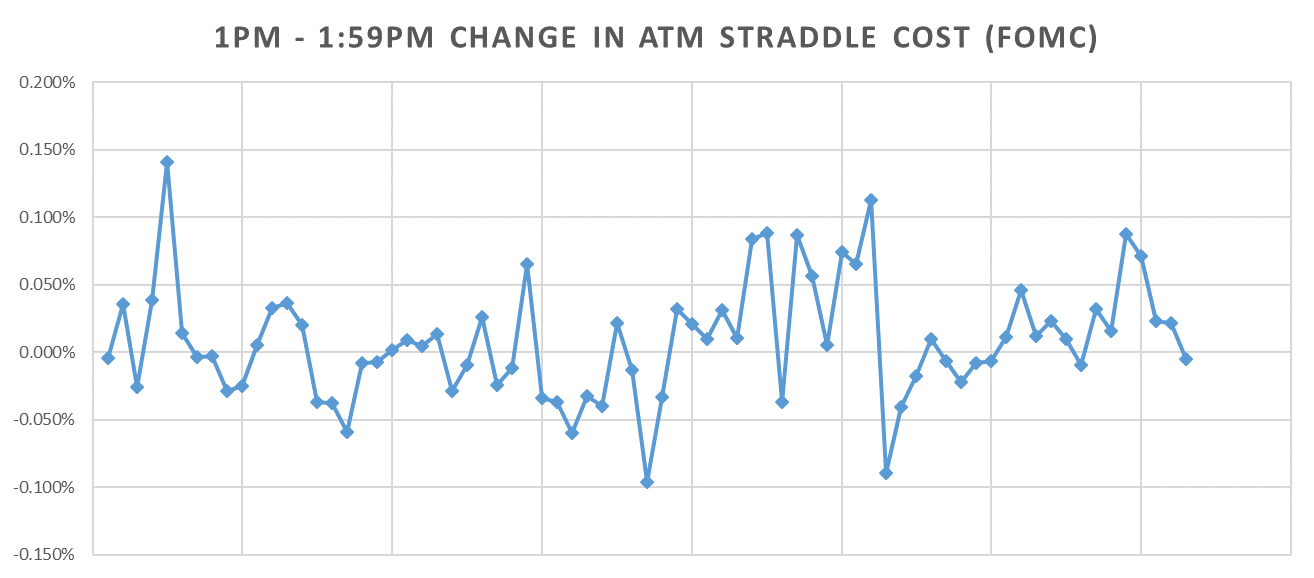

1:59pm

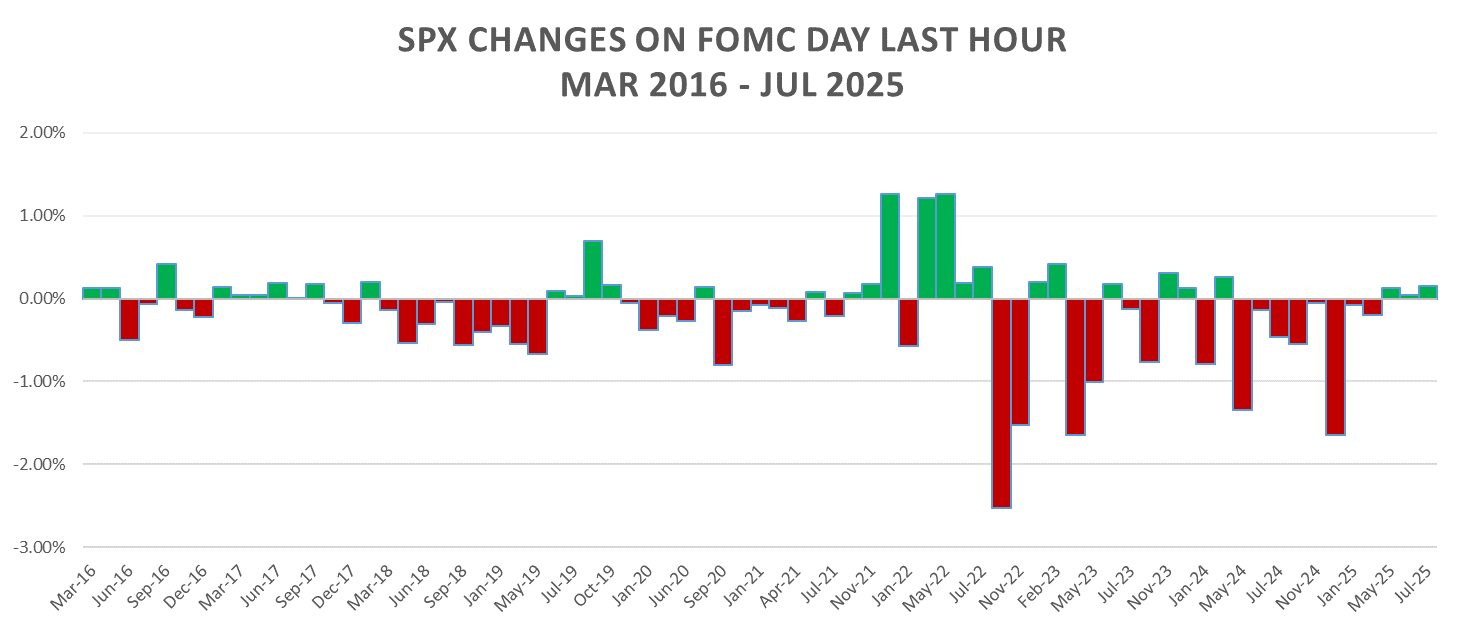

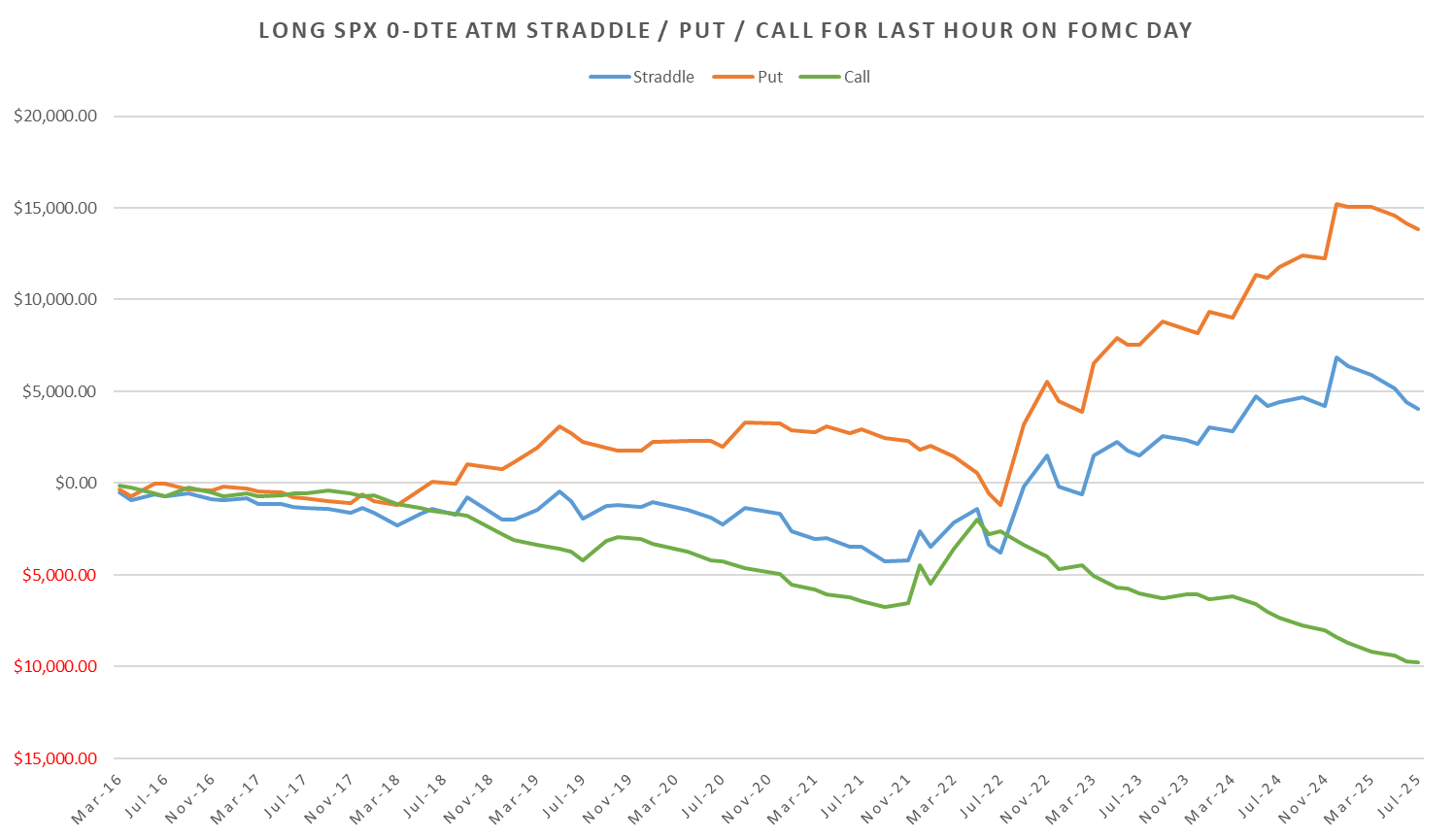

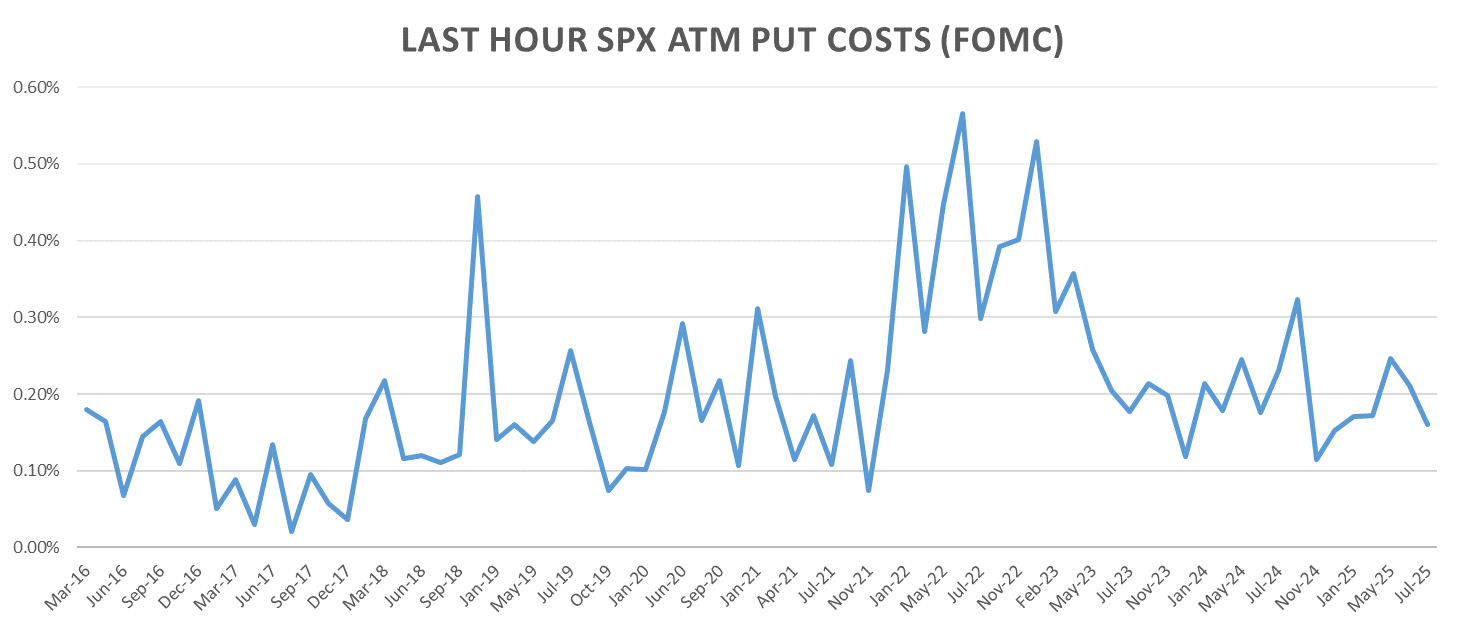

Last Hour

Last hour SPX put cost %:

Intraday Straddle Cost - Hourly

Still seeing a bit of a bump in vols an hour before FOMC.

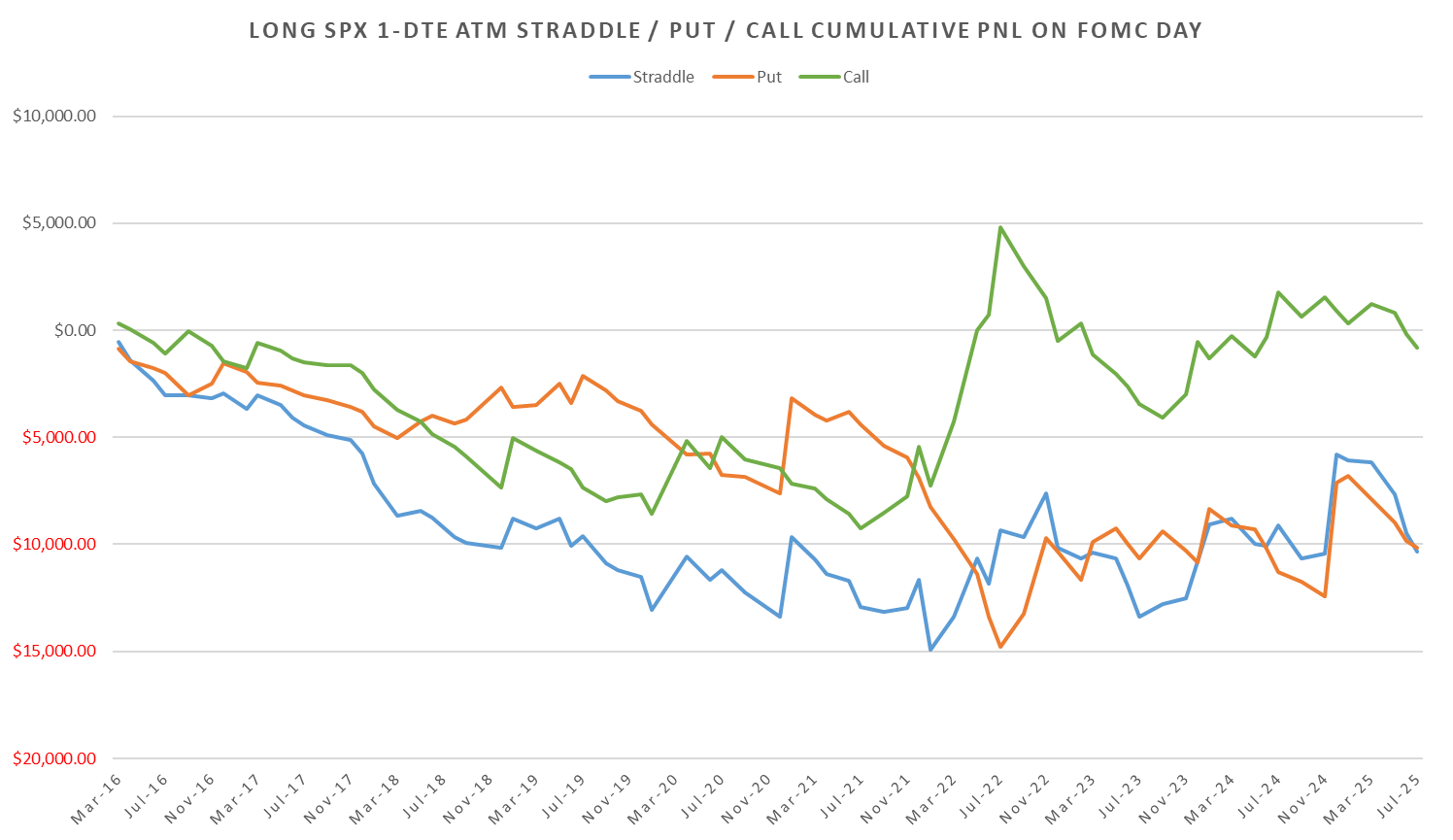

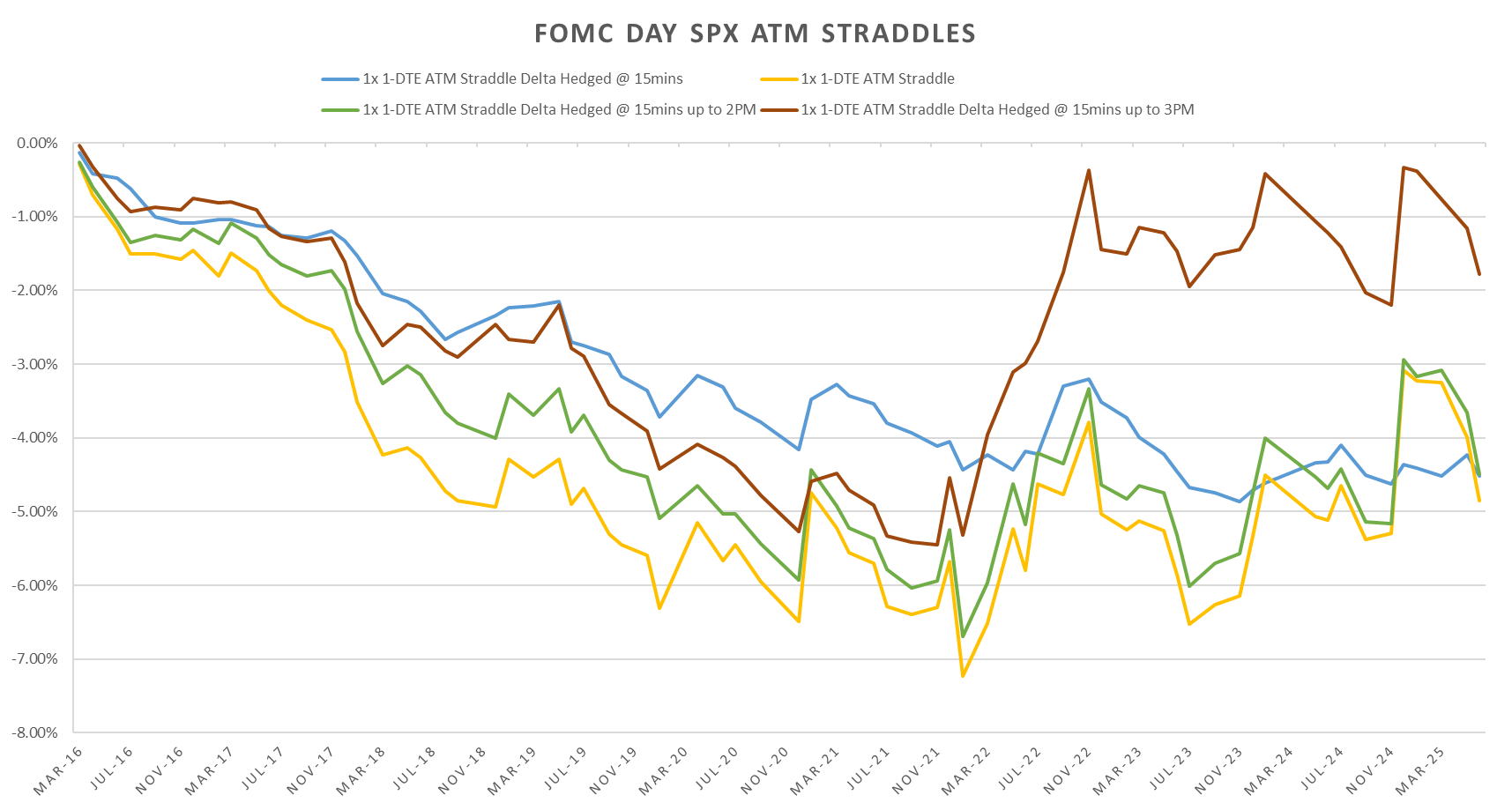

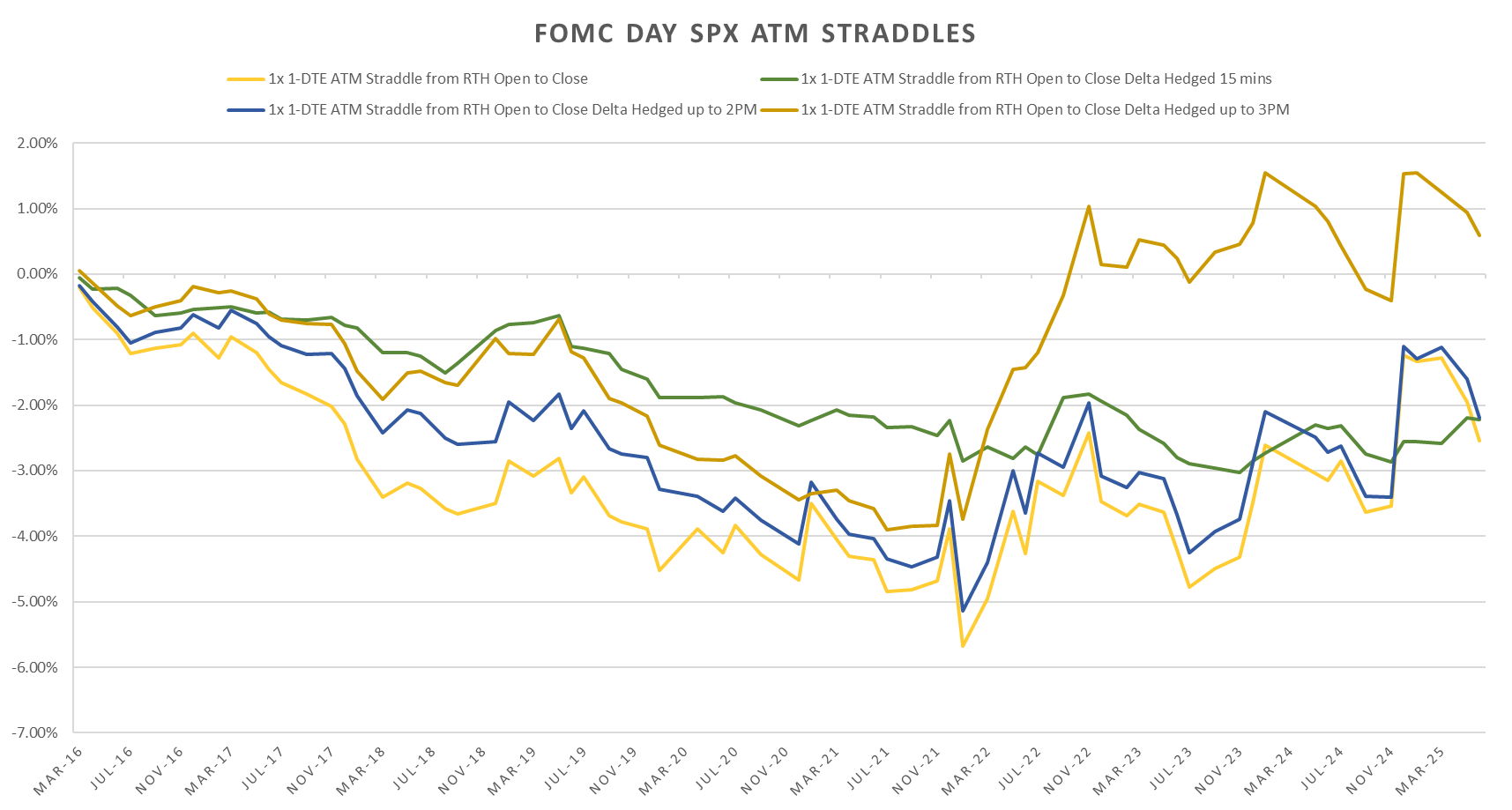

Delta Hedged Straddle Performance

Comparison between between unhedged long 1-DTE SPX straddle & the various delta hedging schemes. Post 2022, as expected given the dominance of last hour vol, hedging long straddles up to 3pm and then not hedging into eod produces ‘best’ relative performance with all the gains mostly happening ~ mid 2022.

Avoiding the overnight decay and instead buying the straddle at US RTH open actually sees positive performance by a smidge over the 10 year period. Delta hedging up to 3pm then not hedging last hour produces highest pnl.

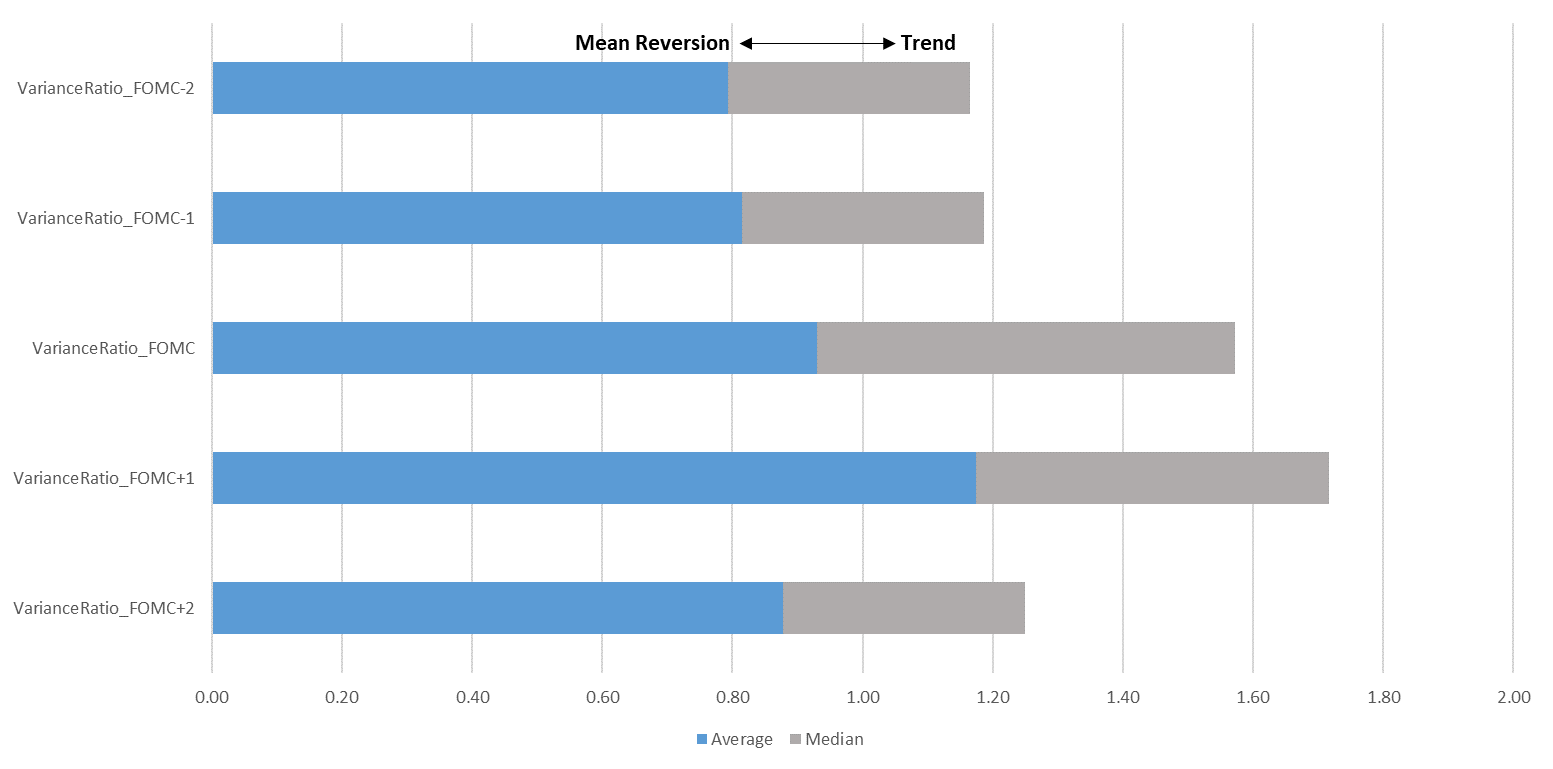

We also tend to see, on average, stronger trend on the day after FOMC which fades by FOMC+2 days (measured using ratio of 5min squared returns to op-cl squared returns.)

Have a great day!