FOMC

SPX Index & Options Performance Update - May 2026

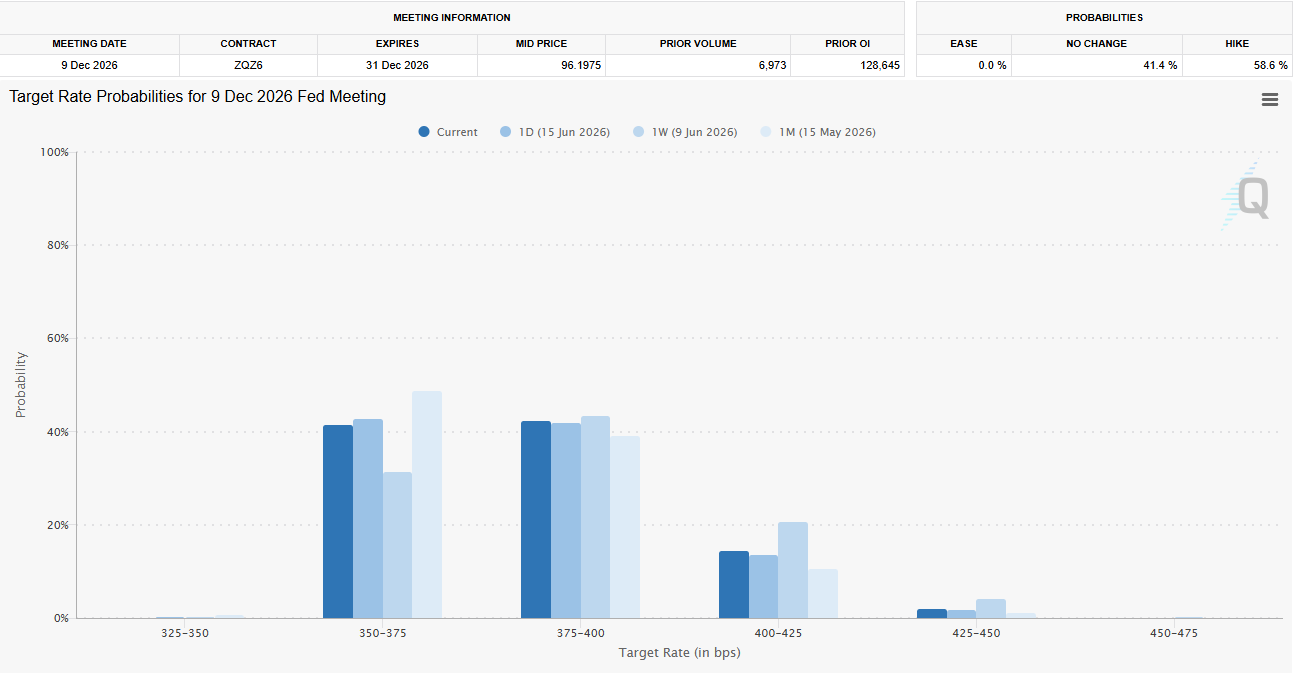

Kevin Warsh will have his first press conference tomorrow as the new Fed chair. While markets are fairly set at ‘no change’ for the meeting tomorrow, the picture for last quarter of the year as well as early 2027 remains unclear:

One thing is clear, market is pricing 0% probability of easing all the way through June 2027 where there is a symbolic 1% chance of easing that picks up slightly (still single digits) into later meetings.

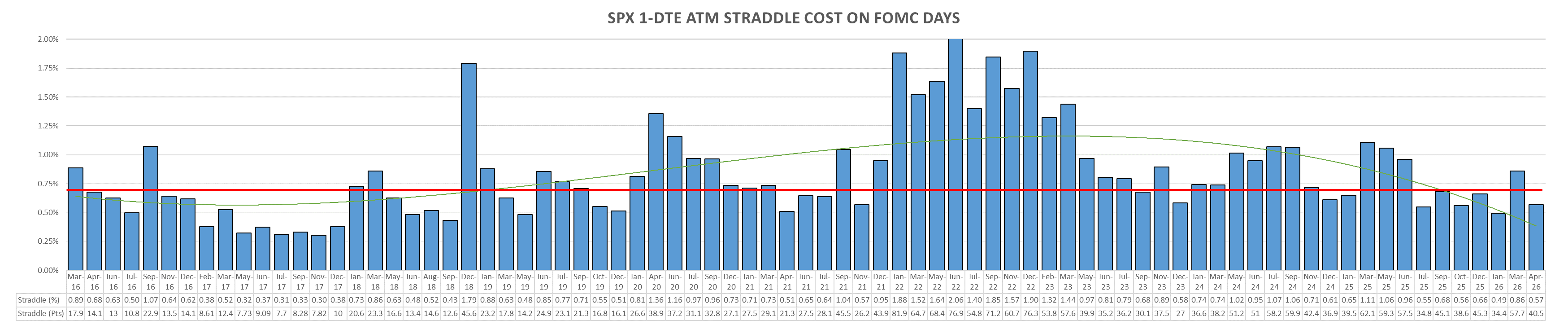

~70bps SPX straddle for tomorrow, highest since July 2025 (March elevated due to overall higher latent implieds.)

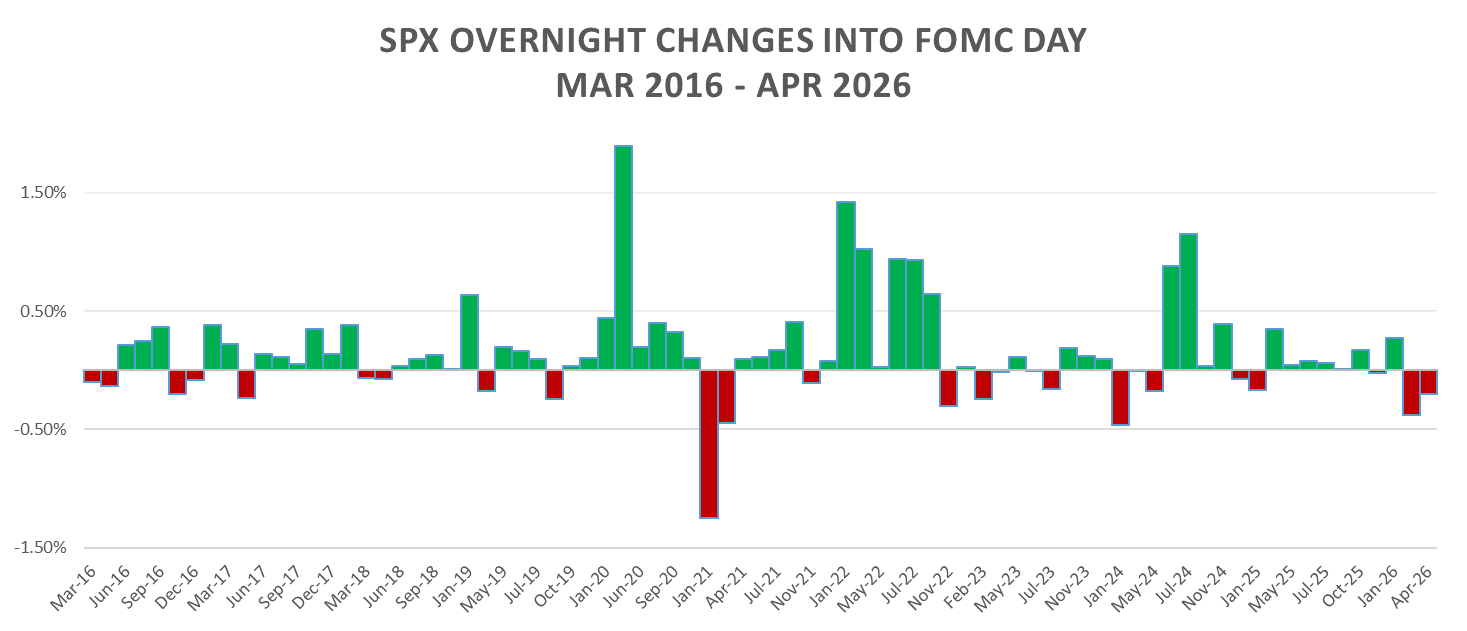

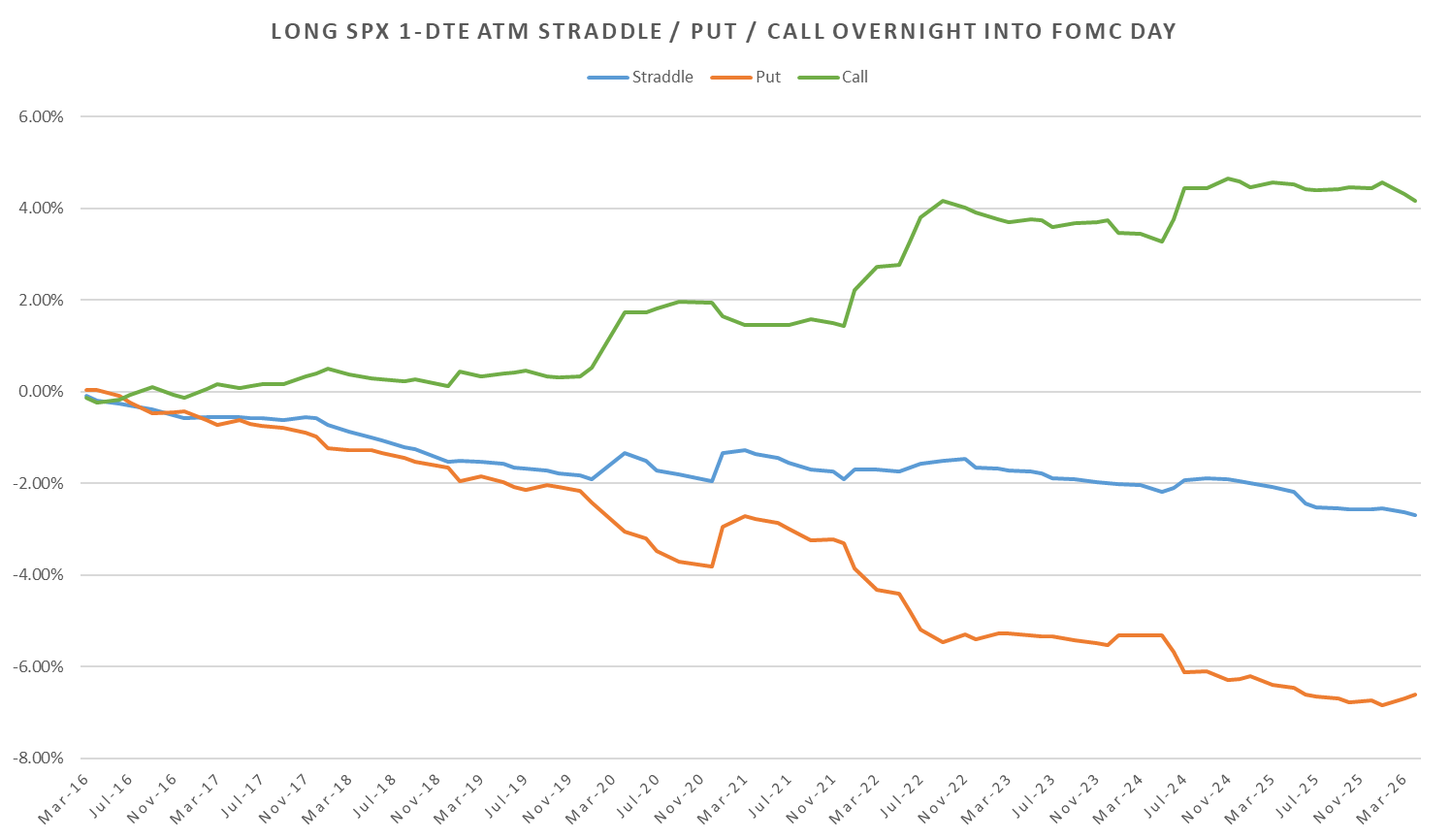

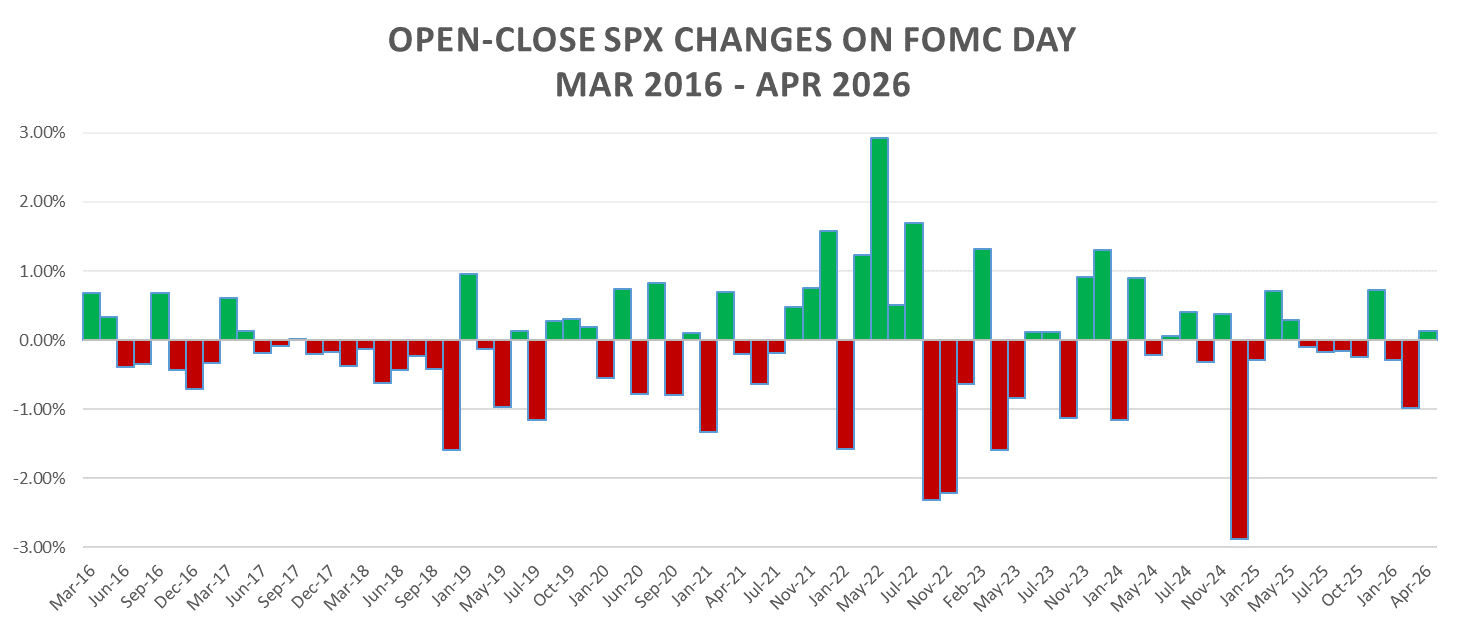

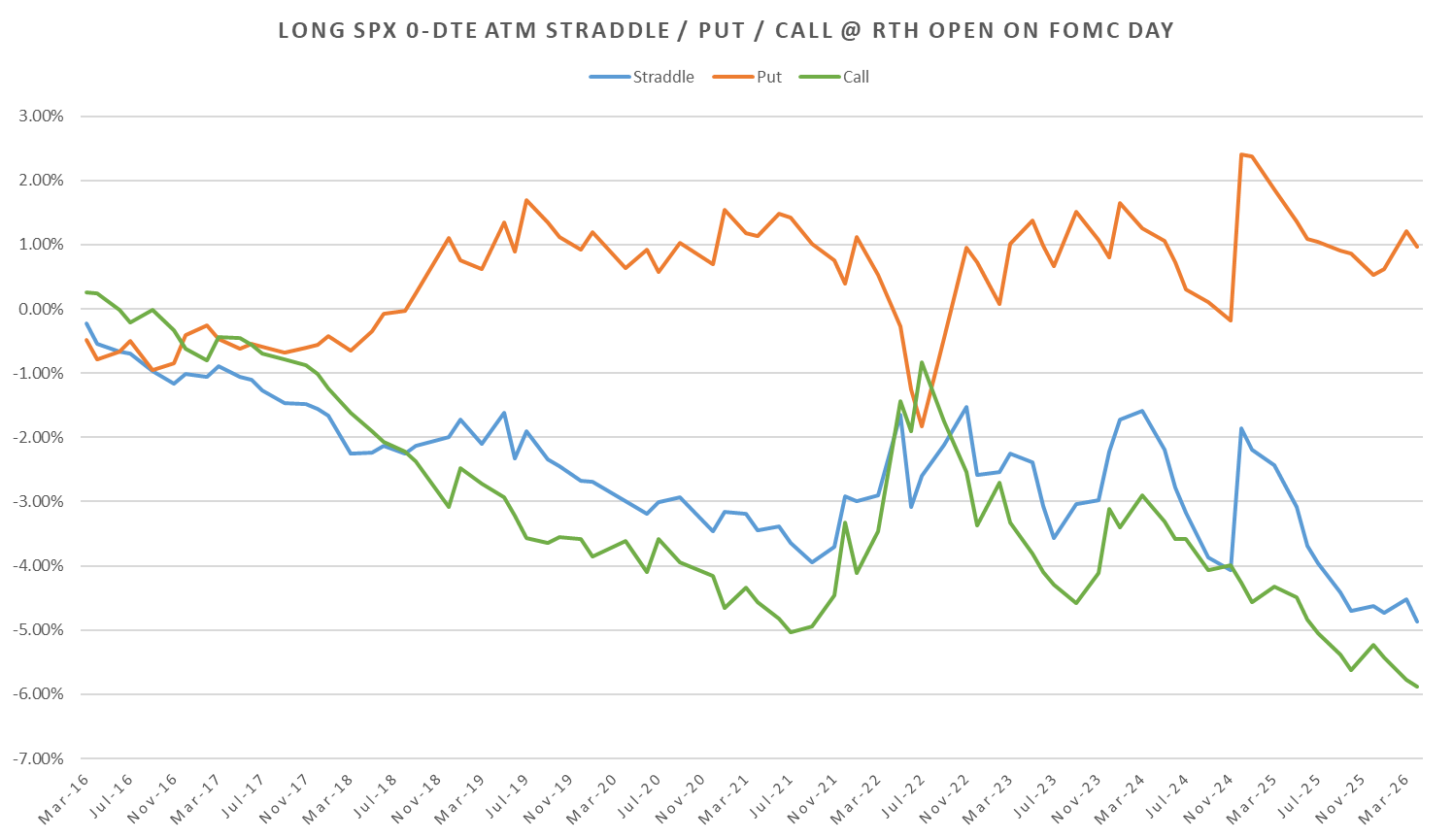

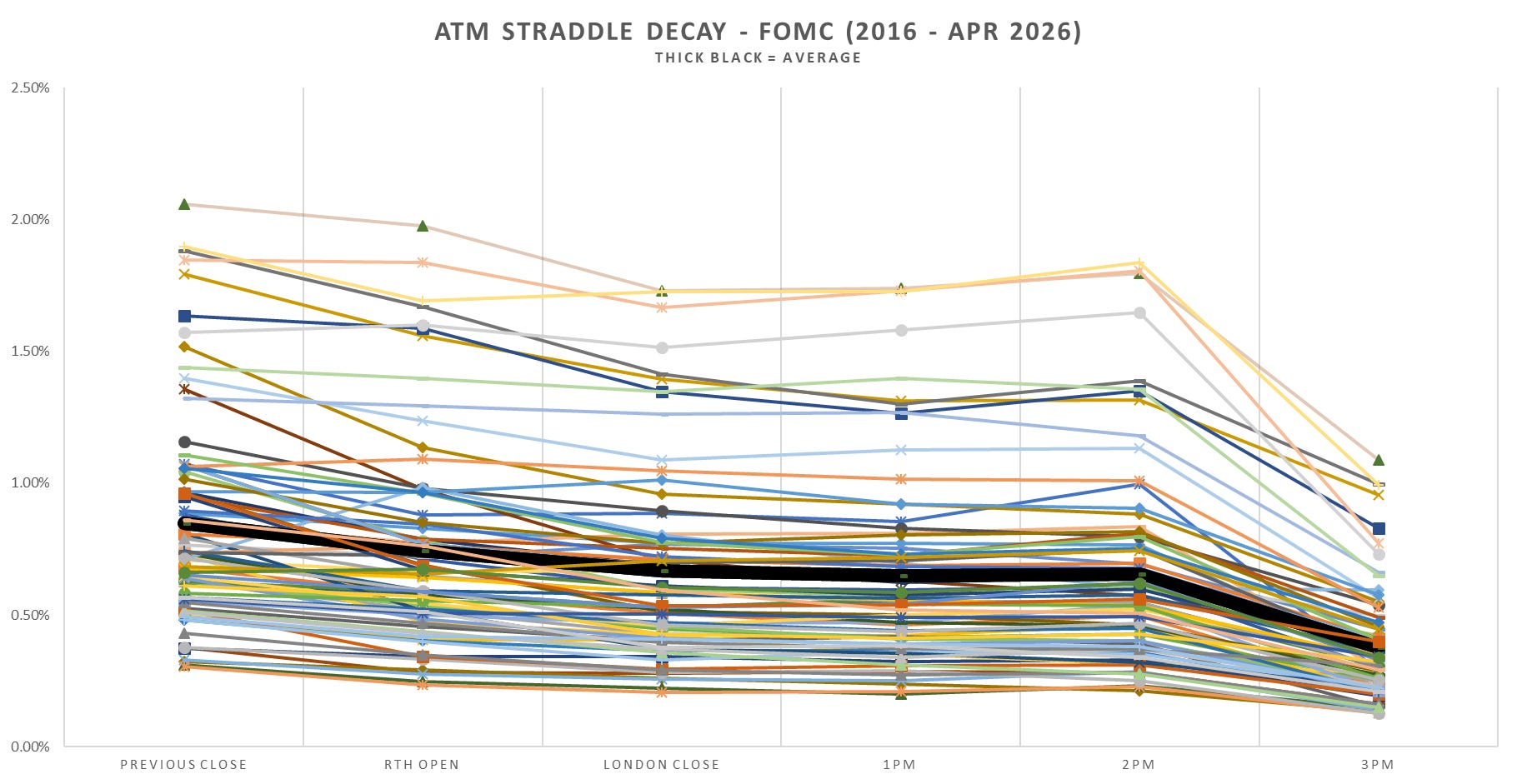

Updated 1-DTE & Intraday SPX Straddle performance:

1-DTE

Overnight Straddles

US cash session straddles

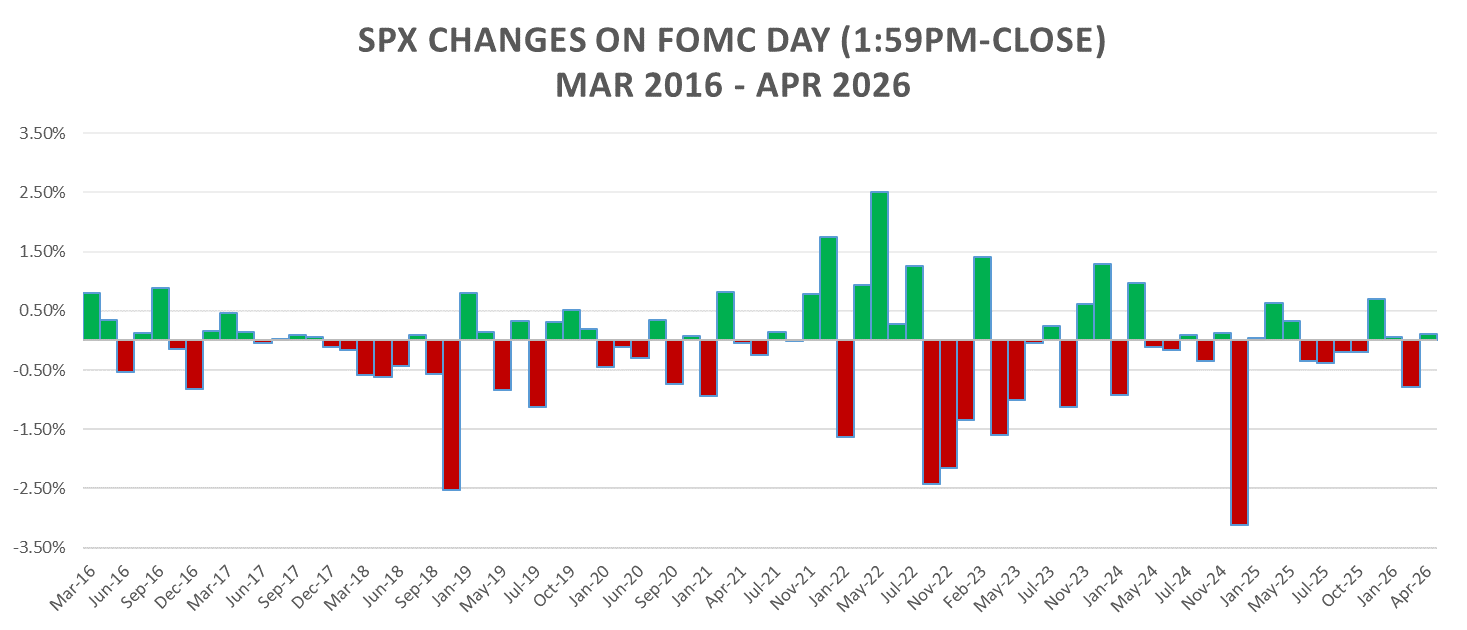

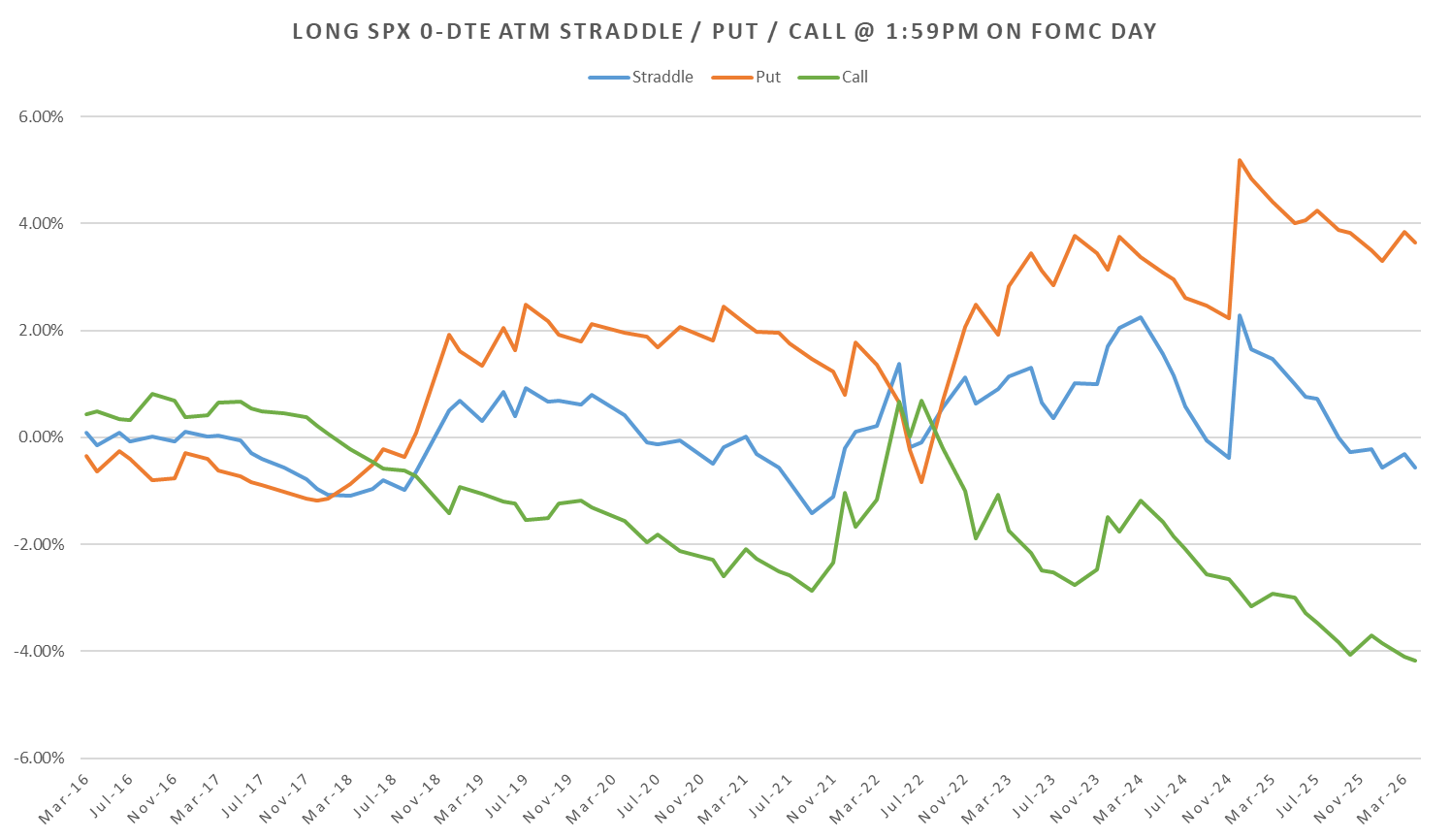

1:59pm - Close (Decision Release)

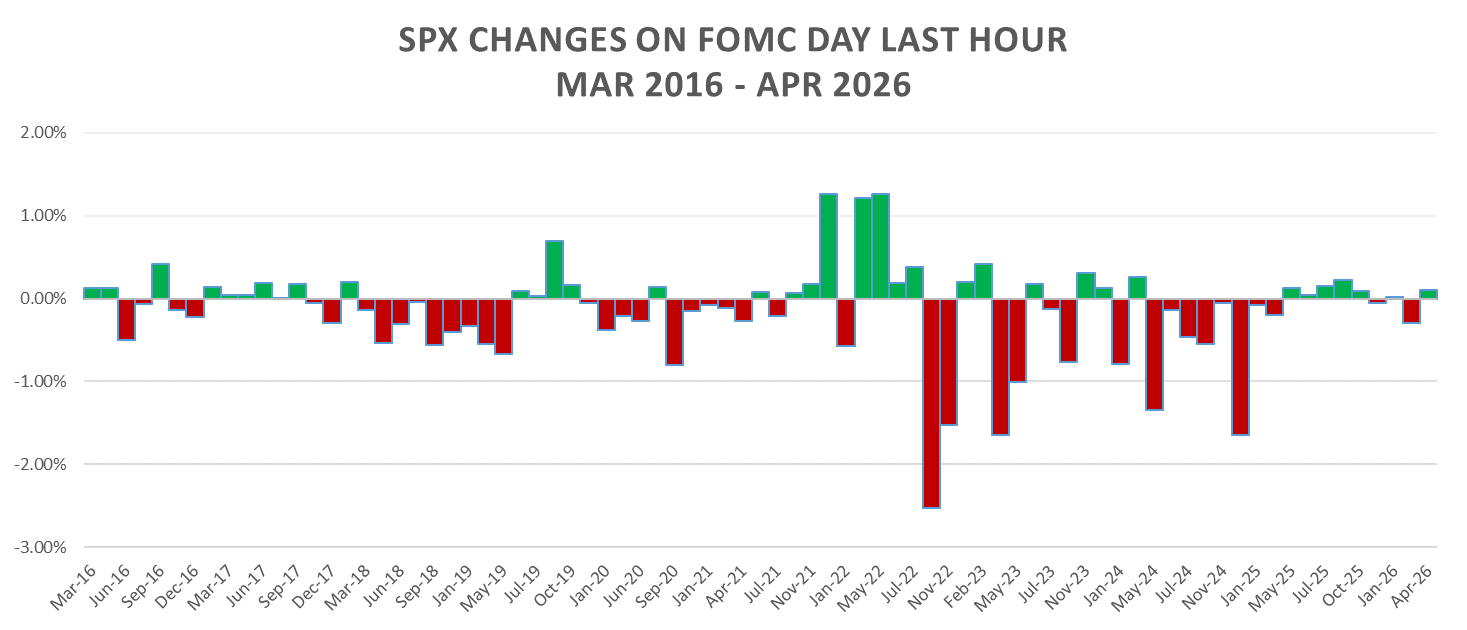

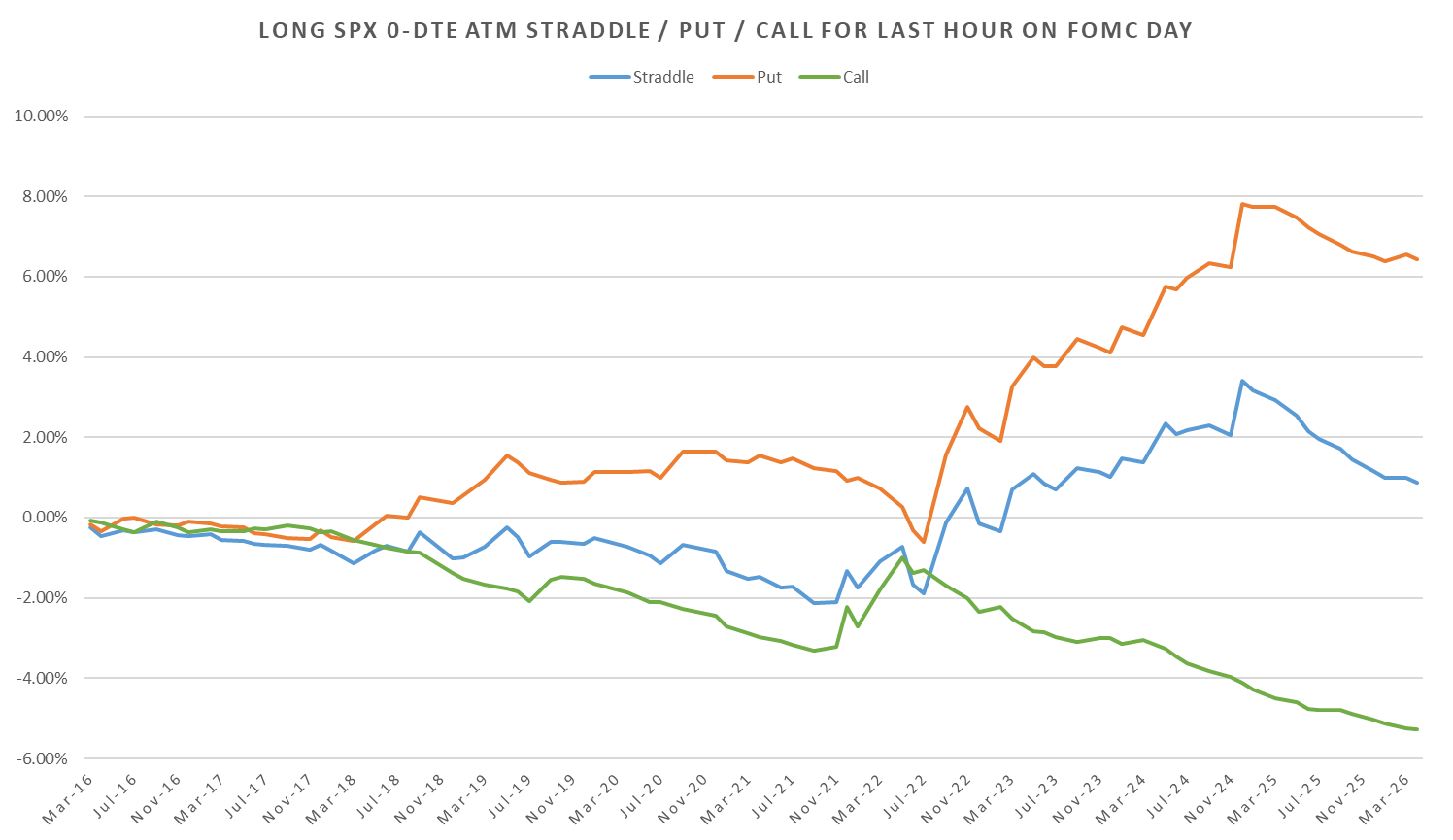

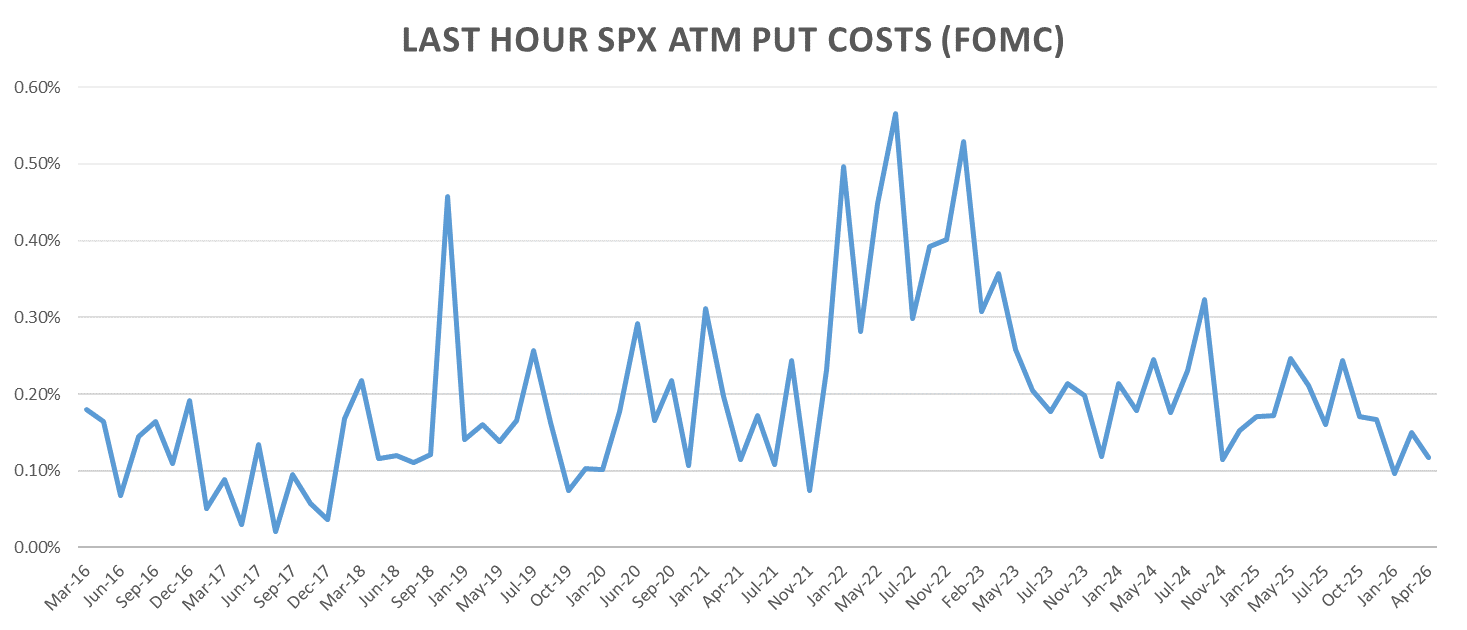

Last Hour (Press conference impact)

Last hour SPX put cost %:

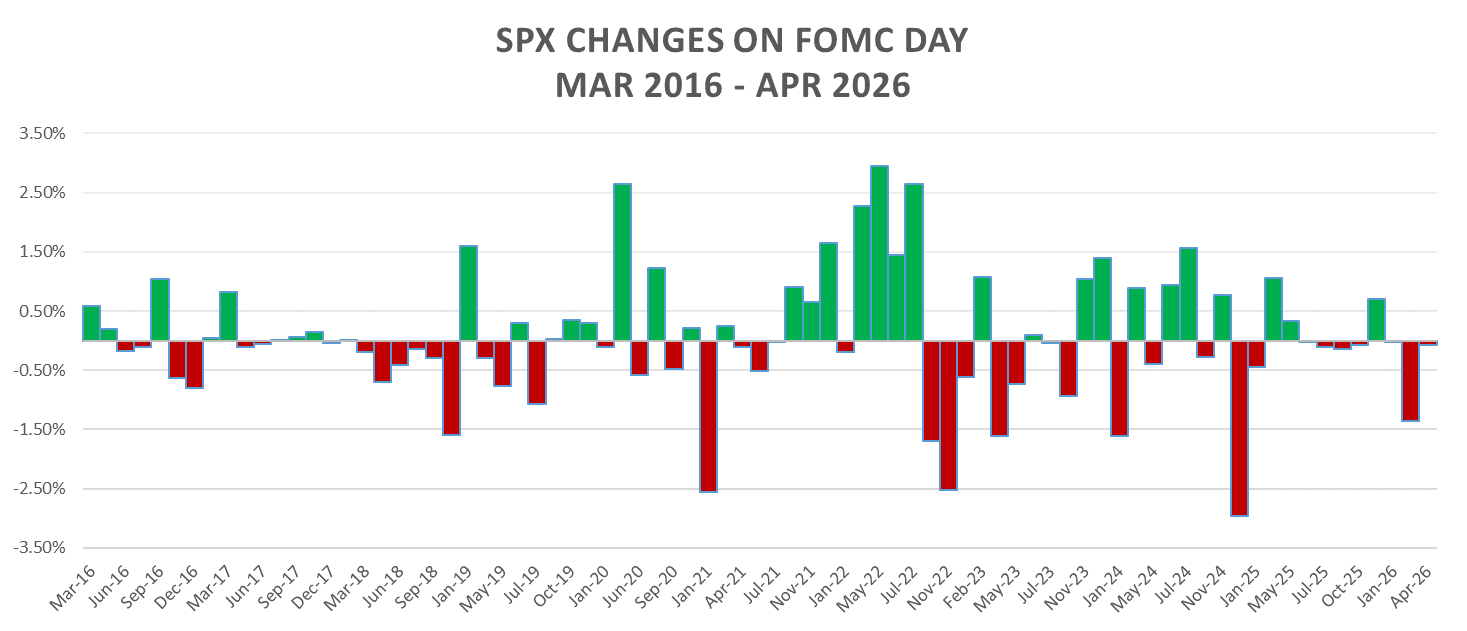

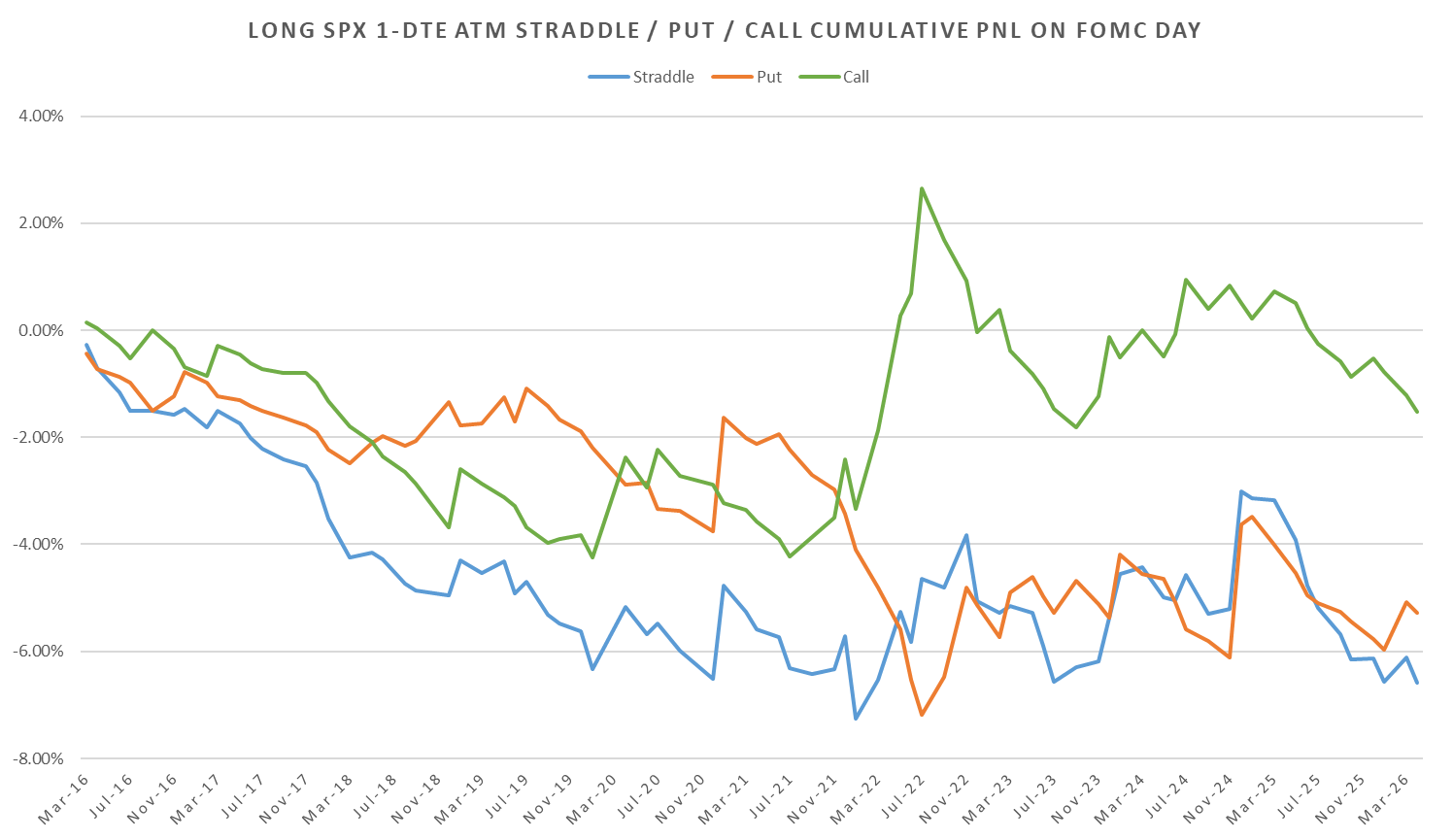

We’ve had a bit of a break in FOMC being relevant last 1.5 years as inflation concerns dissipated (as evidenced by premiums & intraday performance following the press conference.) With rate path uncertainty re-emerging following Iran conflict (due to jumps in energy prices) we might see FOMC become relevant again and the familiar market reactions re-establish themselves. Persistent negative reactions following the press conference from mid 2022 to late 2024 stem from Fed’s reluctance to cut despite markets positioning for lower rates:

Only after Fed undertook a series of cuts in late 2024 markets more or less brushed FOMC aside.

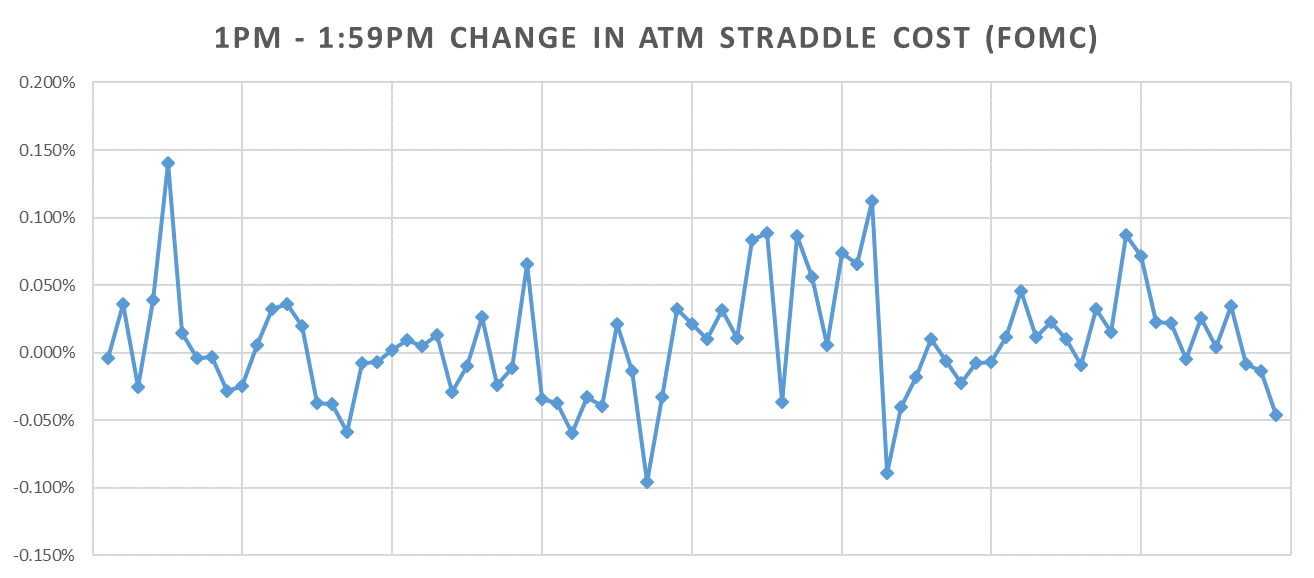

Intraday Straddle Cost - Hourly

Lately a drop in implieds immediately preceding the decision release & press conf have been a good indication that incoming reaction would be a snoozefest.

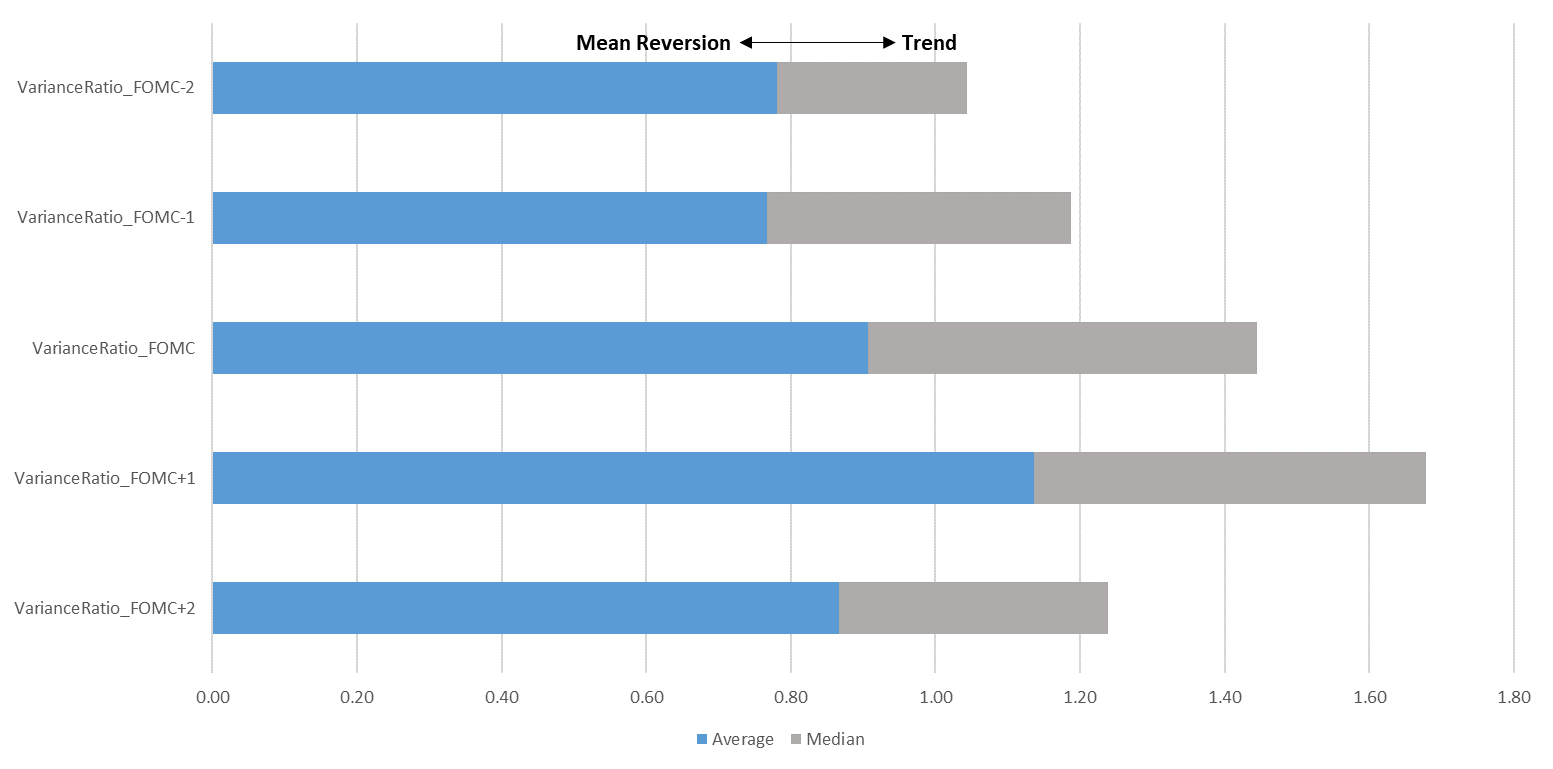

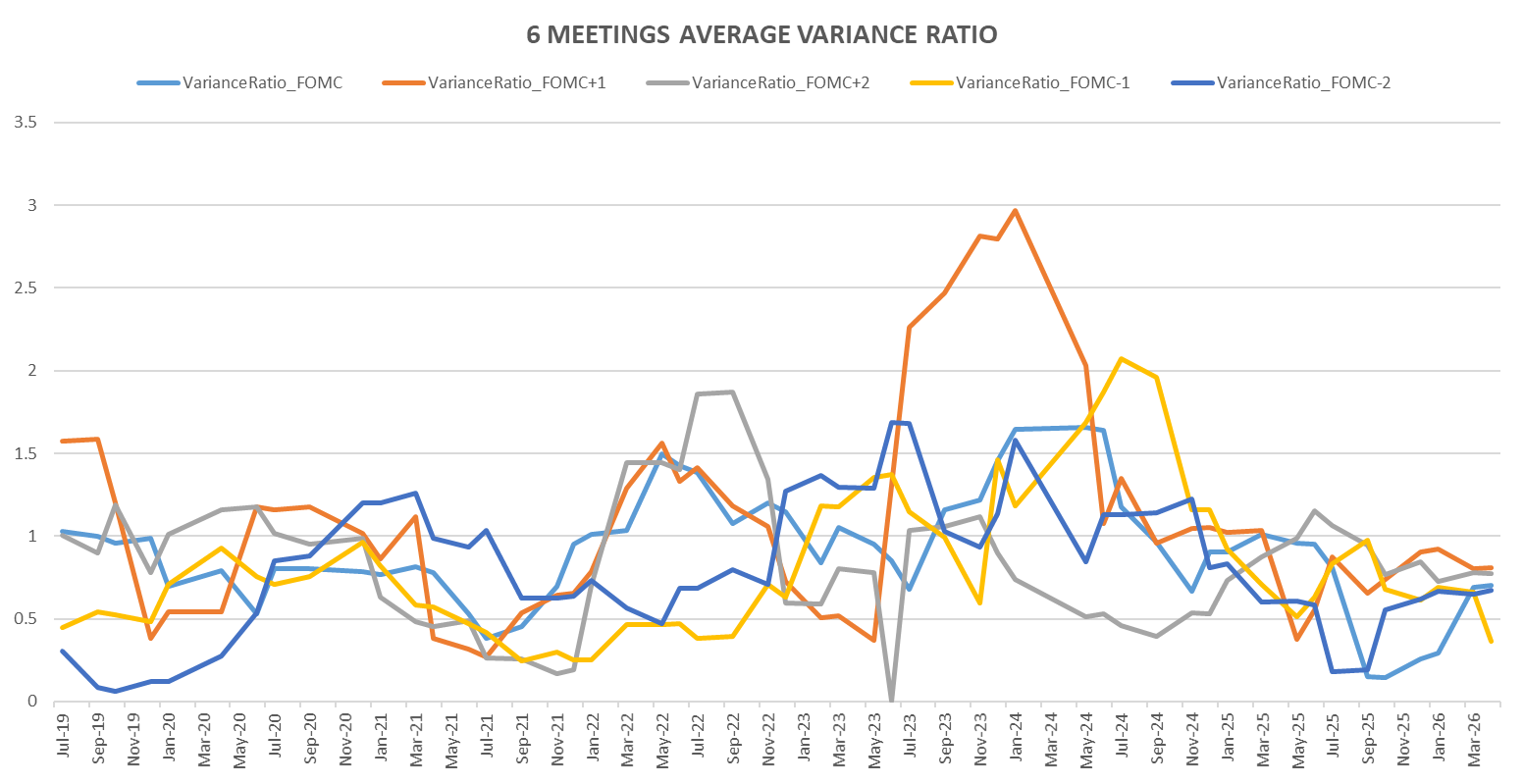

Post-FOMC Trend (Updated to Apr 2026)

Looking at intraday price action going into & few days after FOMC, the ‘expected’ trendy behavior next few days remains clustered around 2023-2024 period when rate path was main focus. Lately, its just been choppy throughout FOMC week without any clear direction following meeting.