Daily / Intraday SPX Straddle Performance

Using variance ratio to trade around long / short 0(1)-DTE SPX straddles

Building on the 0/1-DTE Straddle performance from the April 5th update, decided to explore how the intraday/overnight volatility clustering affects SPX straddle performance when straddles initiated on close prior (1-DTE) or on RTH (regular trading hours) open.

Will be breaking down the straddle performance into long/short as well as long/short 1-DTE against long/short 0-DTE to capture the overnight/intraday volatility clusters (whether market moves more intraday or interday during specific time periods.)

Chart 1.

Chart 2.

First of all, lets do a simple overlay visualized in the above charts. A long/short 1-DTE rolling straddle performance using fixed index notional bet size is plotted against an opposite rth straddle position (so if long 1-DTE straddle, short a 0-DTE ATM straddle at rth open.)

We can see as shown in the previous post (below) the relative outperformance of each individual leg of the trades during 2018-2020 period, with performance being largely in line after mid 2022 with vol more balanced between overnight/intraday periods.

The next question, is how can we improve the performance and take advantage of the difference in overnight/intraday volatility for trading long/short straddles or other option structures?

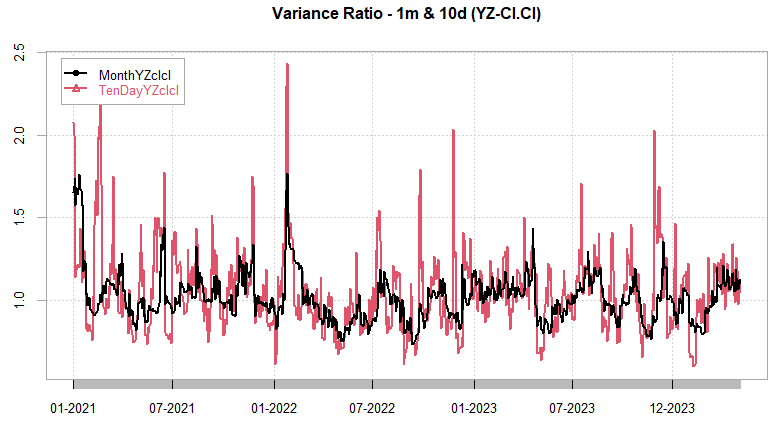

In the last post I mentioned the variance ratio, measuring the ratio of a volatility estimator (Yang-Zhang) that accounts for various intraday movements (opening gaps, high-low, drift) to a simple lower frequency volatility measure like a simple close to close measure. Looking at the charts below, we can see the ratio roughly oscillates around 1-1.1. A high measure implies small close-close volatility but high volatility intraday.

So, lets see if we can take any cues from the variance ratio and improve our 1-0 DTE straddle performance.

Keep reading with a 7-day free trial

Subscribe to Vol Vibes to keep reading this post and get 7 days of free access to the full post archives.